Global| Jan 10 2019

Global| Jan 10 2019French IP Weakens as PMI Dips Below Neutral

Summary

The thrill is gone in France. In 2017, French manufacturing did exceptionally well, but it lost steam gradually in 2018 and at end-2018 the momentum is gone and output in manufacturing is falling for the third consecutive month. The [...]

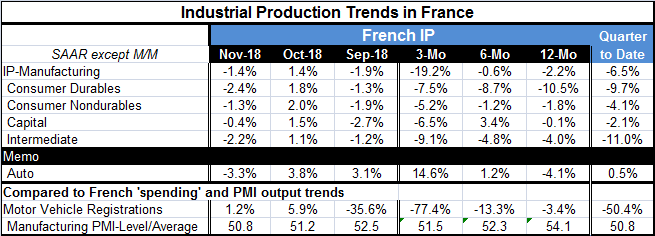

The thrill is gone in France. In 2017, French manufacturing did exceptionally well, but it lost steam gradually in 2018 and at end-2018 the momentum is gone and output in manufacturing is falling for the third consecutive month. The December manufacturing PMI value has dipped below 50, signaling the contraction that has been apparent for several months.

The thrill is gone in France. In 2017, French manufacturing did exceptionally well, but it lost steam gradually in 2018 and at end-2018 the momentum is gone and output in manufacturing is falling for the third consecutive month. The December manufacturing PMI value has dipped below 50, signaling the contraction that has been apparent for several months.

Ubiquitous declines

For the headline manufacturing series for consumer durables and nondurables, for capital goods, and for intermediate goods and their growth rates for IP over three months, six month and 12 months declines are produced with only one small exception. Of these fifteen growth rates, only capital goods over six months show any hint of growth or stability.

In the quarter-to-date (November plus October output divided by the Q3 average), all sectors show a declines.

The bad news could be worse...

The only calming note here is that while in all cases but one (consumer durables), the annualized output decline over three months is greater than over 12 months; there is less weakness over six months than over 12 months. That means there is no progressive deterioration in place.

Little good news

Still, there are few places to look for good news. Monthly data show declines in all sectors in both September and in November with a series of increases sandwiched in between. These are the three months whose results make the three-month growth rate so weak. There is so much weakness in November and in September that the rise of output in October is completely drowned out.

Auto output is nonetheless strong

Interestingly and contrarily, auto output is doing much better than all that. Auto output is actually accelerating from 12-month to six-months to three-months. It has two increases in the past three months, but that one decline came in November. On a quarter-to-date basis, auto output is up at a 0.5% annual rate.

Vehicle registrations are weak

The news on auto output is wholly contrary to auto registrations patterns as registrations are decelerating from 12-months to six-months to three-months and are collapsing over three months at a -77.4% annual rate; a result largely owing to a horrible September. .

French manufacturing PMI

Through all of this, France’s manufacturing PMI is eroding sequentially (as the chart shows) sketching a smoother path of erosion than is manufacturing output. The PMI is also is losing standing sequentially over recent months.

Other issues

The weakness in French manufacturing is clearly ongoing and fits right into the patterns we see in Germany, in the EU and with the survey for France that was just released by INSEE. In addition to the all the economic erosion, there is other trouble afoot in Europe. Hungary is being obstreperous and says it will never give in to German demands on migration. Italy is hoping to join with Hungary in upcoming meetings to provide a sort of Euro-skeptic block within the EU. France, of course, has been struggling with the yellow vest protests. In Germany, several airports have been closed as airport workers have struck for higher wages. And in the UK, the Brexit vote deadline approaches.

Migrant Issues

As economic growth slows, these tensions will probably become more problematic rather than less. Tensions in Europe that had been under the surface have been brought to the fore by the migration problems. The numbers of indigent people in the world has growth for various reasons and they are creating problems globally, not just for the EU. In the EU, there is a question about the Union’s right to make determinations that will bind its members. The EU has gradually been increasing its reach. It has finally gone on to a point where many members have become resentful of its intrusion. The U.K. felt so strongly on the issue that it left. What comes next we can’t tell, but since Italy has tried to shut itself off from recovering any more migrants, the influx has spread to France and Spain. Italy’s along with Greece has been forced to absorb the bulk of the migrants. Italy’s new intransigence on the matter has forced a new solution. Malta had been forced to absorb one boatload of migrants. Now in a new deal, migrants are going to be more evenly spread as Germany, France, Portugal, Ireland, Romania, Luxembourg, and Netherlands are going to take in migrants who had been stranded on rescue ships at sea and had been held on Maltese military vessels. The number of migrants reaching Spain has surged as Italy’s crackdowns on private rescue vessels saw the number of boats and migrants heading across the central Mediterranean toward Italian shores dropping sharply as Italy refused to let them land and unload. In Spain, police recently broke up a gang that smuggled people and drugs by boat from Morocco into Spain, charging migrants up to 2,000 euros a trip. The migrant saga is a story and an issue that is not going to go away. Tensions in the EU are liable to continue to mount over this issue alone.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief