Global| Aug 25 2016

Global| Aug 25 2016German IFO Survey Fades

Summary

All components of the IFO index except construction demonstrated a significant monthly fade in August. The all sector index fell from 9.6 to 5.6. The manufacturing sector stepped back to 6.3 from 9.7. Wholesaling saw its reading [...]

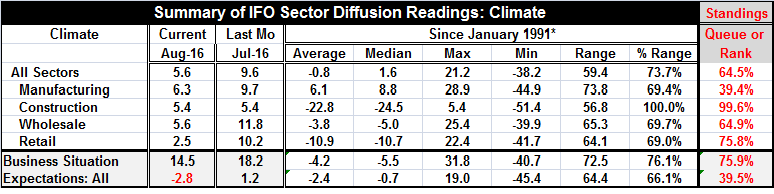

All components of the IFO index except construction demonstrated a significant monthly fade in August. The all sector index fell from 9.6 to 5.6. The manufacturing sector stepped back to 6.3 from 9.7. Wholesaling saw its reading chopped down from 11.8 to 5.6. Retailing reeled all the way back to a score of 2.5 from July's 10.2. The August readings for the IFO are not just lower but substantially lower. Perhaps this is the first glimpse of what German firms think will happen as the actual date for Brexit disruptions arises on the horizon. The U.K. is talking of making its exit filing in April of next year. That would mark the start of formal talks to leave the EU.

All components of the IFO index except construction demonstrated a significant monthly fade in August. The all sector index fell from 9.6 to 5.6. The manufacturing sector stepped back to 6.3 from 9.7. Wholesaling saw its reading chopped down from 11.8 to 5.6. Retailing reeled all the way back to a score of 2.5 from July's 10.2. The August readings for the IFO are not just lower but substantially lower. Perhaps this is the first glimpse of what German firms think will happen as the actual date for Brexit disruptions arises on the horizon. The U.K. is talking of making its exit filing in April of next year. That would mark the start of formal talks to leave the EU.

The all sector index was last weaker than its August value in February of this year. Manufacturing was last weaker in March. Wholesaling, which includes international trade, was last weaker in October 2014. Retailing was last weaker in December 2014. These are sizeable step backs in terms of months of progress lost.

The standings of the various sectors, except construction of course, also have fallen sharply. The all sector index now has a 64th queue percentile standing. It is stronger historically about one-third of the time. Manufacturing has a weak 39th percentile standing. Wholesaling has a 64th percentile standing. Retailing has a 75th percentile standing. Construction has a 99th percentile standing.

The business situation stepped back in August to a 14.5 reading from 18.2 in July. This step-back pulls the business situation back to a 75th percentile standing, a much more moderate positioning for the current situation. Expectations turned negative in August for the first time since April and the weakest since February. Expectations now have a very low 39th percentile standing.

The IFO took a huge step back in August. The wholesaling sector has fallen by more month-to-month only 4% of the time. Manufacturing has fallen by more month-to-month only 13% of the time. Retailing has fallen by more month-to-month only about 7% of the time. These are substantial and material changes in conditions as perceived by the firms engaged in these various lines of business. These are not third party surveys, but surveys of the principals. And they are now worried or at least much less confident.

Europe has a number of conditions to worry about. Global growth is weak and European growth is weak. The ECB is pushing hard on its monetary string with little results. A broad swath of interest rates is negative. Italian banks especially are in need of funding and there is no clear idea how they can get it since the new EU rules bar bailouts. Migrant issues continue to create disruptions of various sorts in European nations. And on top of it all is the U.K. pull-out from the EU.

Brexit is still going to be a difficult thing for all parties concerned. The U.K. has been the financial center for the EU even though the central bank is in Frankfurt. International lending occurs principally under U.S. or U.K. law- not French, not German, not Japanese, and not Chinese law. It is unclear how much of this strangle hold on lending that the U.K. has will be diminished by it being outside the EU. There is no precedent for diverting it. It is unclear how aggressively the EU will be treating the U.K.; the more it is `at an arm's length' the more that will make everyone suffer. It is not a good time to make everyone suffer. Yet, if the U.K. gets too-sweet a deal upon its exit, more countries might want to leave the EU and evade its requirements. This is not going to be easy. It is going to be messy. And the worst part does lie ahead when the untangling of these trade relations will be forced by the implementation of new rules mandating new treatment. And maybe for the first time, the IFO respondents have begun to focus on how all that will affect them.

The impact of Brexit on Germany, on the EU or even on the U.K. is not about `how markets react.' It will be about how the economies react when commerce finally will have to engage under very different rules, rules that are only now being contemplated and have yet to be drawn up let alone to have become effective. But this brave new world does lie ahead - somewhere. Right now it is just devilishly difficult to handicap.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief