Global| Feb 25 2020

Global| Feb 25 2020French Sector Climate Gauges Rise Gradually

Summary

The French business climate gauge moved up to 102.5 in February from 101.9 in January striking a 2.3 percentile standing just above its historic median. It is a reading slightly above ‘normal' and the highest mark reached since August [...]

The French business climate gauge moved up to 102.5 in February from 101.9 in January striking a 2.3 percentile standing just above its historic median. It is a reading slightly above ‘normal' and the highest mark reached since August of 2019, a half-year ago. The service sector gauge is moving up as well.

The French business climate gauge moved up to 102.5 in February from 101.9 in January striking a 2.3 percentile standing just above its historic median. It is a reading slightly above ‘normal' and the highest mark reached since August of 2019, a half-year ago. The service sector gauge is moving up as well.

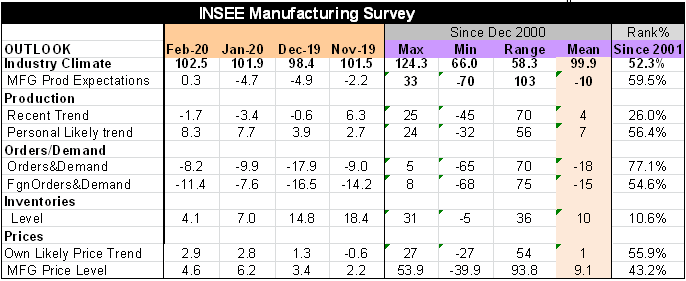

Manufacturing industrial production rose to 0.3 in February, it's first positive reading since September of last year. The February reading has a 59.5 percentile standing.

For production the recent trend has been fluctuating in value while the likely trend that firms view for their own industry has been improving steadily. The overall recent trend has only a 26 percentile standing while the own-trend has a much stronger 56 percentile standing.

Orders and demand have been slipping over the past two months but have firmed slightly on that trend. Foreign orders and demand are erratic but firmer on balance. Overall orders and demand have a 77th percentile standing while foreign orders and demand have a 54.6 percentile standing.

Inventories also have moved lower to a 10.6 percentile standing. That would seem to remove the risk of there being any inventory overhang.

The own likely price trend and the manufacturing price level each have been moving higher although the two series movements are mixed this month. The own likely price trend has a 55.9 percentile standing while manufacturing has a price level at a 43.2 percentile standing.

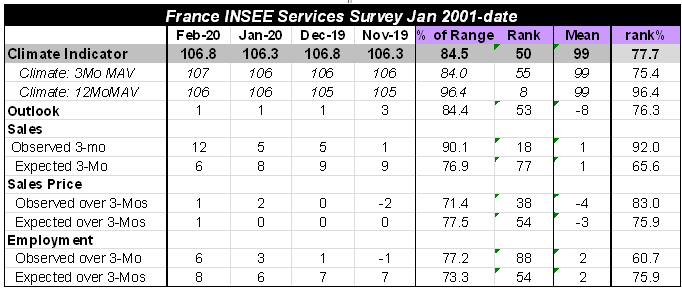

The outlook index has been very steady over the last three months; it has a 76 percentile standing.

Observed sales have been building momentum but expected sales have lost some. In terms of ranking the observed sales have a 92 percentile standing compared to the much weaker 65.6 percentile standing for expected sales.

Observed selling prices have been slightly firmer for the observed recent trend while expected sales prices have been mostly steady and flat. Observed selling prices are at an 83rd percentile standing compared to an expected sales standing in its 75.9 percentile.

The Employment situation has seen some strengthening for the observed and expected paths recently. For this metric the expected series is stronger with a 75.9 percentile standing compared to a 60.7 percentile standing for the observed trend.

The services and industrial surveys show a French economy that is operating above its normal or median marks on its key service sector metrics and operating at or above its median marks for most of, but not all, its manufacturing sector metrics. For the most part the survey seems to depict a well-functioning unexciting economy that is neither in danger of slipping into a weaker phase nor on the verge of acceleration.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief