Global| Jun 24 2019

Global| Jun 24 2019German IFO Erodes; The Mixed Message from Rankings Data Continues

Summary

With concern mounting about the state of growth in the global economy, all incoming reports are being scrutinized for signs of which way growth may be turning; is it improving or deteriorating? The German IFO report gauges are plotted [...]

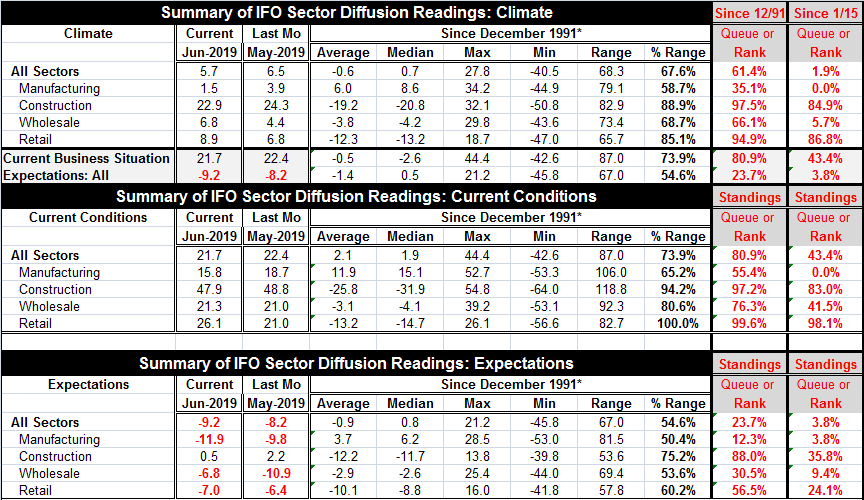

With concern mounting about the state of growth in the global economy, all incoming reports are being scrutinized for signs of which way growth may be turning; is it improving or deteriorating? The German IFO report gauges are plotted as indexes in the chart and presented as diffusion values in the table. The report shows a clear deteriorating trend.

With concern mounting about the state of growth in the global economy, all incoming reports are being scrutinized for signs of which way growth may be turning; is it improving or deteriorating? The German IFO report gauges are plotted as indexes in the chart and presented as diffusion values in the table. The report shows a clear deteriorating trend.

In June, two of four sector climate readings deteriorated. Current conditions improved in two of four sectors and deteriorated in two others. Expectations also weakened in two of four sectors; not the same two sectors.

The top climate panel of the charts shows the overall sector gauge weakened on the month, falling to a net diffusion reading of 5.7 in June from 6.5 in May. It has a 61.4 percentile standing over data since 1991; however, over the period since 2015 to date, the ranking is on its 1.9 percentile, very weak. The climate standing is above its median since 1991, but it is extremely weak on data from 2015. Obviously, the period since 2015 has been a relatively strong one since the June reading is weak when compared that that string of data, but moderate when evaluated over a longer stretch. A look at the chart confirms that assessment.

Climate

The manufacturing reading is on its low since 2015 but has a weak 35.1 percentile standing on climate data back to 1991. Construction and retailing climate are still strong under either set of rankings. Wholesaling is moderate compared to the long period and weak compared to the shorter one.

The current situation and expectations overall

The overall current situation has an 80.9 percentile standing on data back to 1990 but a standing below its median with a 43rd percentile standing since 2015. Expectations are poor on either comparison a 23.7 percentile standing for since 1991 and a 3.8 percentile standing on expectations since 2015.

Current situation sectors

Looking at current conditions, manufacturing is extremely weak in the shorter period and of moderate standing over the longer period. Service sector and construction gauges are generally firm to strong with strong readings when compared to the longer timeline and weaker readings on the shorter time line.

Expectations by sector

Expectations show only one strong reading on the long timeline and that is for construction. Manufacturing is still very weak on both timelines. Wholesaling is below its median for both. And retailing resides just above its median reading on its long period comparison. But since 2015, all expectations measures rank as weak.

Summing up

The declining momentum on all the comprehensive climate current and expectations readings is quite clear. The IFO is showing degradation in its trend. But the overall current business situation is still quite solid when viewed most broadly even though expectations are weak.

The IFO, therefore, does not reassure us much about the future. For now Germany is still giving off tolerably solid readings, but momentum is negative and expectations are poor. The readings are extremely weak by the standards we have been used to over the past five years or so. The IFO will not be reassuring to the ECB.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief