Global| Jun 08 2015

Global| Jun 08 2015German IP Heads Higher

Summary

German capital goods sector turns sharply higher as the rest of IP continues to struggle. Industrial output rose by 0.9% in April after a 0.4% decline in March. Overall IP growth is advancing on all horizons with growth in a 3.4% to [...]

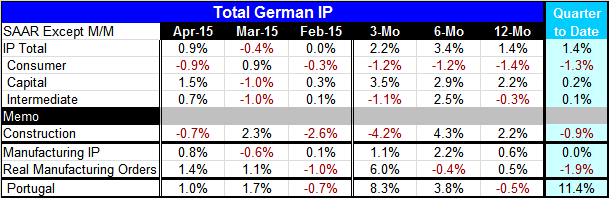

German capital goods sector turns sharply higher as the rest of IP continues to struggle. Industrial output rose by 0.9% in April after a 0.4% decline in March. Overall IP growth is advancing on all horizons with growth in a 3.4% to 1.4% range.

German capital goods sector turns sharply higher as the rest of IP continues to struggle. Industrial output rose by 0.9% in April after a 0.4% decline in March. Overall IP growth is advancing on all horizons with growth in a 3.4% to 1.4% range.

Only capital goods output is showing building growth with the rate rising from 2.2% over 12 months to 2.9% over six months and to a 3.5% annual rate over three months. In comparison, consumer goods output is falling on all horizons and intermediate goods output is declining over 12 months and over three months.

While German IP is gaining in April and rising in two of three sectors, momentum remains suspect. Even the construction sector that has been very strong in Germany is showing an output decline in April and a net drop over the most recent three months. IP in manufacturing is up by 0.8% in April and yet its sequential growth rates are in a range of 0.6% to 1.1%.

Real manufacturing orders show a pop of 1.4% in April and post a 6% annual growth rate over three months. That is reassuring as orders do tend to lead output with some reliability in Germany.

For the quarter to date, a tentative calculation with only one month's data from the new quarter in hand, we find overall IP up at a 1.4% annual rate with manufacturing IP dead flat in the new quarter.

Portugal is the only other EMU member that has reported IP early. It has production accelerating from 12 months to six months to three months. Portugal is still on a tear. And Portugal's output is up very strongly in the quarter to date.

However, for the euro area as a whole, investor confidence has fallen this month. The euro area investor confidence index fell to 17.1 in June, a four-month low, from 19.6 in May.

The rebound in German IP in May is good news but not great news and it is not news that we can take to the bank about growth talking root in the euro area. Indeed, with the Group of Seven meeting in Europe, there are still many unresolved European issues of importance pending including the fate of Greece.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief