Global| Jul 08 2009

Global| Jul 08 2009German IP Follows Orders Higher

Summary

German industrial production rose by 3.7% in May from April. It has risen in two of the last three-months. IP is accelerating, rising at a 5.4% annual rate over three-months compared to a rate of minus 22.2% over six-months and minus [...]

German industrial production rose by 3.7% in May from April. It has risen in two of the last three-months. IP is accelerating, rising at a 5.4% annual rate over three-months compared to a rate of minus 22.2% over six-months and minus 18.1% over twelve-months. Still in the quarter to date IP is contracting at a pace of 6.1%. Two months into the second quarter, despite the stirring in the industrial sector, IP is still a subtraction from growth.

Construction is showing a steady acceleration and positive growth rates over 3-months, 6-months and 12-months. Manufacturing is up at a strong 10% annual rate over three-months but still falling at a 6.6% pace in the current quarter.

Industrial orders are rising on a much more explosive path over this period. But orders are a precursor to increases in output.

Among large EMU countries Spain and the UK also have reported industrial output measures for May. For each of them the May result for MFG output was negative. But MFG output in Spain and in the UK had risen in April. In the UK output is falling at a 0.9% pace in Q2. In Spain output is dropping at a 3% pace in Q2.

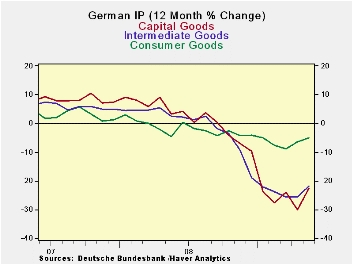

These trends have the trappings of a bottoming in progress but not here yet. The German chemicals industry reported that it had made a recession bottom already. For Germany , as a whole, capital goods orders are leading the way out. In May these orders surged by 8.3% compared to April, but that was after a 6.9% plunge in April output itself. Intermediate goods output was up by 4.3% in May. The consumer is not a major factor in the rebound. Output from consumer goods industries is up by 0.6% in May, the second monthly rise in a row, but it is still falling at a pace of 5.4% in Q2. Capital goods output is declining at an 11.5% pace in Q2 and intermediate goods output is falling at a 2.1% pace. There are signs of stirring but no evidence that the real positive thrust is here yet.

Overall there is evidence of the drop in output and the decline in GDP slowing or of a bottom forming and tentative signs of a rise from the lows being put in place for industrial output. The UK reported consumer sentiment rose in June as another sign of optimism in Europe . The G-8 is getting ready to meet and tell us that we have not turned the corner yet. The message from that is for countries not to reverse the stimulus that is in place but a further subtle message is not to commence any new stimulus either.

| Total German IP | Quarter | ||||||

|---|---|---|---|---|---|---|---|

| Saar exept m/m | May-09 | Apr-09 | Mar-09 | 3-mo | 6-mo | 12-mo | to-Date |

| IP total | 3.7% | -2.6% | 0.3% | 5.4% | -22.2% | -18.1% | -8.1% |

| Consumer | 0.6% | 0.5% | -1.0% | 0.4% | -5.7% | -5.0% | -5.4% |

| Capital | 8.3% | -6.9% | 3.7% | 19.1% | -31.2% | -22.6% | -11.5% |

| Intermed | 4.3% | -1.0% | -1.7% | 6.4% | -23.5% | -21.8% | -2.1% |

| Memo | |||||||

| Construction | -3.2% | 0.0% | 6.0% | 11.2% | 5.0% | 1.3% | 14.8% |

| MFG IP | 4.9% | -3.1% | 0.8% | 10.1% | -24.6% | -19.5% | -6.6% |

| MFG Orders | 4.4% | 0.1% | 0.0 | 38.4% | -17.4% | -28.8% | 19.4% |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief