Global| Nov 22 2013

Global| Nov 22 2013German Ifo Fills Out

Summary

Germany's Ifo continues to power higher. It is engaged in its second upswing in its cyclical recovery since the end of the financial crisis. In this `second wave up' the Ifo is locked into a milder upgrade that it had earlier, but the [...]

Germany's Ifo continues to power higher. It is engaged in its second upswing in its cyclical recovery since the end of the financial crisis. In this `second wave up' the Ifo is locked into a milder upgrade that it had earlier, but the upgrade is still marking steady progress as the chart demonstrates.

Germany's Ifo continues to power higher. It is engaged in its second upswing in its cyclical recovery since the end of the financial crisis. In this `second wave up' the Ifo is locked into a milder upgrade that it had earlier, but the upgrade is still marking steady progress as the chart demonstrates.

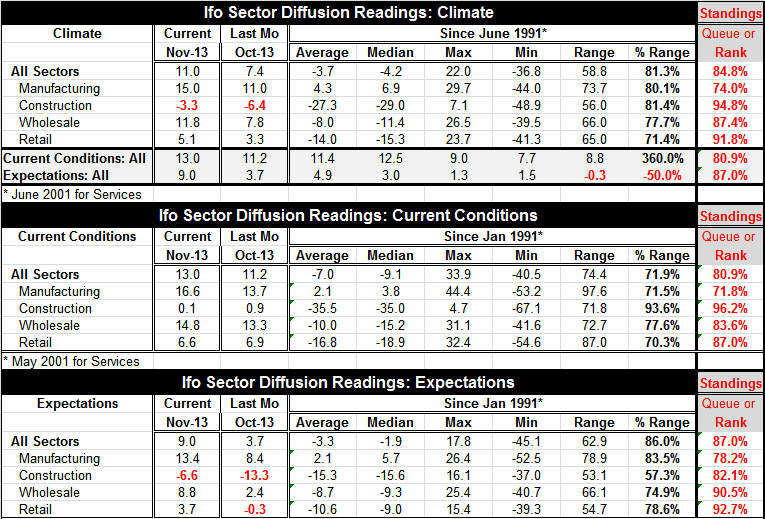

The steady improvement is now extremely widespread. Virtually all main Ifo sectors now have solid standings. The all-sector climate index rose to +11 in November from +7.4 in October. The standing for overall climate is in the 84.8 percentile of its queue. The sector percentiles range from a high of 94.8% for construction to a low of 74% for manufacturing.

The current conditions index rose to 13.0 in November from 11.2 in October. The current conditions barometer stands in the 80.9 percentile of its historic queue- it has been higher less than 20% of the time. The strongest sector in terms of its current standing is construction again, at the 96.2 percentile of its historic queue. But the bottom is defined by manufacturing in the 71.8 percentile of its historic queue.

Expectations are where the real strength is for the Ifo this month. While the November reading at 9.0 is below the current reacting for November which stands at 13.0, the 9.0 reading for expectations is a stronger reading in the sense that it is at a higher standing in its historic queue than does the current reading in its queue.

The expectations index that rose to 9.0 in November from 3.7 in October stands in the 87th percentile of its historic queue; it has been higher only 13% of the time. Retailing expectations are in the 92.7 percentile of this historic range with wholesaling also in the 90th percentile range. The weakest sector is manufacturing in its 78th percentile.

Perhaps the best news in this Ifo survey is that the retail sector now has the strongest expectations. Its current standing is also quite good at the 87th percentile, but the strength in expectations is even better. Germany needs to consume more for the good of the EMU whose members need a pick-up in consumption to help propel output. Many are still under the yoke of austerity. Notice that is not the way the German economy works. Retailing is strong on the relative gauge (percentile standing), but it is still the second weakest outright diffusion reading among sectors for expectations. Retailing is doing the best on expectations in relative terms- not absolute terms. Still it's progress. Europe is making progress and Germany is a big part of it.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief