Global| Mar 07 2014

Global| Mar 07 2014German IP Picks Up Strongly As Consumer Goods Lag

Summary

Germany's industrial production in January rose by 0.8%, continuing a string of advances. Over the last three months, industrial production is expanding at a sharp 13.9% annual rate. That's up significantly from a 5.9% annual rate [...]

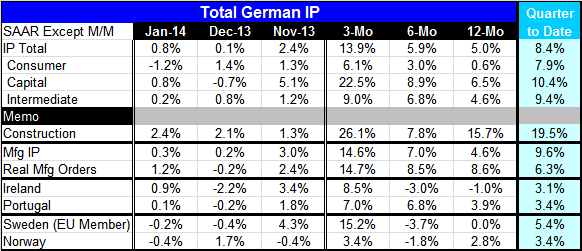

Germany's industrial production in January rose by 0.8%, continuing a string of advances. Over the last three months, industrial production is expanding at a sharp 13.9% annual rate. That's up significantly from a 5.9% annual rate over six months and a 5% annual rate over 12 months. Capital goods are leading the increase with a 22.5% annual rate increase over three months and a 6.5% annual rate increase over 12 months. Next in line is intermediate goods; there output is rising at a 9% annual rate over three months and at a 4.6% annual rate over 12 months. Bringing up the rear is consumer goods. Consumer goods output is up at a 6.1% annual rate over three months and only a 0.6% annual rate over 12 months. The output of consumer goods by German firms is trailing capital goods by a long shot. And consumption in Germany is also a trailing sector in the economy.

Germany's industrial production in January rose by 0.8%, continuing a string of advances. Over the last three months, industrial production is expanding at a sharp 13.9% annual rate. That's up significantly from a 5.9% annual rate over six months and a 5% annual rate over 12 months. Capital goods are leading the increase with a 22.5% annual rate increase over three months and a 6.5% annual rate increase over 12 months. Next in line is intermediate goods; there output is rising at a 9% annual rate over three months and at a 4.6% annual rate over 12 months. Bringing up the rear is consumer goods. Consumer goods output is up at a 6.1% annual rate over three months and only a 0.6% annual rate over 12 months. The output of consumer goods by German firms is trailing capital goods by a long shot. And consumption in Germany is also a trailing sector in the economy.

Construction is a strong contributor to industrial output in January. It rose at a 2.4% rate month-to-month in January. It's up at a 26.1% annual rate over three months and at a 15.7% annual rate over 12 months. A spell of mild weather has helped to spur industrial production in construction.

For manufacturing alone, production is up at a 14.6% annual rate over three months and has accelerated from its six-month and its 12-month pace. Real manufacturing orders also have continued to spurt. They are up at a 14.7% annual rate over three months and an 8.6% annual rate over 12 months.

In the new-quarter to date, which is a comparison of January to the fourth quarter base of activity, we have industrial production up at an 8.4% annualized rate. Capital goods continue to lead, rising at a 10.4% annual rate. Construction is up at a whopping 19.5% annual rate. Manufacturing by itself has industrial production up at a 9.6% annual rate with manufacturing orders in real terms up at a 6.3% annual rate. Germany's output is doing well.

We have two early reporters among euro area countries, Ireland and Portugal. Each of them shows an increase in output in January following declines in December. Each of them shows strong increases in industrial output, a 14.6% for Ireland and 14.7% for Portugal over the last three months. However, over 12 months Ireland's output is still falling by 1% while Portugal's output is up at a 3.9% annual rate. In the new quarter pressure industrial production in these countries is up at a pace in excess of 3%.

Sweden and Norway, two European countries, one an Economic Union member, showed declines in output in January. Both Sweden and Norway show increases over three months with Sweden getting the best of it at a 15.2% annual rate over three months compared with a 3.4% rate of increase for Norway. Over the last 12 months, however, output in Sweden is flat compared to Norway with output rising at a 2.8% annual rate. In the quarter to date, both Sweden and Norway are posting increases in output that are solid. For Sweden, output is up at a 5.4% annual rate; for Norway it's up at a 3.4% annual rate.

Increases in output have been common among the official industrial production figures for European countries as well as for indicators such as diffusion indexes in manufacturing and even for services. The continuing signal is that Europe is improving and expanding. The problem or fly-in-the-ointment has to do with the pace of the expansion and lingering concerns about sustainability. There are still broad differences among members in the community and other examples of uneven development. In this month's numbers form Germany, the question marks are raised about the consumer sector. Germany's consumer sector is showing a decline in output in January and a limp increase of less than 1% over 12 months. In the quarter to date consumer goods output is doing much better, but that's based on one month over the fourth quarter base and certainly is only indicative.

The sharp increase in construction output suggests that some of the increase in output is temporary and weather-related. However, the ongoing strength and rise and real manufacturing orders suggests that there is an ongoing drumbeat of demand for German products. Seeing continuing increases of output in Ireland and Portugal, two economies that have struggled, is somewhat reassuring for Europe. For the time being, we can be content with this report which is encouraging but not decisive.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.