Global| Dec 22 2020

Global| Dec 22 2020German Confidence Is Sliding on a Slippery Slope

Summary

German confidence in the GfK survey has gone from a highflying set of optimistic readings prior to the Covid-19 crisis to a weak wobbling and slipping assessment of German welfare. The index that assesses economic climate on a scale [...]

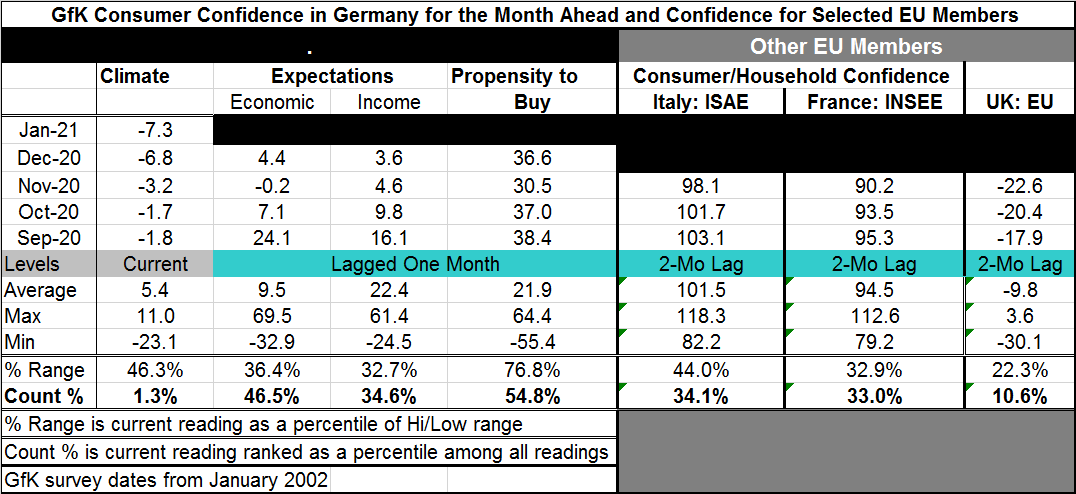

German confidence in the GfK survey has gone from a highflying set of optimistic readings prior to the Covid-19 crisis to a weak wobbling and slipping assessment of German welfare. The index that assesses economic climate on a scale back to 2002 has been weaker than its projected January reading only 1.3% of the time. When Covid-19 infections struck Germany, this index slipped to a low of -23.1, the hands-down low point in this series. It since sprang back to get as high as -0.2 in August, but since August the assessments have been weakening pretty much month-by-month to -7.3 in January.

German confidence in the GfK survey has gone from a highflying set of optimistic readings prior to the Covid-19 crisis to a weak wobbling and slipping assessment of German welfare. The index that assesses economic climate on a scale back to 2002 has been weaker than its projected January reading only 1.3% of the time. When Covid-19 infections struck Germany, this index slipped to a low of -23.1, the hands-down low point in this series. It since sprang back to get as high as -0.2 in August, but since August the assessments have been weakening pretty much month-by-month to -7.3 in January.

The components for the GfK index generally hit their respective lows one month ahead of the headline. Although two of the three GfK components reached their recovery peaks (so far) a month after, the headline had turned lower (the propensity to buy index has been on a similar profile with the headline).

The 'spread' in Germany and the U.K.'s new outbreak But in Germany on the ongoing spread of the virus remains serious and currently Europe is trying to sort out how it will interact with the U.K. as a new seemingly more contagious strain of the virus seems to have emerged. The first step was to shut out U.K. arrivals as 40 countries announced that step. The borders then were shut to the flow of goods. Today the EU is trying to recommend opening borders to merchandise and to the return of people back to their homes. It is not clear if that is going to hold sway or not. For the time being, the U.K. is quite thoroughly and unexpectedly isolated. Maybe some of the planning in expectation of a no-deal post-Brexit trade arrangement will help it weather this development.

GfK components

By comparison, the GfK components are clearly not as weak as the GfK headline with count or rank standings in their 46.5 percentile for economic expectations, 34.6 percentile for income expectations and an above-median 54.8 percentile for the propensity to buy. While these reading are not in the same dregs as the GfK headline, two of them are still extremely weak readings. The sense of trend among the components, however, is in state of chaos; it is not possible to tell which way they are going. The headline has worsened for three months in a row. This compares to the component income expectations that also is weakening for three months in a row while both economic expectations and the propensity to buy increase for only one month.

Elsewhere in Europe

Italy, France and the U.K. all have confidence readings that lag the look-ahead German reading by two months. In general, they continue to show weakening conditions from September to October to November. The November standing for these three European nations are in their 33rd and 34th percentiles for EMU members France and Italy, respectively, with the U.K. scraping by at a 10.6 percentile standing – a reading that does not yet reflect the emergence of a new strain of the Covid-19 virus and the stepped up spread of the disease that is currently sweeping through the U.K.

The virus rules

Of course, these economic and confidence or climate assessments are mostly about the virus. The metrics seem to pertain to certain economic conditions, but those conditions are totally controlled by what the virus is doing and how the political environment is reacting in response to it.

The U.K. – a bizarre litmus test

The U.K.'s current situation is telling. While the U.K. and the EU continue to bargain hard over their post Brexit relations, the new virus strain in the U.K. has thrown a wrench into the works. Europe's initial response to this new virus strain was to red-line the U.K. to stop the spread. That is not surprising given that the U.K. is separable from Europe owing to the channel (with the minor exception of the tunnel). However, an unexpected border closure creates a good deal of angst for any traveler of any nationality. And an unanticipated closure of the border for shipping goods is a disaster of a high order of magnitude for parties on either side of those borders. Germany trades a lot with the U.K. This is not just important for the U.K. It is something we should watch closely. Since the vaccine is coming, there may not be any replication of this problem. But that depends a lot on how vaccine manufacturing and distribution go and on the in-situ performance of the vaccine.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief