Global| Jan 21 2021

Global| Jan 21 2021French Surveys Improve Despite Ongoing Virus Issues, But the French Economy Still Lags Badly

Summary

The spread of the virus in Franc is still untamed. The incidence of infection is at its highest since mid-November. The trend may still be rising. But France also has one significant positive virus-related event and that is that the [...]

The spread of the virus in Franc is still untamed. The incidence of infection is at its highest since mid-November. The trend may still be rising. But France also has one significant positive virus-related event and that is that the total number of deaths have formed a curve that is very flat and still well below its peaks of late-2020. France has taken steps to control the spread. Despite these steps, the economy has been able to improve. The French data are, in fact, a hopeful sign that as countries administer the vaccine, they might be able to use the various things they have learned about the virus to keep their economics afloat and even to repair growth. However, as much as France is a sign of hope, it is also clearly evident the French economy is only a shadow of its former self and has a long way to go. But there is progress and there is hope….

The spread of the virus in Franc is still untamed. The incidence of infection is at its highest since mid-November. The trend may still be rising. But France also has one significant positive virus-related event and that is that the total number of deaths have formed a curve that is very flat and still well below its peaks of late-2020. France has taken steps to control the spread. Despite these steps, the economy has been able to improve. The French data are, in fact, a hopeful sign that as countries administer the vaccine, they might be able to use the various things they have learned about the virus to keep their economics afloat and even to repair growth. However, as much as France is a sign of hope, it is also clearly evident the French economy is only a shadow of its former self and has a long way to go. But there is progress and there is hope….

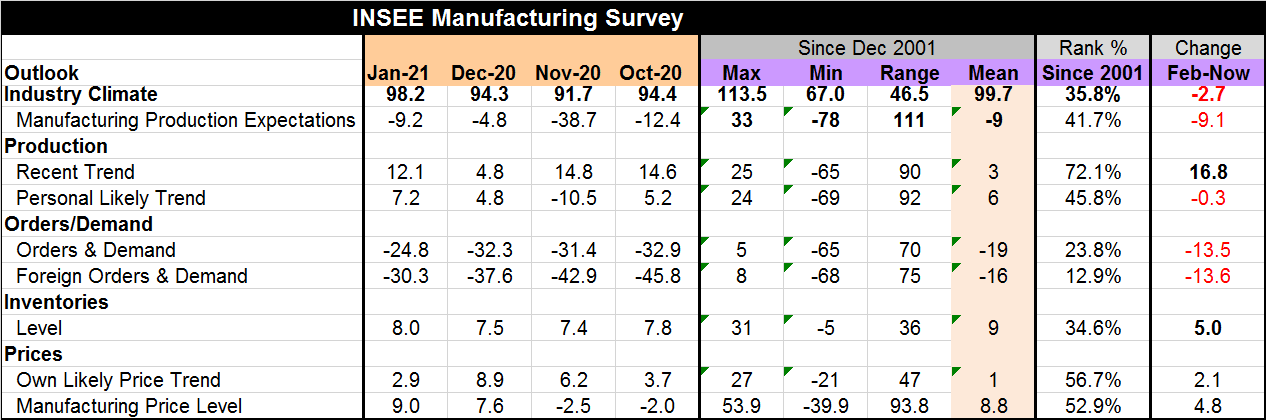

France's INSEE manufacturing survey show mixed results but with some improvement. Industrial climate improves strongly in January, rising to 98.2 from December's 94.3. However, despite that strong one-month move, that reading has only a 35.8 percentile standing- it has been stronger than this nearly two-thirds of the time. The reading also is still 2.7 points below its February pre-virus level. Still, it is progress.

The manufacturing survey shows production expectations are weaker in January, having fallen to -9.2 from -4.8 in December. It is also 9.1 points below its pre-virus level in February.

The recent production trend shows a reading of 12.1 in January, up strongly from 4.8 in December. And the personal (or own-industry) trend is at 7.2, up from 4.8 in December. The recent trend is some 16.8 points above its mark in February 2020 while the likely personal trend is lower by a thin 0.3 points. The trend has been France's friend. The recent trend reading has a quite firm 72.1 percentile standing while the own-trend has a just below-median 45.8 percentile standing.

Total and foreign orders and demand still register negative readings, but that is a congenital state for those components (total orders average -19). Total and foreign orders each improved by over seven points month-to-month in January. Still, both are lower than their respective pre-covid-19 February levels by over 13 points. And both series also are seriously weak despite the monthly gain. Total orders have a 23.8 percentile standing while foreign orders have a 12.9 percentile standing.

Inventory levels are up slightly month-to-month. They are higher by five points compared to their February level. The January reading has a 34.6 percentile standing.

Prices are mixed. The own price is lower month-to-month, falling to 2.9 in January from 8.9 in December. Overall manufacturing prices are deemed higher with a 9.0 January reading, up from 7.6 in December. Both price series, however, are up from their levels of February 2020 and both have standings slightly above their 50th percentile levels.

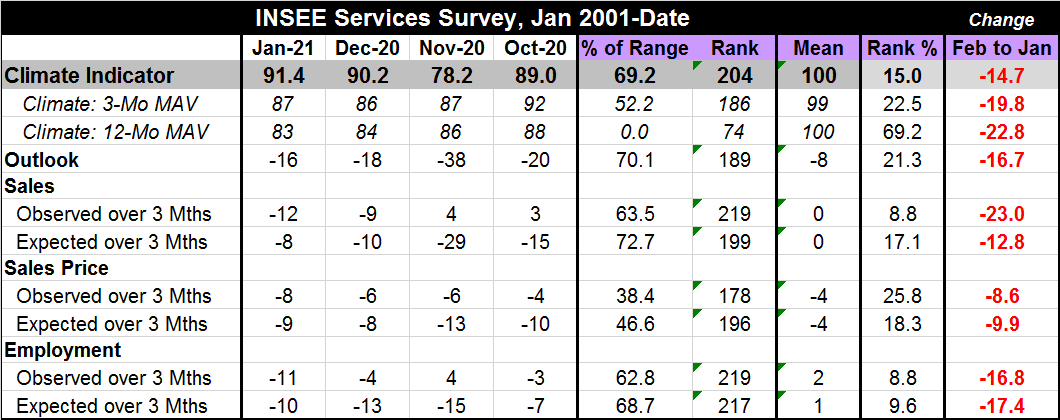

The services sector that is usually hit harder when virus problems arise also improved in January with its climate indicator rising to 91.4 from 90.2 in December. At that mark, the services indicator is in only its 15th percentile, an extremely weak reading and it is below its February level by 14.7 points. The three-month and 12-month moving averages have progressively higher rankings, underscoring that France's services sector has been slipping.

The outlook for January improved by two points compared to its December value. But the reading of -16 is still only a 21.3 percentile standing and it is below its February level by 16.7 points.

Sales as observed over three months have deteriorated, falling to a reading of -12 in January from -9 in December. That reading has an 8.8 percentile standing and is 23 points below its level of February 2020. However, that is water under the bridge. Expected sales are doing better, improving to -8 in January from -10 in December; they have a still very weak 17.1 percentile standing and are weaker than February 2020 by 12.8 points.

Sales prices both observed and expected are weak and weaker in January. The observed trend over three months is lower by two points while expected changes over three months are lower by one point. Observed prices have a 25.8 percentile standing while expected prices have an 18.3 percentile standing. Both are below their February levels by 8.6 points for observed prices and by 9.9 points for expected prices.

Observed employment has deteriorated for two months running as it fell to -11 in January from -4 in December. That reading has a very weak 8.8 percentile standing and it is 16.8 points below its February 2020 mark. However, expected employment rises to -10 in January from -13 in December. It also has a low ranking in its 9.6 percentile and is 17.4 points below its February 2020 level.

The French data show that making progress when under siege by covid-19 is possible. But the levels of activity attained in France are disappointing. The manufacturing sector is a mixed bag of progress. But services, despite their monthly gain, are still severely depressed. Maybe making progress while the vaccine is distributed will be possible, but it seems that real progress may have to wait until the virus is more decisively stuffed back into the bottle.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief