Global| May 27 2021

Global| May 27 2021German Climate Improves Slowly As Expectations Lead the Way Higher

Summary

The GfK climate index as estimated for June rose to a -7 reading. This lifts the reading to its lifetime standing at its 3rd percentile – still extremely weak. The components of the index lag by one month. Even so, economic [...]

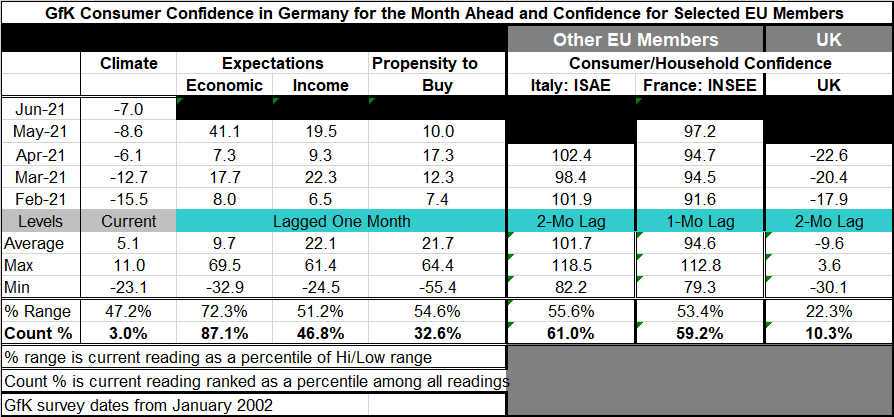

The GfK climate index as estimated for June rose to a -7 reading. This lifts the reading to its lifetime standing at its 3rd percentile – still extremely weak. The components of the index lag by one month. Even so, economic expectations rose very strongly to a value of 41.1 in May from 7.3 in April and to an 87.1 percentile standing.

The GfK climate index as estimated for June rose to a -7 reading. This lifts the reading to its lifetime standing at its 3rd percentile – still extremely weak. The components of the index lag by one month. Even so, economic expectations rose very strongly to a value of 41.1 in May from 7.3 in April and to an 87.1 percentile standing.

Despite the rise in the climate index, it is the 9th lowest reading in its history and is improving far more slowly than its components. Income expectations have risen to 19.5 in May from 9.3 in April to a 46.8 percentile queue standing. The buying index receded in May, falling to 10.0 from 17.3 to a below median 32.6 percentile standing.

Germany is improving. Its virus new case and death count curves are falling. These trends should underpin ongoing improvement in the German economy and in its climate index.

Elsewhere in Europe

The confidence measures for Italy, France and the United Kingdom provide some perspective. They all lag the forward-looking German GfK headline index. Italy and the U.K. even lag the German components in terms of their timeliness. These other European gauges show improvement in Italy and France but a setback in the U.K. Italy logs a queue percentile (or rank) standing in its 61st percentile above its median on the same timeline as the German GfK reading. On that same timeline, France has a similar 59.2 percentile queue standing, but the U.K. has a very weak 10.3 percentile standing.

The virus

Virus trends show new cases and deaths trending lower in France and Italy. The U.K. has reduced its infection and death rate even more substantially. However, the UK is dealing with Covid-19 issues as well as ongoing Brexit adjustments.

The virus is in retreat and it is looking less like the increasingly vaccinated developed economies are much less at risk. New studies show that infections among those who have been vaccinated –fully vaccinated- are rare and death after vaccination is extremely rare. Vaccinations are working and will aid growth but the developing economies have populations much less vaccinated and much more at risk and there are lingering questions about new variants, their trends and their eventual potency.

Fiscal policies and central banks

Beyond those issues the new focus is turning to central banks tapering and how countries will exit their extreme polices of fiscal stimulus.

Improving trends are in place and there is optimism. But there remains risk. Consumer confidence gauges show that there has been improvement but still a good way to go to restore growth to where it was. Germany is still lagging, but its economic expectations are moving strongly higher. Even so, the backtracking in the buying index this month is a reminder that the path is unlikely to run straight and true to a full recovery.

Remember that as the virus struck in early 2020, global interest rates were still extremely low. Only the U.S. had hiked rates since the Great Recession and had room for rate reductions before turning to QE (or large-scale asset purchases). The stimulus is putting growth back on track, but government interventions in the local economies to support the dislocated also are creating new issues and uncertainties for future policy. Central banks are grappling with the standards they should wait to see before trying to normalize their approach.

The China factor

The behavior of the Chinese by delaying for over a year then impeding the WHO investigation and now trying to blame some other unknown country as the cause of the virus has exposed exactly the depths to which China will stoop to avoid facing any fair inquiry. China seeks to control Taiwan and it has dismembered the democratic elements the British had installed in Hong Kong that China once had promised to respect. China seized and still attempts to own and to bully others over control and the rights of passage in the South China Sea. China was the source of the much needed medical supplies for the rest of the world as the pandemic struck. It did not work out. Global supply chains are being reset as multinational corporations are rethinking the lessons of depending on Japan’s just-in-time inventory techniques in the face of rising trade impediments and increasing global tensions. That approach now has to be reevaluated in a world where commerce no longer flows smoothly and where a good deal of trust has been lost. The post Covid-19 world is going to be different. We are still in the process of finding out how different it will be.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief