German Orders Fall Again, Unexpectedly

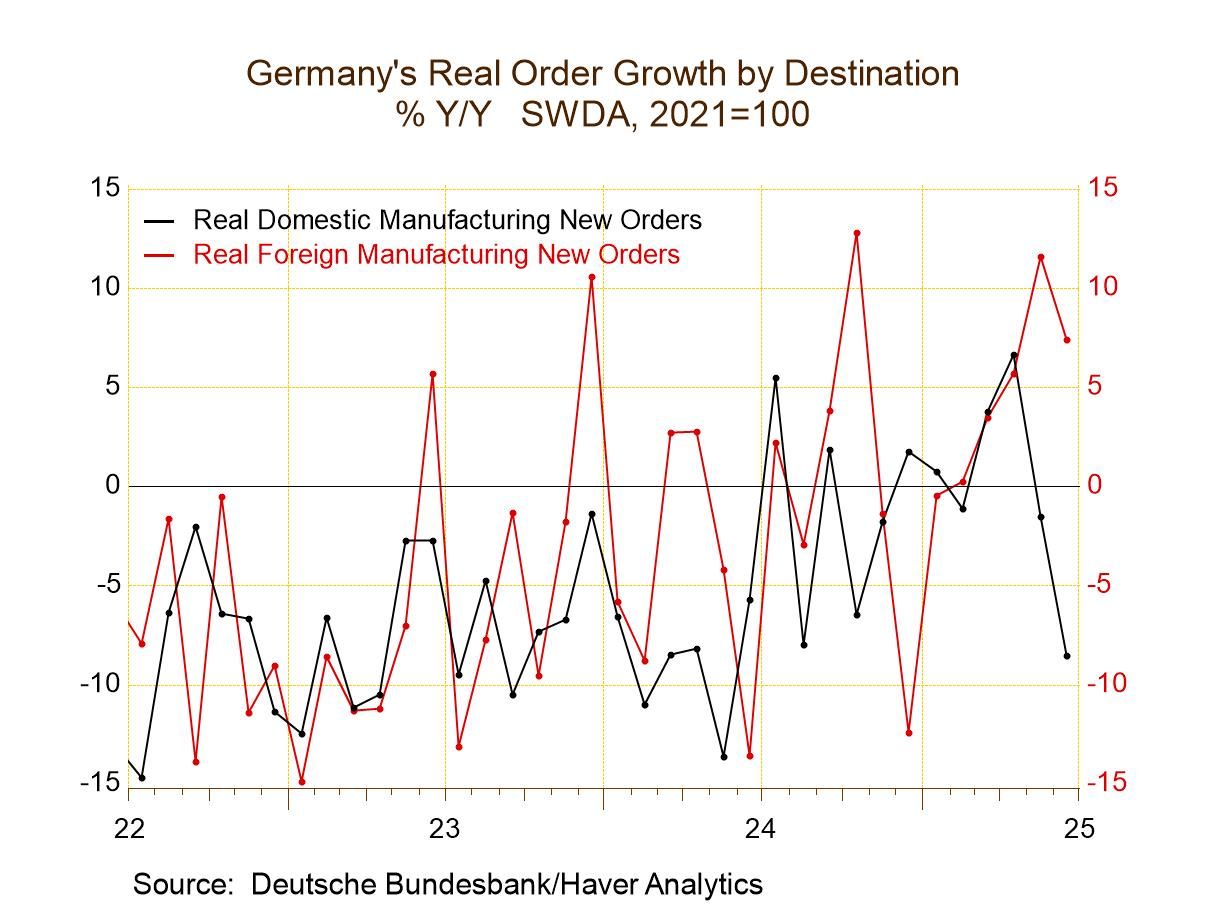

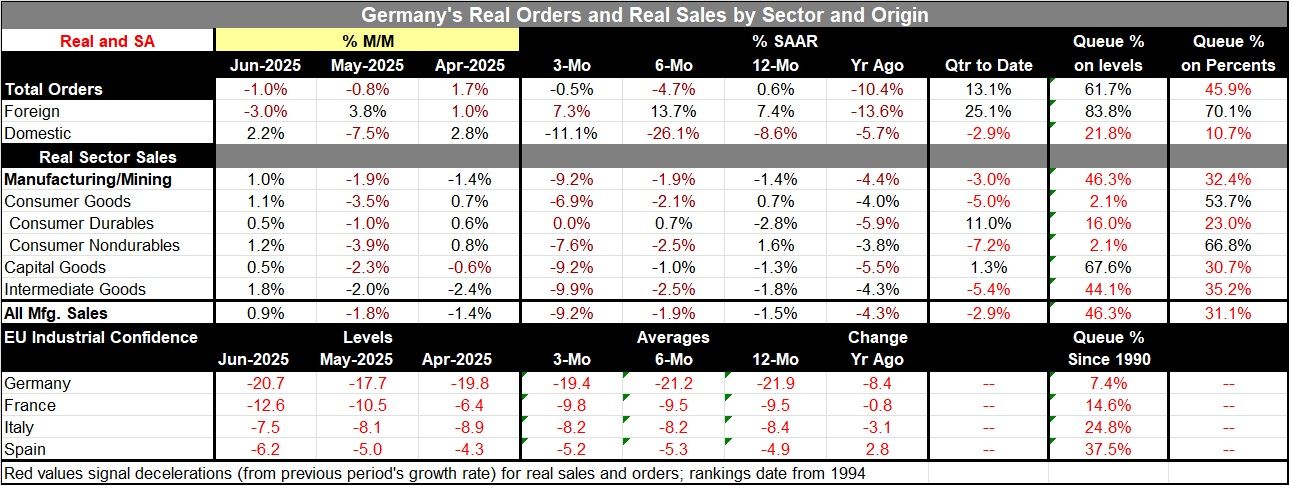

German orders expressed in real terms fell by 1% in June after falling by 0.8% in May. Foreign orders fell by 3% month-to-month after rising 3.8% in May. Domestic orders came back to life rising by 2.2% in June but only after a sharp 7.5% drop in May; that drop had been preceded by a 2.8% increase in April. The gyration and trend performance of orders is still choppy and, for the most part, weak.

Order trends Sequential growth rates show that overall orders for Germany (still expressed in real terms) rose by 0.6% over 12 months; however, they fall at 4.7% annual rate over six months and fall at a 0.5% annual rate over three months. Foreign orders rise by 7.4% over 12 months; over six months the gain is at a 13.7% annual rate, and over three months that pace is reduced to a 7.3% annual rate. German domestic orders fall by 8.6% over 12 months, then decline at an extremely rapid 26.1% annual rate over six months, and continue to decline at 11.1% annual rate over three months. For the time being, orders have been propped up by strength in the international market while domestic orders continue to languish and to contract.

Real sales Sector sales, expressed in real terms, rose by 1% and those across all the components after seeing widespread contractions in May that had followed an uneven performance in April. Real sales for manufacturing fall by 1.5% over 12 months, fall at a 1.9% annual rate over six months, and fall at an annual rate of 9.2% over three months. Real sales trends are not reassuring.

European Surveys on Industry Survey results for the largest economies in the European Monetary Union show slippages in June compared to May as three of the four large economies weaken (with Italy being the exception). Over three months France logged a weaker reading compared to six-months, Germany improved, Italy's performance is unchanged; Spain reports a result that's better by a single tick on the survey index comparing 3-months to 6-months. Comparing the 12-month to averages to 3-month averages for the four large European economies, shows deterioration that's across the board with the slight exception of Italy.

Quarter-to-date (completed Q2) The quarter-to-date (QTD) performance in Germany for orders are strong, rising at a 13.1% annual rate. Sector sales show deteriorated real sector sales across most sectors on QTD basis; manufacturing sales fall at a 2.9% annual rate.

Longer term evaluations The two right hand columns evaluate the growth and level performance of these various metrics on real sector sales and on a level basis and well as on annual growth rates. Total orders and foreign orders ranked on levels are well above their 50% mark, which puts them above their median on data back to 1994. Domestic sales levels have only a 21.8 percentile standing, extremely weak. Rankings on growth rates show total orders at a 45.9 percentile ranking, below the median growth rate (which occurs at a ranking of 50%). However, foreign orders’ growth ranks in the 70th percentile, quite firm, while the domestic growth rate queue ranking resides in the lower 10.7 percentile of its range. Growth rates for real sector sales are mostly below their 50-percentile mark except for consumer nondurables and consumer goods sales overall (which, of course, are boosted by the sales of consumer nondurables). The industrial confidence indicators for European economies that are from diffusion surveys are evaluated relative to historic levels only. All of them score weak results. The best queue standing is Spain with a 37.5 percentile standing, followed by Italy at a 24.8 percentile standing. France has a 14.6 percentile standing, while Germany has a 7.4 percentile standing. These range from weak, and below median, to very weak.

Summing up On balance, German performance in June is poor. The trends are poor, and far from reassuring. Sector sales performance is poor. Performance across Europe continues to be poor as captured by survey results- that performance continues, for the most part, to deteriorate. However, German quarter-to-date growth rates for orders are strong in Q2 compared to Q1, but that is only on the back of strength in foreign orders. German domestic orders are still behaving badly. All-in-all, it's a disappointing report on the manufacturing sector for Germany and for what we survey of Europe.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief

Global

Global