Global| Feb 23 2015

Global| Feb 23 2015German Ifo Limps Ahead

Summary

The Markit flash PMI data showed some strength in the EMU but less of it is in France and Germany with the services sector leading the way in both nations. The German Ifo shows much the same situation, agreeing with Markit, with [...]

The Markit flash PMI data showed some strength in the EMU but less of it is in France and Germany with the services sector leading the way in both nations. The German Ifo shows much the same situation, agreeing with Markit, with manufacturing as the clear trialing sector according to queue rankings. That means setting aside the `absolute' diffusion readings. Manufacturing is weaker relative to its history than are other sectors.

The Markit flash PMI data showed some strength in the EMU but less of it is in France and Germany with the services sector leading the way in both nations. The German Ifo shows much the same situation, agreeing with Markit, with manufacturing as the clear trialing sector according to queue rankings. That means setting aside the `absolute' diffusion readings. Manufacturing is weaker relative to its history than are other sectors.

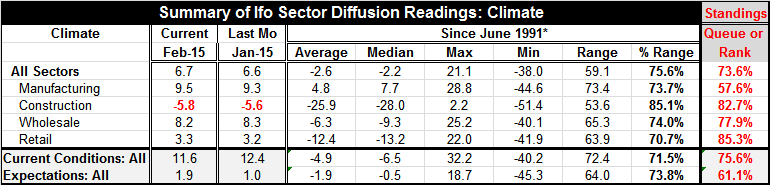

Climate in the Ifo framework ticked higher in February to 6.7 from 6.6, a barebones gain. As such, the climate reading stands in the 73rd percentile of its historic queue, a modestly firm reading. The current component weakened to 11.6 from 12.4 while the expectations diffusion advanced to 1.9 from 1.0. The current reading has a 75th percentile queue standing while expectations have a more modest 61st percentile standing. Expectations are better than this 39% of the time which is still a lot. But expectations are 11 queue percentile points above their historic median reading.

As to sectors, two improved and two eroded. Construction continues with negative readings and it worsened its degree of slippage slightly in February. Wholesaling's momentum stepped back by the smallest of margins. Retailing advanced faster by the smallest of margins while manufacturing gained two diffusion points on the month. Clearly February is a month of little change in Germany. The sector relative performance gauges show the best performance by retailing in its 85th queue percentile followed by construction in its 82nd and wholesaling in its 77th. Manufacturing is the relative weakest sector, standing in its 57th queue percentile.

As things stand, this is neither the prototypical German expansion nor the one we have been looking for. As Markit shows, Germany's services sector is the relative strongest and manufacturing is lagging. Yet, Germany is the most competitive country in the EMU and the euro exchange rate is falling well below most objective statistical measures of its purchasing power parity value. That should make Germany, the country with the smallest price level rise in the EMU history, its most competitive economy. And the German current account seems to bear this out. Yet, the German export sector is not fully engaged. Its manufacturing sector is still lagging.

Part of this dilemma is my looking at relative variables here like retailing which has the top queue score and manufacturing the lowest. In raw terms, manufacturing has the top diffusion score and retailing the second weakest. Still, we expect Germany's relative and absolute scores to improve with the euro's real exchange value so weak. The failure of the German external sector to score larger gains is a testament to ongoing problems in Russia and to the overall difficulty of operating in this global environment.

Some Fake Policies for Some Real Issues

After some initial glowing forecasts for 2015 based on lower oil prices, there have been many forecast pull backs based on the damage that is being done to the oil sector. In the U.S., the recent Fed meeting minutes reveal that Fed has had more concern that it had previously let on. The outlook for German output is still net higher. But there is a more fully established concern that the energy sector has been driving a good deal of global investment and with lower oil prices and weaker global growth and less energy demand. There is much less energy investment in need. With that sector's investment dial turned down, we find ourselves in the old familiar macroeconomic excess supply trap with too much output potential and not enough effective demand. Much of that stems from a shift in output to Asia where savings rates have been lower and consumption has been restrained as a matter of policy and where exchange rates continue to be maintained at levels that are below parity to support export growth and the acquisition of even more global production. It's the rat-race model whereby my rat steals your rat's cheese but does not eat it, and instead lends some of it to you so your rats don't starve, but then you owe me.

This is the international game that no longer works. Exchange rate configurations that worsen the balance of payments and cause the Asian surpluses to rise -or even the German surplus to rise- serve the world poorly. But that is exactly what has been in train. Surplus countries (countries running current account surpluses) need to add themselves to the ranks of those providing domestic demand growth to the global economy instead of siphoning off demand from abroad. Instead, the U.S. economy is adding its domestic demand to the world and continuing to run a current account deficit and one that is growing. The dynamics of this situation are unsustainable. But in the `short run' Europe and Japan are being allowed to pursue policies that weaken their exchange rates and pad their respective trade/current account surpluses. China is struggling to hold its growth rate at 7% and has `no aspirations' to let the yuan rise and erode its surpluses and growth prospects. But China needs to develop domestic demand because it has become too big and the West is too enfeebled to support China's growth target via export-led growth.

So we find China's transition all too slow, painful and lacking commitment. We find Europe and Japan pursing stop-gap unsustainable policies. We hope low oil price can keep consumer demand alive despite its puncturing of an important investment balloon globally. And we hope that the deflation of the balloon in the U.S. does not undermine the U.S. recovery where job growth appears strong but the quality of job created appears low. However, that job mix is a bad one for keeping U.S. demand improving in the face of all the pressures including the rising dollar which is now well above its true parity level. It's all a house of cards, not a well-oiled machine.

What we find are a number of policy choices living on `borrowed time' trying to drive growth by making existing imbalances worse. This is a good way to create another crisis. Although accumulated fiscal deficits are large, it is now monetary policy that is being stretched around the world. What happens when fiscal and monetary policy reach their limits of excess at the same time? Does anyone doubt but that there will be price to pay for this eventually? There is some return to leveraging already. The U.S. auto sector is the only one that has made a full economic recovery and that is only because it alone has gone back to the old habit of excess reliance on subprime loans.

Oh no, as the Wizard said, ignore that man behind the curtain. But is there really a great and powerful wizard that can put the odds ever in our favor for a happy ending if we continue on this path? Or are we simply careening from one crutch to another to keep growth in gear with certain tragedy lying ahead? I must declare my concern about the abject denial of all the global excesses and the unwillingness of the G-n (where n= some number from 3 to 20) which has had no capacity or backbone to deal with these issues. Every man for himself no longer works. Keeping everyone limping ahead from Greece to China to Japan to the U.S.A. itself, using any scheme possible is all too risky.

Riddles and Enigmas or Wampeters, Foma and Granfalloons?

How does any of this improve Europe's internal competiveness? Is Greece really going to be able to stay in the EMU? Is it really willing to keep with the program or is Europe just stringing it along and throwing more good money after bad? Can Greece really carry all that debt? When and how will Germany allow its trade surpluses to fall to an internationally tolerable level? How will that happen with its insistence on being the low inflation nation in the EMU year-in and year-out? How does the U.S. survive and how does it keep its growth rate up with its deficits rising and competiveness undercut by a rising dollar and growing current account gap while U.S. energy investment is smacked back by the Saudis? Why is a desert Sultanate dictating policy to the US when the US has the ability for its own energy dependence? What inmates are ruing this asylum? Whatever happened to economic rules and principles? Why has `floating exchange rates' turned to such a `managed float'? Why do so few care that the system no longer bears any resemblance to one that could support true free trade? And given that why do people think trade expansion is good thing and not bad thing since NOTHING is being done along the lines of true comparative advantage when exchange rate are misaligned so badly? Riddle me that.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief