Global| May 22 2015

Global| May 22 2015German GDP Finalizes Slowdown

Summary

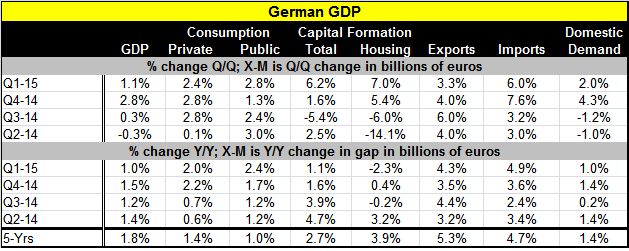

German GDP is now finalized. It is up at a 1.1% annual rate in Q1 2015 and at a 1.0% pace year-over-year. Both growth rates represent slowdowns from the previous quarter. Perhaps the most perplexing thing about the German economy is [...]

German GDP is now finalized. It is up at a 1.1% annual rate in Q1 2015 and at a 1.0% pace year-over-year. Both growth rates represent slowdowns from the previous quarter. Perhaps the most perplexing thing about the German economy is that, even with the euro exchange rate so low, German manufacturing and exports have not been quick to respond to the advantage represented by the weak euro exchange rate.

German GDP is now finalized. It is up at a 1.1% annual rate in Q1 2015 and at a 1.0% pace year-over-year. Both growth rates represent slowdowns from the previous quarter. Perhaps the most perplexing thing about the German economy is that, even with the euro exchange rate so low, German manufacturing and exports have not been quick to respond to the advantage represented by the weak euro exchange rate.

Today the German Ifo survey shows a slight setback to business confidence. Earlier this month, the ZEW financial experts registered a sharp drop in their expectations. As GDP trends show, Germany is not accelerating despite circumstances that should be favorable to the German economy. And that is reflected in economic measures from ZEW, Ifo and Markit.

German GDP saw private consumption step back a bit in Q1 on a quarterly basis as public consumption increased Year-over-year, however, private consumption decelerates while public consumption gathers momentum. Total capital formation and housing surged in Q1, but on a year-over-year basis both continue to decelerate. Exports, despite a weak euro, are weaker in the quarterly data while year-over-year German export growth is only in line with past trends. German imports have sped up generally over the last four quarters and on year-over-year gauges.

Overall German domestic demand tailed in Q1 compared to Q4 although both those quarters represented a pick up from the two previous quarters. But on year-over-year growth we see domestic demand simply stuck at growth rates near 1% compared to a five-year average of 1.4%.

All the GDP components sport year-over-year growth in Q1 2015 that is below their respective five-year growth rates except for domestic consumption, government consumption and imports. Imports are only slightly faster than their average five-year pace, while public consumption is more than twice as strong as its previous average and private consumption is nearly 50% faster. Germany has been led by its consumption spending, especially public spending.

Looking at year-over-year trends, few things are clear. One is that capital formation has been slowing. Another is that imports have been accelerating slightly. Private consumption is stronger over the last two quarters, but that is not a very certain trend. German public sector consumption has been creeping higher steadily. These trends do not give us much to be confident about. Typically, Germany is led by its manufacturing sector and benefits from export-led growth. The trends we see here do not tap into those traditional sources of strength. The Markit PMI data tell us that the German economy is being led ahead by its services sector, not by manufacturing. As if to underscore that, German capital formation is slowing sharply.

Germany certainly is hurting from weakness in two of its important export markets: Russia and China. Another chunk of its exports stay within the EMU and do not benefit from the weak euro exchange rate. Still, German competitiveness within the euro area remains top-notch. But when economic growth hits hard times competiveness usually is not enough compensation to hold the line on export growth. This is Germany's lesson. Weak global growth and the fact that services sector also is leading growth in the EMU finds Germany lost in a world where its competitive powers are not helping it as they have in the past. It's as though superman has discovered kryptonite. Germany is growing, but it is not thriving and it is leaning heavily on public consumption.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief