Global| Feb 24 2021

Global| Feb 24 2021French Sectors Show Minor Recovery from Pre-Covid19 Levels

Summary

French industry climate improved in February by a modest 1.4 points. It remains 3.5 points below its February 2020 (Pre-Covid19) level. After improving for two months in a row, the services index fell in February and now stands below [...]

French industry climate improved in February by a modest 1.4 points. It remains 3.5 points below its February 2020 (Pre-Covid19) level. After improving for two months in a row, the services index fell in February and now stands below its December level. Service sector climate is some 17.8 points below its pre-Covid19 level. And with this reading, the state of its recovery is uncertain. The comparison of industry or manufacturing with services underscores how much harder the services sector has been hit and that also underlines how much more it is vulnerable to these renewed bouts of infection that France has been prone to. Recovering from the virus is not a one-time thing. It is an ongoing process that depends on how well reinfections can be saved off or contained. France continues to fight this battle and it continues to take a toll on services. In terms of rankings (queue standings), the industrial sector has a 32.1 percentile standing while services have a 10.4 percentile standing. Services, broadly, have been hurt much worse. But both sectors are well below their medians; the median occurs at a rank standing value of 50%.

French industry climate improved in February by a modest 1.4 points. It remains 3.5 points below its February 2020 (Pre-Covid19) level. After improving for two months in a row, the services index fell in February and now stands below its December level. Service sector climate is some 17.8 points below its pre-Covid19 level. And with this reading, the state of its recovery is uncertain. The comparison of industry or manufacturing with services underscores how much harder the services sector has been hit and that also underlines how much more it is vulnerable to these renewed bouts of infection that France has been prone to. Recovering from the virus is not a one-time thing. It is an ongoing process that depends on how well reinfections can be saved off or contained. France continues to fight this battle and it continues to take a toll on services. In terms of rankings (queue standings), the industrial sector has a 32.1 percentile standing while services have a 10.4 percentile standing. Services, broadly, have been hurt much worse. But both sectors are well below their medians; the median occurs at a rank standing value of 50%.

Manufacturing

The manufacturing survey shows five of its eight components surveyed as improved as of February 2021 compared to February 2020. Prices are improved with the manufacturing price level stronger by 12.8 points and the own-industry likely price trend stronger by 11.8 points. The recent trend for production is improved by 9.7 points and inventory levels are higher 2.9 points. The own industrial or ‘personal likely trend’ is better by 2.7 points. While it is comforting to see that the trend metrics are improved, the more important reading for manufacturing production expectations is still weaker by 7.5 points. Orders and demand are weaker by 13.7 points with foreign orders and demand weaker by 15.4 points. On balance, it is the past trend that seems to have improved and the future that is more in doubt.

Services

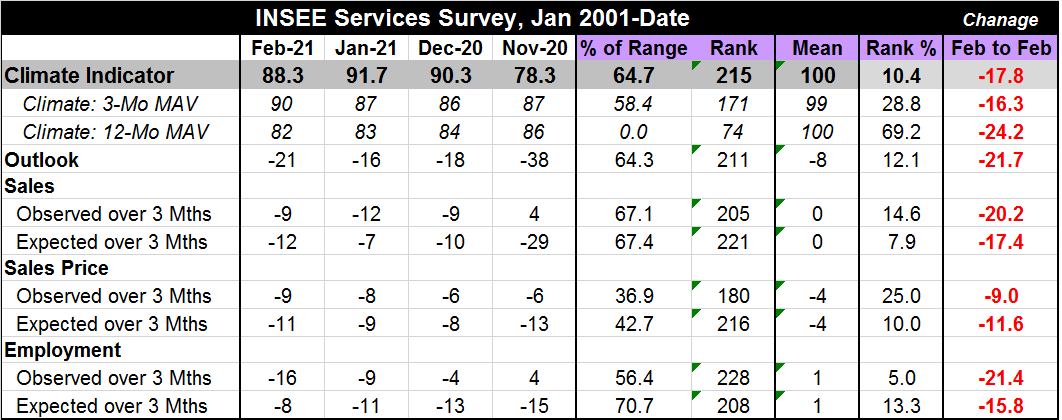

As noted previously, the service metric backtracked this month falling by 3.4 points after two months of improving. The graphic shows that the services sector has fallen a long way and is making only a minor recovery compared to its pre-Covid19 level of performance. Even smoothed measures of climate are down sharply indicating a long slide in climate values. Unlike in manufacturing, there are no readings in the services sector survey that are improved compared to February 2020.

The service sector outlook has fallen to a reading of -21 in February from -16 in January. It is its weakest Since November. The outlook is also 21.7 points lower than it was in February 2020. Sales improved in February to -9 from -12. But the sales outlook deteriorated to -12 from -7. The sales expectation is at its worst since November as well. Both measures are down sharply from their levels of February 2020. Sales prices observed and expected both are weaker month-to-month. Expected prices were last weaker in November; observed prices were weaker on a longer timeline back to May 2020. Observed employment weakened in February to -16 from -9, but expected employment improved to -8 from -11. This looks more like the to-and-fro of the virus coming on stream and then being expected to recede - a sort of virus hokey-pokey.

On balance, France is still dealing with the devil virus. It continues to nag at services and to hold back progress even creating new backtracking. For manufacturing, progress is able to be maintained better in the face of the virus. Still, the chart for neither sector looks particularly encouraging. Clearly future performance will be up to the progress made with the vaccines. The current French trends for infections and deaths caused by the virus are well off their November peaks, but they are still holding stubbornly to somewhat elevated levels.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief