Global| Aug 14 2007

Global| Aug 14 2007French Long-term HICP Trend Moves Lower

Summary

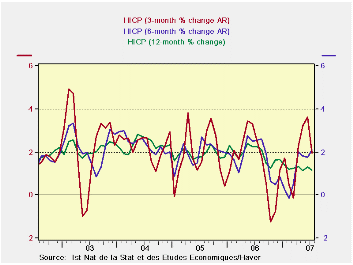

3-month inflation shifts much lower. French inflation trends show Frances contribution to the Euro areas inflation trends are middle of the road. France is still not in great shape but it is not one of the problem countries on the [...]

3-month inflation shifts much lower.

French inflation trends show France’s contribution to the Euro area’s inflation trends are middle of the road. France is still not in great shape but it is not one of the problem countries on the inflation side. And France has seen its GDP slow unexpectedly in the second quarter. The French stock market remains one of the very weakest in Europe. We are for the first time getting some consistent signs of slowing from Europe. It’s too soon to say if they will last or not.

The trouble for the ECB is going to be sorting out the disparate trends. It will have to deal with its previous hint that it was set to hike rates and compare it to actual current needs. Financial markets events work to put the ECB on hold. And then there is the GDP picture which was not as strong in Q2 as had been expected across the Euro area. The moderation of inflation trends feeds a third development into this mix that also comes out on the side of pushing the ECB to stay its hand.

This by the way is not a isolated position for the ECB. Japan’s central bank is in a similar fix for all the same reasons.

| M/M % | SAAR % | Year/Year | |||||

| Jul-07 | Jun-07 | May-07 | 3-Mo | 6-Mo | 12-Mo | Yr Ago | |

| HICP Total | 0.0% | 0.2% | 0.2% | 2.0% | 2.1% | 1.2% | 2.2% |

| Core | #N/A | 0.1% | 0.1% | #N/A | #N/A | #N/A | 1.5% |

| CPI: All Items | 0.1% | 0.2% | 0.2% | 1.7% | 1.8% | 1.1% | 2.0% |

| CPI ex Food & Energy | 0.1% | 0.1% | 0.1% | 1.1% | 1.2% | 1.3% | 1.4% |

| Food | -0.2% | 0.5% | 0.1% | 1.9% | 0.4% | 0.8% | 2.1% |

| Alcohol | 0.3% | 0.4% | 0.4% | 4.5% | 3.4% | 0.6% | 0.2% |

| Clothing & Shoes | -0.7% | 0.2% | 0.2% | -1.4% | 1.2% | 0.2% | 0.2% |

| Rent & Utilities | 0.2% | 0.5% | 0.0% | 2.7% | 3.4% | 2.4% | 4.8% |

| Health Care | 0.4% | 0.0% | -0.1% | 1.1% | 0.3% | 0.4% | -0.2% |

| Transport | 0.2% | 0.4% | 0.7% | 5.0% | 6.1% | 1.5% | 4.0% |

| Communication | 0.0% | -0.1% | 0.1% | -0.1% | -3.8% | -0.6% | -6.2% |

| Recreation & Culture | -0.2% | 0.1% | -0.3% | -2.0% | -0.9% | -1.6% | -0.9% |

| Education | 0.2% | 0.2% | 0.2% | 2.9% | 2.7% | 2.4% | 2.8% |

| Restaurant & Hotel | 0.5% | 0.3% | 0.2% | 4.4% | 3.7% | 2.9% | 2.3% |

| Other | 0.0% | 0.1% | 0.3% | 1.7% | 1.8% | 2.0% | 3.2% |

| 6-mo | 12-mo | Yr-Ago | |||||

| Diffusion | 54.5% | 63.6% | 45.5% | ||||

| 3COLSPAN | |||||||

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief