Global| Dec 09 2016

Global| Dec 09 2016French IP Provides a Bridge to a Preview of ECB Policymaking in 2017

Summary

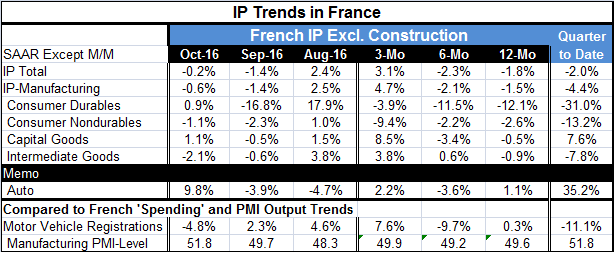

French manufacturing and overall industrial output fell in October. The French PMI reading has output advancing in October. The chart shows that over broad periods the IP and PMI indices for France move roughly in the same direction [...]

French manufacturing and overall industrial output fell in October. The French PMI reading has output advancing in October. The chart shows that over broad periods the IP and PMI indices for France move roughly in the same direction (yes, I plot IP as an index, not as a growth rate on this chart). But over short periods, there can be disconnects between the signals of these two reports. This month we have one.

French manufacturing and overall industrial output fell in October. The French PMI reading has output advancing in October. The chart shows that over broad periods the IP and PMI indices for France move roughly in the same direction (yes, I plot IP as an index, not as a growth rate on this chart). But over short periods, there can be disconnects between the signals of these two reports. This month we have one.

PMI and industrial production: usually two peas in a pod

The PMI is formally a survey of the breadth of output and other sector conditions rather than an actual reading on the level of output itself. The IP reading for manufacturing is strictly about the level of output. Both the PMI gauge and the IP gauge decelerated from 2011 to late-2012 then picked up, accelerating through late-2015. In early-2016, both indices fell, but now the story is less clear and less consistently told. Manufacturing IP has spiked and dropped while the manufacturing PMI gauge has rising sharply and advanced further. These two tentative IP stories are on a different page for the moment. And it is important to know which is right.

The ECB's unexpected move

While markets are abuzz over ECB policy, they are largely dismissive of the ECB's latest move to taper policy since ECB head Mario Draghi refuses to call it a taper. But there are events afoot whose signals should not be ignored and in whose context make this decision look more like an actual taper.

The PMI view of the world

The PMI view of the world has been that the euro area and France have been improving after a long period of lethargy and contraction in manufacturing (see the period averaged manufacturing PMI values in the table). Yet, for IP, contraction is still being experienced in September and in October as well as over six months and 12 months. However, over three months, French output is expanding mostly on the back of a surge in output posted in August. Still, in the fourth-quarter-to-date, French manufacturing output is on the decline again according to the output gauge. The IP view of the world is very different from the PMI view.

To taper or not to taper- is that real question?

These distinctions are important since France is the second largest economy in the euro area. Its performance will importantly affect macroeconomic measures of the euro area itself. And although Mario Draghi is not calling the ECB action a taper, the ECB is set to reduce its monthly bond purchase amount but to expand the period for making purchases to ultimately inflate its balance sheet by more (not less) in the wake of yesterday's announcement. Still, the bond market acted as though it would be getting less support. The intensity of the monthly purchases is an important aspect of the bond market's support by the ECB and that is now being reduced. So this is why the notion of taper is sort of being obscured because the ECB is doing less (per month) but also doing more (in total). It's a rare opportunity to talk out of both sides of its mouth at once.

The monetary policy plot thickens

Also yesterday Jens Weidmann, head of the German Central Bank, declared that the ECB must make policy solely based on the rate of inflation. This sounds like Weidmann is throwing down the gauntlet and it is curiously-timed to coincide with the ECB's 'non-taper' and the Bundesbank's own new forecast of elevated growth for Germany in 2016 and 2017. At the same time, the Bank of France has issued a new forecast and does not see things picking up for France until 2018. We all know where the Bundesbank stands on policy and the only 'problem' with Weidmann reminding the ECB of its mandate was the way he and other Germans ignored it and obstructed and delayed the ECB's attempts at stimulus to boost the inflation rate over the past several years when inflation fell and ran markedly below its policy objective for a protracted period. While Draghi assures us that 'everyone is on the same page' in some sense, it appears that agreeable state of affairs is about to break down. The worst situation for the euro area and the ECB would be to have inflation rising and over target with the German economy running hot, the French economy running cold and the Italian political situation hanging in the balance. Yet, with OPEC paring output -and the Saudis just today put customers on notice for supply cutbacks - pressure on headline inflation just might emerge a bit faster than had been expected.

The minefield of shared monetary policy by the ECB

The ECB does not engage in 'price level targeting.' That means that a period of inflation overshooting is not typically followed by undershooting or vice versa. So Weidmann wants to make it clear that just because the HICP undershot its target for 47 months in a row does not mean that any overshooting will be tolerated on a short-term basis. Weidmann is a good trough uncompromising central banker. And because of those traits, he is a really bad politician and that skill might serve him better here. January 2013 was the last time the ECB essentially hit its inflation target of 2% (the actual target is just under 2%). It has been the better part of four years during which the ECB has not even been even close to achieving it. The current price level in the EMU (as of November 2016) is six percentage points below where it would have been had the ECB achieved a steady state of 2% growth in the HICP from January 2013. You might imagine how with all the austerity and pain suffered by other countries in EMU it will go down if at the first whiff of 2.1% inflation Weidmann wants to bring interest rates higher. While the ECB has no mandate other than achieving its inflation objective (of a bit less than 2%) and while there is no provision for price level targeting, the ECB would seem to have scope to not be on a hair-trigger with policy rates- especially with oil prices as the trigger. Yet, Weidmann clearly does not see it that way. And while is no scope under the ECB charter to talk about anything other than inflation with the German economy doing so well, it will be politically very divisive to be hiking rates in the euro area where inflation is rising modestly because of global oil prices when conditions among members countries are still exhibiting so much slack- except for Germany, of course- especially after four years of such rampant undershooting.

The rocky road ahead (not ice cream)

It seems to me that this is the reality for which we are headed. That is why the ECB does not want to call this a taper now, but it surely looks like one. And it looks like the time for policymakers to sit around the ECB board table and reach full agreement on what to do is also coming to an end. We can already see previews of how this policy plays out by what is going on at the Fed in the United States. In Europe, the discord will be much greater and much more heated. Welcome to the world of policymaking in 2017. Fasten your seat belts, please. There will be turbulence ahead.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief