Global| Oct 26 2016

Global| Oct 26 2016German Confidence Expected to Retreat

Summary

German consumer confidence for all intents and purposes peaked back in 2015. Then it swooned and recovered in 2016 to recover that peak, but now it is on the decay again. GfK does a look-ahead assessment of German confidence. That [...]

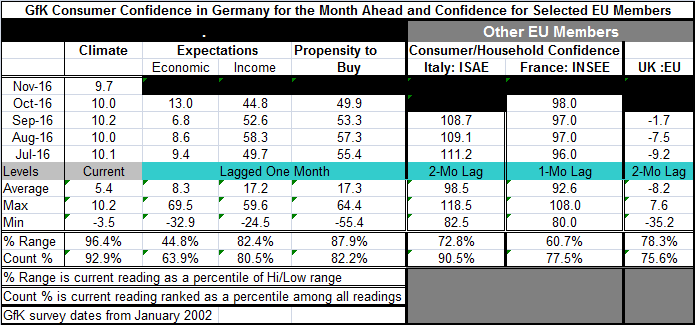

German consumer confidence for all intents and purposes peaked back in 2015. Then it swooned and recovered in 2016 to recover that peak, but now it is on the decay again. GfK does a look-ahead assessment of German confidence. That index sees a drop to 9.7 in November from 10.0 in October. A 9.7 reading will be the weakest reading since May. Prior to May, the GfK index had been in the 9.3 to 9.5 range for a period of six months. In the five months before that, it was on the same 10-plus plateau it is falling off now in 2016.

German consumer confidence for all intents and purposes peaked back in 2015. Then it swooned and recovered in 2016 to recover that peak, but now it is on the decay again. GfK does a look-ahead assessment of German confidence. That index sees a drop to 9.7 in November from 10.0 in October. A 9.7 reading will be the weakest reading since May. Prior to May, the GfK index had been in the 9.3 to 9.5 range for a period of six months. In the five months before that, it was on the same 10-plus plateau it is falling off now in 2016.

GfK components lag and economic expectations jump

The GfK components lag the headline by one month. Its components for October show a relatively sharp gain in economic expectations for October. They posted their strongest reading since June in October and their second strongest economy reading since August 2015. The gain on the month was strong enough that the index has gained by more monthly only about 25% of the time. Yet, in October the GfK index already was slipping from its peak and it has continued to slide in November.

Income weakness

October brought weakness to the GfK income component. It fell sharply to 44.8 in October from 52.6 in September. That drop took it back to the 80.5 percentile of its historic queue of data. Its month-to-month change was bad enough that the sub-index monthly drop has been worse historically less than 10% of the time. The Index slipped so severely that it was last lower in November 2015 and this is the second lowest reading since December 2014.

Propensity to buy also slips

The GfK buying climate index also fell in October to 49.9 from 53.3 in September. That reading has an 82nd percentile standing in its historic queue of data. The monthly drop in the buying climate index is greater about one quarter of the time. The buying climate itself was last weaker in March and in a series of months late in 2015 as well. Its fall off is the least dramatic.

GfK Sum-up

On balance, with the exception of the economy index, there appears to be some serious erosion in the German confidence picture. And even for economic expectations, while the October reading was a jump and a surprise, it still has the weakest standing among components in its historic queue at its 63rd percentile compared to readings in the low 80th percentiles for income and the propensity to buy.

GfK vs. Other Europe

The GfK headline is still very strong itself sitting in its 92nd queue percentile in November well above the queue standings of its three components. The component rankings are far more similar to confidence readings in two of the three large European economies we show in the table, Italy, France and the United Kingdom. U.K. confidence lags by two months. Its September reading is still recovering from the shock of the Brexit vote. It rises to -1.7 in September from a low reading of -9.2 in July. Italy's measure lags GfK by two months as well. Its reading in September represents its second straight monthly drop and reduces the headline to a surprisingly strong 90.5 percentile standing- not too different from that of the Germany's GfK headline itself that has 92nd percentile standing. Despite all sorts of economic problems, political conflicts and banking sector woes, the Italian consumer remains surprisingly upbeat. In France, confidence bumped up this month to a 77.5 queue percentile. That is not too different from the U.K.'s 75.8 percentile standing or the standing in October for the German GfK components (low 80th percentiles).

What we learn about growth

While yesterday's (German) IFO report was surprisingly strong, the look-ahead consumer index from GfK suggests that the IFO is not signaling some new surge in the German economy. The confidence measures for the other large European economies do not seem to be signaling any change in circumstances either. Italy continues to surprise with a strong confidence measure. The U.K. continues to recover from its Brexit low helped by the collapse in the value of the pound sterling. France is still just France, continuing to underperform but to grow. These observations also jibe with the Markit sector indices released earlier in the week. Those sector indices suggested that some manufacturing sector rebound was in play but did not show any trend improvement in place to bolster confidence in a new more upbeat trend. The services sector in Europe remains as issue. On balance, consumers seem to be just marking time among a series of disparate trends.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief