Global| Nov 07 2018

Global| Nov 07 2018German IP Advances at Slow Pace...Maybe

Summary

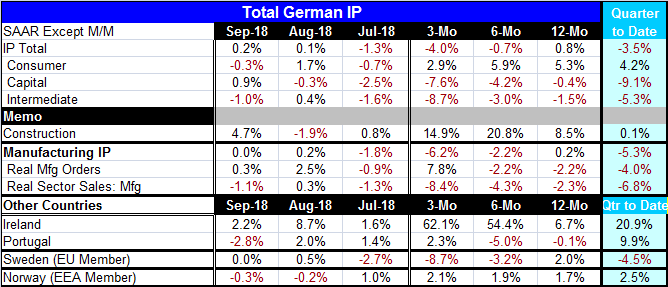

Germany's industrial production rose by 0.2% in September as manufacturing output was flat. Overall IP gained 0.8% over 12 months while manufacturing gained only 0.2%. Still, IP is growing and the PMI signal from the Markit gauge is [...]

Germany's industrial production rose by 0.2% in September as manufacturing output was flat. Overall IP gained 0.8% over 12 months while manufacturing gained only 0.2%. Still, IP is growing and the PMI signal from the Markit gauge is positive. The German manufacturing IP and Markit manufacturing series track one another reasonable well at this time. Their peaks and troughs, their accelerations and decelerations seem to match up quite well and one would be very hard pressed to call one a bellwether for the other...except that the Markit PMI data are always at least one month fresher than IP data.

Germany's industrial production rose by 0.2% in September as manufacturing output was flat. Overall IP gained 0.8% over 12 months while manufacturing gained only 0.2%. Still, IP is growing and the PMI signal from the Markit gauge is positive. The German manufacturing IP and Markit manufacturing series track one another reasonable well at this time. Their peaks and troughs, their accelerations and decelerations seem to match up quite well and one would be very hard pressed to call one a bellwether for the other...except that the Markit PMI data are always at least one month fresher than IP data.

For the time-being, the Markit diffusion survey is not pointing to a decline in German IP (diffusion >50), but the series value is quite low. The IP series taken on its own has been decelerating from 12-months to six-months to three-months. And while it has logged two monthly increases in a row, the monthly gains have been anemic at 0.2% and 0.1% in September and August, respectively. Moreover, manufacturing IP is flat in September and rose in August by only 0.2% after a 1.8% decline in July. Year-over-year total output is up by 0.8% while manufacturing output is up by only 0.2%. None of that inspires confidence.

Manufacturing metrics

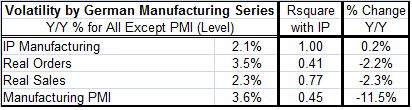

The manufacturing IP series has a reasonably strong correlation with real orders, real sales, and the manufacturing PMI. The manufacturing PMI is still above the key 50 level pointing to continued expansion, but the PMI index has fallen by 11.5% over 12 months. Of course, IP is still up by a scant 0.2% over 12 months, but real manufacturing orders and real manufacturing sales both are lower on balance over 12 months. And both of them have as strong or a stronger correlation with manufacturing IP than the manufacturing PMI. Still, the manufacturing PMI level remains above 50 and that signal continues to support an outlook for expansion.

The manufacturing IP series has a reasonably strong correlation with real orders, real sales, and the manufacturing PMI. The manufacturing PMI is still above the key 50 level pointing to continued expansion, but the PMI index has fallen by 11.5% over 12 months. Of course, IP is still up by a scant 0.2% over 12 months, but real manufacturing orders and real manufacturing sales both are lower on balance over 12 months. And both of them have as strong or a stronger correlation with manufacturing IP than the manufacturing PMI. Still, the manufacturing PMI level remains above 50 and that signal continues to support an outlook for expansion.

There are many economic indicators and more for manufacturing than for most series. Their signals all are weakening; their prognosis for growth differs. The German PMI for services also has weakened, but it is still above its level of 50. For Germany, domestic conditions continue to expand. However, Germany is a very export and trade oriented economy, and trade right now is under pressure. German domestic indicators may not be the best gauges of the future for this economy.

Beyond Germany

As we saw in yesterday's report on German orders (a report that also includes a table of the new PMI readings for the EMU here), the PMI gauges in the EMU and for Germany are extremely low by the standards of the last four and one half years. The EMU composite index has been lower since January 2014 only 20.7% of the time, the German composite has been lower only 10.3% of the time, the Spanish index has been lower only 5.2% of the time, and the Italian index is on its low for the period. Yet, only Italy has a PMI index of any sort (composite, manufacturing or services) below 50 (and Italy has a trifecta of those). The prediction from the PMI indexes is that Europe has weakened but not that it is contracting- at least that signal is not in play yet and the ECB says that is not in the cards.

Still, PMI momentum remains in a downward spiral across the EMU with few exceptions and even the exceptions themselves are only technical in nature. There is still plenty to worry about on the growth front and on the trade front. The daily Baltic dry index is starting to deteriorate more noticeably and the weekly index shows no growth year-over-year. The trade war which should hit manufacturing harder than services and hit manufacturing first seems to be doing just that.

The GFOL (Geopolitical Facts of Life)

While economic conditions globally clearly are deteriorating, politics have reared their ugly head in a lot of places. We can have a great deal of concern that distractions of the political or geopolitical sort are going to distract a lot of policymakers and cause them to take their eye off of economic needs. While politicians are busy doing what they do best (which is wrangling, complaining and blaming the ‘other guy'), the economy is deteriorating. In the U.K. and Europe, one issue is Brexit. Also in the EU, the issue is the Italian budget. PMI data tell us how bad things are in Italy and the EU has refused to cut Italy any slack on EU rules even though in the past Germany and France have evaded sanctions for their own missteps. Theresa May is under extreme pressure, but no one will challenge her until the Brexit baton is passed because no one wants to inherit that mess. German politics are upside down with Angela Merkel leaving. Even France's President Emmanuel Macron has gotten himself in hot water over comments made about a French war hero that has Nazi affiliations. The EU Commission hopes that Italy's Northern League and Five Star Movement will turn out to be bad dreams (they won't). Spain still struggles with Catalan succession. There is a for-now dormant U.S. European trade conflict that is being held in abeyance. The U.S. and China are trade-warring full tilt. North Korea is dragging its heels on denuclearization while pushing unification. New U.S. sanctions on Iran and possible new sanctions on Russia for its chemical weapons use muddy the waters further on U.S.-Russian relations. And Europeans wanted to keep the Iran deal despite its flaws and U.S. sanctions and still want to do business in Iran. In the U.S., the new mid-term elections have given over control of the House to the Democrats and they foresee a wrecking ball aimed at the Trump administration. If they launch that, it is hard to seeing any bipartisan work being done over the next two years in the U.S.

Globally, there are many geopolitical pitfalls- a lot of political distractions for economic policy. I mention ‘a few' above. I hope our new representatives choose wisely and remember that vengeance may seem sweet but what goes around comes around. Is anyone willing to break the cycle of retribution? It distracts policy and focuses attention on partisan goals above national goals. I hope we are done with that... but I doubt it.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief