Global| Jul 08 2016

Global| Jul 08 2016German Export and Import Flows Decay

Summary

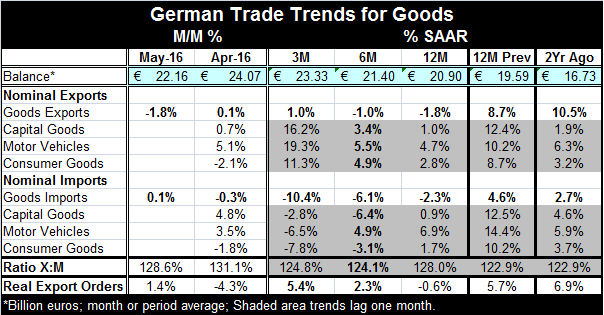

Germany's trade surplus contracted slightly in May, but the surplus remains huge. German exports fell by 1.8%, marking their largest drop in nine months. German imports ticked higher by only 0.1% in May after a 0.3% decline in April. [...]

Germany's trade surplus contracted slightly in May, but the surplus remains huge. German exports fell by 1.8%, marking their largest drop in nine months. German imports ticked higher by only 0.1% in May after a 0.3% decline in April. German domestic demand is not hitting any home runs or scoring any goals for the rest of Europe.

Germany's trade surplus contracted slightly in May, but the surplus remains huge. German exports fell by 1.8%, marking their largest drop in nine months. German imports ticked higher by only 0.1% in May after a 0.3% decline in April. German domestic demand is not hitting any home runs or scoring any goals for the rest of Europe.

The chart shows how year-on-year export and import flows are withering. These trends should be disconcerting. They show a slowing in German domestic demand (weak imports) and in foreign demand generally (weak exports).

Decline and Deceleration

German export and import flows not only are declining but within the 12-month framework the weakness is intensifying. Their growth rates are progressively weaker over shorter periods. The weakness is not just present, but it is cumulating.

The ratio of export to imports is off its peak but still quite elevated. Perhaps the only really `good news' is a bit of old news from real export orders that shows real export orders still are advancing despite these poor trends for past export and import performance. Real export orders are even accelerating. That is the only silver lining here because the trends are simply very disturbing.

Trailing data on export and import components show actually quite solid one-month-delayed German three-month growth rates for the exports capital goods motor vehicles and consumer goods exports from Germany. But those same groups show declines for nominal imports on the same one-month delayed three-month horizon.

Trade flows elsewhere are weak

All of the early reporters of exports for May, the U.K., Germany, the U.S. and Japan except France (where exports are up 0.9%) show declines in exports in May as well as over 12-months (even France shows a 12-month drop). Trade is simply not a bright spot internationally.

International environment remains weak

The intentional news simply is not very good today. The key June U.S. jobs report did post an outsized gain of 287,000 jobs but did so after a very weak May. U.S. job growth is still slowing along with hours worked; wages are weak and the unemployment rate moved higher in June to boot. In Japan, the economy watchers index fell to a 24 month low. In the U.K., permanent jobs placements fell for the first time in 45 months. U.K. consumer sentiment, the first reading since the Brexit vote, fell sharply to -9 in July from -1 in June, logging the biggest monthly decline since 1994. Yes, there are headwinds out there. There is a great deal of global weakness and even traditionally faster-growing trade flows are not able to put a better face on the state of global conditions.

Sideshow

But perhaps the most important side show to watch will be in Europe where Spain and Portugal have failed to hit their budget targets and are at risk to having sanctions imposed for not reaching their prescribed goals. The OECD is urging the European Commission to not impose sanctions on Portugal and Spain because `it's the last thing we need.' Of course it has been exactly that kind of mindless no exception and no holds-barred implementation of `The Rules' that has created hostilities in the euro area. The Germans typically do not like exceptions and believe in enforcing rule scrupulously. This will be something to watch. In the wake of the U.K. Brexit imbroglio, it would be a bad time indeed to penalize Spain and Portugal for missing budget targets in such a hostile global environment. Stay tuned.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.