Global| Mar 08 2010

Global| Mar 08 2010German IP Advances

Summary

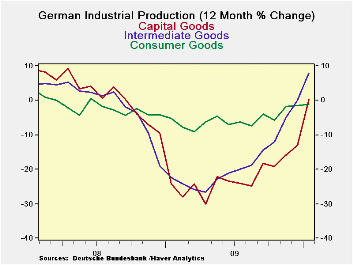

The sharp German recovery in the Yr/Yr growth of industrial production is being led by an upsurge in intermediate goods output. Capital goods output is rising briskly as well. Consumer goods continue to make snail’s pace progress. [...]

The sharp German recovery in the Yr/Yr growth of industrial production is being led by an upsurge in intermediate goods output. Capital goods output is rising briskly as well. Consumer goods continue to make snail’s pace progress. Only intermediate goods output is rising Yr/Yr to any significant degree, but capital goods output now has broken that threshold as well. Still, on a different venue all this is turned upside down.

Although the Yr/Yr rise in IP seems to have strong acceleration across sectors this is NOT confirmed by the sequential growth rates that look at annualized rates of growth over telescoped periods. The table shows that the annualized growth rate over three months for overall IP is just 1.3%, down from 6.8% over six months and below the Yr/Yr rate of 2.1%.Capital goods and intermediate goods output have decelerated sharply over three months compared to six months. But consumer goods output surprisingly is in a sharp accelerating phase with growth at a 12% pace over three months compared to an 8% pace over six months and to -1.2% Yr/Yr.

In the brand new quarter consumer output is rising at an 8.8% annual rate along with intermediate goods where output is up at a strong 5% pace. Capital goods output is falling by 3.2% early in 2010-Q1. Of course the best news for the sector is that orders have stepped up their pace in January after a period of meandering weakness. So whatever hint of slowing or erratic movement we see in the industrial production report, the sector seems to be well underpinned by new orders so that IP growth should continue to be strong in the months to come.

| Total German IP | |||||||

|---|---|---|---|---|---|---|---|

| Saar exept m/m | Jan-10 | Dec-09 | Nov-09 | 3-mo | 6-mo | 12-mo | Quarter to-Date |

| IP total | 0.6% | -1.0% | 0.7% | 1.3% | 6.8% | 2.1% | 1.0% |

| Consumer | -0.1% | 1.6% | 1.3% | 11.9% | 8.2% | -1.2% | 8.8% |

| Capital | -1.0% | 0.3% | 0.7% | 0.0% | 8.1% | 0.2% | -3.2% |

| Intermed | 3.3% | -4.1% | 1.3% | 1.2% | 11.5% | 7.9% | 5.0% |

| Memo | |||||||

| Construction | -14.3% | -2.0% | 0.6% | -49.2% | -28.2% | -9.4% | -63.1% |

| MFG IP | 0.9% | -1.2% | 0.9% | 2.5% | 9.3% | 3.6% | 2.5% |

| MFG Orders | 4.3% | -1.6% | 0.0 | 23.7% | 14.2% | 19.7% | 27.5% |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief