Global| Aug 27 2014

Global| Aug 27 2014German Consumer Confidence Finally Slips

Summary

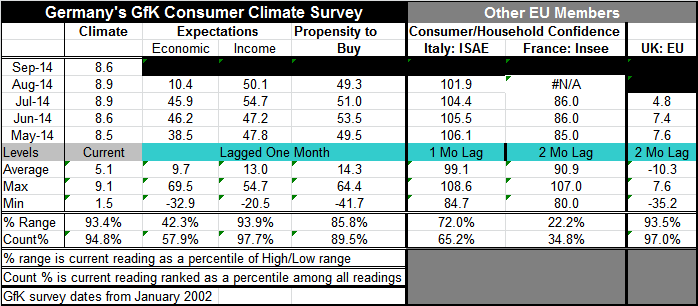

Germany's consumer climate rating for September fell to 8.6 from 8.9 in August. The drop is the first since January 2013. The climate reading fell by 0.3 percentage points, which is the largest drop since May 2011 (more than three [...]

Germany's consumer climate rating for September fell to 8.6 from 8.9 in August. The drop is the first since January 2013. The climate reading fell by 0.3 percentage points, which is the largest drop since May 2011 (more than three years ago). The disturbance to the ongoing climb of the German consumer climate reading is an unusual event in the context of recent German statistics that have been a juggernaut of strength.

Germany's consumer climate rating for September fell to 8.6 from 8.9 in August. The drop is the first since January 2013. The climate reading fell by 0.3 percentage points, which is the largest drop since May 2011 (more than three years ago). The disturbance to the ongoing climb of the German consumer climate reading is an unusual event in the context of recent German statistics that have been a juggernaut of strength.

GfK estimates confidence in the month ahead. We have, however, details for the index only through August, and what we have is quite telling. Although the August reading for climate was unchanged at 8.9, the same level as July, economic expectations fell sharply to 10.4 in August from 45.9 in July. This is an exceedingly sharp drop in that indicator, pulling it down to the 57th percentile of its historic queue.

Also in August we have data for income expectations that fell to 50.1 from 54.7. The 54.7 reading of July was quite a jump from June's level of 47.2. The setback to 50.1 in August still leaves the index above its June level by a substantial margin. As a result, the income metric stands in the 97th percentile of its historic queue; still an exceptionally high reading.

The final GfK component is the propensity to buy reading. In August the propensity to buy index fell to 49.3 from 51.0 in July. The propensity to buy had also fallen in July relative to June to 51.0 from 53.5. As a result, this drop in the propensity to buy in August brings the measure down below its May level. But the propensity to buy still has a relatively high standing in historic context. It stands in the 89th percentile of its historic queue (weaker only 11% of the time).

We see in this report the evidence of slippage at all three of the components in August. We see some ongoing slippage in the propensity to buy and we see a sharp drop in economic expectations.

Comparing German consumer confidence measures to confidence measures elsewhere, we have, in the right portion of the table, the readings from Italy, France and the U.K.

The Italian reading fell to 101.9 in August from 104.4 in July; it is making a steady string of declines, but fell relatively more rapidly in August. Italian consumer confidence is down to 65th percentile of its historic queue. This is a level of moderate strength as neutrality on this measure is at the 50th percentile.

The French reading is updated through July. At 86, it's flat for two consecutive months. French consumer confidence stands in the 34th percentile of its historic queue. This is a very weak reading, barely above the lower third of its historic queue of data. France has been struggling economically; recently its economic difficulties have become political difficulties and have caused a reshuffling of the government.

The U.K. data also are updated through July at which time its confidence measure had fallen to 4.8 from 7.4 in June. Like Italy, the U.K. confidence measure has been slipping in recent months. Even so, the queue standing of the U.K. consumer confidence indicator is in the 97th percentile of its historic queue. This means that it's higher historically only about 3% of the time, marking this is a still very strong level, despite its relatively significant month-to-month fall.

Taking these indicators together, we see that there is a weakening of consumer attitudes in recent months. The U.K. and French data that are updated through July, Italy's data are updated through August, and Germany's are updated through September. Despite these different end points, we see slippage in each of these countries. Germany's consumer climate has been increasing almost inexorably in recent years. As we pointed out, the last decline of any sort for German consumer climate was about 20 months ago. Other euro area countries show confidence at much lower relative levels in historic terms. The U.K., however, has a confidence reading in relative terms that is even stronger than Germany's.

We know there's been some economic slippage in the euro area; we've seen it in a variety of indicators even in the most up-to-date PMI metrics from Markit. The slipping consumer confidence is evidence that consumers are aware of the dangers and risks to their economies from the weaker economic data and they undoubtedly see the cause which has gone beyond some normal stumbling of an economic recovery process and become entangled in geopolitical confrontations.

There is, as I write this, an ongoing summit between Ukraine and Russia. In an early statement from President Vladimir Putin, he suggests that Russia views these talks as potentially constructive. But the Russian take on the geopolitical events in the area has been unwilling to confront the facts as most of us know them. Russia does not admit to any incursions into Ukraine except to deliver humanitarian aid. The recent capture of Russian soldiers on Ukraine ground was explained up by Russia as bad map reading. If this is going to be the approach that Russia takes at the summit, regardless of the nice jargon from Putin, the summit is unlikely to be productive and we will have continuing concerns about the impact of Ukrainian situation on the economies of Eastern, Western and Northern Europe.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief