Global| Mar 28 2017

Global| Mar 28 2017German Federal Debt Levels Fall

Summary

German debt level fell outright in Q4 2016 as the ratio of federal debt-to-GDP also fell. Germany has the lowest ratio of debt-to-GDP among the original EMU members with the exception of Luxembourg, a small country that is a financial [...]

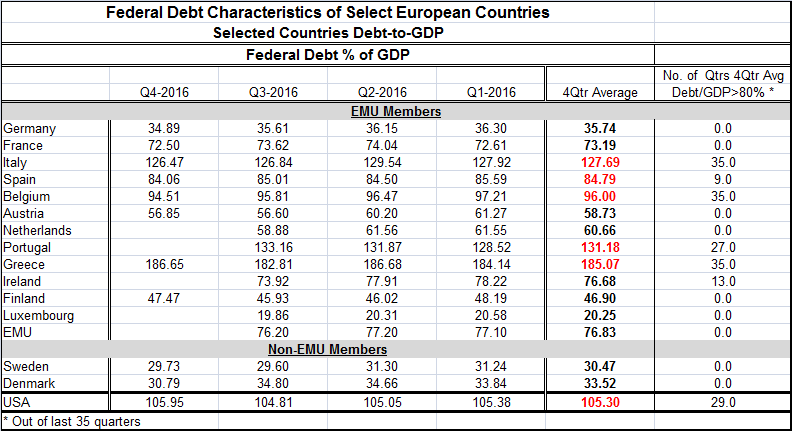

German debt level fell outright in Q4 2016 as the ratio of federal debt-to-GDP also fell. Germany has the lowest ratio of debt-to-GDP among the original EMU members with the exception of Luxembourg, a small country that is a financial center. After Germany's debt ratio to GDP of 36% (I use Q3 ratios since all have reported in Q3), the next lowest ratio is Finland (46%) whose position is helped by its oil sector. After that, the ratios rise to Austria at 57% and the Netherlands at 59%.

German debt level fell outright in Q4 2016 as the ratio of federal debt-to-GDP also fell. Germany has the lowest ratio of debt-to-GDP among the original EMU members with the exception of Luxembourg, a small country that is a financial center. After Germany's debt ratio to GDP of 36% (I use Q3 ratios since all have reported in Q3), the next lowest ratio is Finland (46%) whose position is helped by its oil sector. After that, the ratios rise to Austria at 57% and the Netherlands at 59%.

At the high end, we have Greece at 183%, Portugal at 133% and Italy at 127%. Below Italy is Belgium at 96%. Placed on this same grid, the U.S. Federal debt-to-GDP ratio is 105% in Q3. It is high ranking just above Belgium and below Italy among EMU members. And U.S. policy is gearing up to reduce taxes. It is not so clear to me that it is a good idea for the U.S. to plan to use economic stimulus with federal debt ratios so high, and a coming demographic bulge that will increase demands on government spending at a time that inflation pressures might make existing fiscal indebtedness even more of a burden. But such is policy. European policy has its own challenges.

Debt of course can be a huge overhang on a country's fiscal position as debt service payments will come to absorb a good deal of government revenue if debt levels relative to GDP are too high. However, in our current unusual period countries' debt payments have been kept low by ongoing low inflation and by the persistence of low rates owing to central bank policy and market dynamics. While central banks have led rates lower, the yield curve is hardly protesting what central banks are doing.

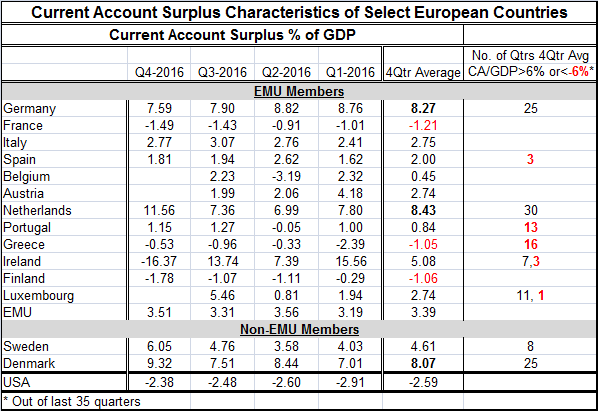

Germany continues to run a very large current account surplus as ratio to GDP. It is the largest such imbalance in the world among developed economies and it has been quite large for some time. The combination of paying down fiscal debt and running large current account surpluses has not exactly made Germany a good neighbor in the EMU at a time that domestic demands have been wanting across Europe. German debt levels were rising relative to GDP in the immediate aftermath of the financial crisis, but by 2012 Germany was getting control of its debt and stabilizing it relative to GDP and actually reducing it as other EMU members were put on their own programs of imposed austerity. Germany mimicked the process of austerity back home rather than to use its low debt-to-GDP ratio to provide policy flexibility to help provide further demand stimulus to ease the pain in the rest of the EMU. In fact, Germany's current account surplus has been expanding steadily until very recently a fact that implies that Germany has been living off the fat of the land in terms of other countries' domestically generated demand and doing it at a time when there has been little such fat.

Nonetheless, the process of austerity has helped to bring member current accounts back into line in the EMU after being in such disarray. The standard deviation of the current account positions relative to GDP has fallen from near 8 in 2008 to a current low of 3.2. Still, not only do structural differences remain, but they still look rather well-entrenched. However, Germany has been protesting the recent focus on its massive surplus and contends that it is already in the process of being reduced.

In these data on federal debt and current account deficits, we get a good look at why the euro area continues to have troubles. Its members have very different views on what constitutes good economic policy. Even with rules restricting debt and deficit behavior, some large differences and imbalances have developed in this region where harmonization- ostensibly- has been the watch-word. As much as Europe likes the notion of being a single bloc in some respects, it at the same time abhors the idea of having a common fiscal policy. As some recent unfortunate statements made by various euro-members has shown, there are still deep divisions, animosities and distrust about how some members handle their financial affairs. Many members simply do not want to mix their financial futures with such. And with such deep government debt and current account differences, economic policy is going to wash across these countries in a very uneven way.

While Europe is trying to reflate, the low inflation rate has actually been a godsend for the likes of Italy with its huge debt-to-GDP ratio. Once inflation and interest rates start rising, Italian fiscal deficits are going to be much harder to deal with. Meeting deficit objectives will require cutting public expenditures that Italy will not want to cut.

In some ways, Europe is 'much better off' with such weak economic performance and a lack of inflation. Once inflation takes hold and rates rise forcing interest rates back up to normal levels, the various debt ratios across the EMU are going pose a different pressure across members' budgets.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief