Global| Sep 11 2020

Global| Sep 11 2020German Inflation Stays Down

Summary

Inflation is remaining low globally in the wake of the coronavirus-induced recession. The one exception is that oil prices have flared but now they also are turning lower as the initial recovery spurt in growth is giving way to more [...]

Inflation is remaining low globally in the wake of the coronavirus-induced recession. The one exception is that oil prices have flared but now they also are turning lower as the initial recovery spurt in growth is giving way to more modest results and expectations and as the virus has spread again undercutting both growth and expectations.

Inflation is remaining low globally in the wake of the coronavirus-induced recession. The one exception is that oil prices have flared but now they also are turning lower as the initial recovery spurt in growth is giving way to more modest results and expectations and as the virus has spread again undercutting both growth and expectations.

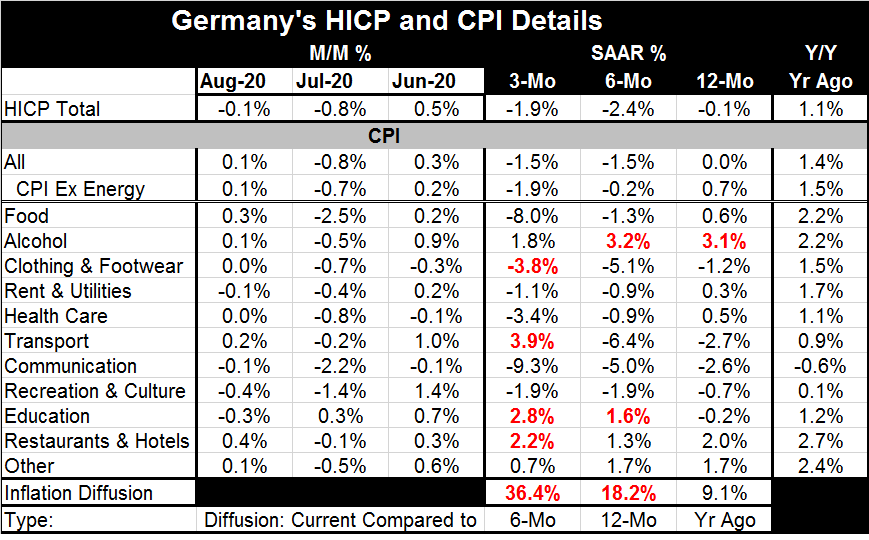

German HICP inflation ticked lower by one tenth of a percentage point in August as the German CPI ticked higher by the same amount. The German HICP is lower by one tenth of one percentage point over 12 months while the German CPI is unchanged over 12 months. But of these are considerably below the old Bundesbank gauge of just under 2% and below the same mark which the ECB currently targets for EMU-wide inflation. Countries do not have separate inflation targets in the EMU.

The diffusion statistic in the table calculates the proportion of sequential inflation rates from the CPI that are stronger than over the previous horizon. Values over 50% show more acceleration than deceleration. Over each horizon in the table, we find inflation diffusion is well below 50%, a feature that supports the extreme underperformance in the headline of both the German CPI and the HICP.

In August alone among the eleven CPI categories, prices fell in the month in four categories and were unchanged in two others. That makes up over half the categories with falling or stable prices levels month-to-month. This follows July, a month in which ten of eleven price levels fell month-to-month. In June, three of eleven price levels fell.

This is clearly still a period when inflation pressures are weak. This comes at a time when the virus is breaking out again across much of Europe and there could be slower growth ahead as a result of that.

Inflation targets are being missed globally although in the U.S. there has been some slight revival of some inflation metrics recently. Nowhere is inflation running hot or consistently higher. Central banks are not focused on it; they are preoccupied with starting or maintaining growth. Unemployment rates are elevated and growth prospects seem to be damped. Central banks are running full out pretending they have more they can do to stimulate growth. And while they can technically do ‘more’ there is not much they can do that will make a difference. The virus is a constant problem as countries try to develop momentum but are persistently being forced to pull back as the virus spreads. This process has impeded the development of growth and inflation.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief