Global| Mar 15 2016

Global| Mar 15 2016French Inflation Crosses Over to an Expanding Dark Side: Deflation

Summary

French inflation has turned to the dark side, showing persisting deflation and going deeper down the rabbit hole of deflation. Prices are now falling for two months in a row, as even the domestic measure, the CPI ex-energy, is [...]

French inflation has turned to the dark side, showing persisting deflation and going deeper down the rabbit hole of deflation. Prices are now falling for two months in a row, as even the domestic measure, the CPI ex-energy, is negative for two consecutive months and fading in terms of its sequential progression.

French inflation has turned to the dark side, showing persisting deflation and going deeper down the rabbit hole of deflation. Prices are now falling for two months in a row, as even the domestic measure, the CPI ex-energy, is negative for two consecutive months and fading in terms of its sequential progression.

The chart shows that the ex-energy price index is no longer showing ongoing `price level recovery.' That has stalled and prices have tuned back lower.

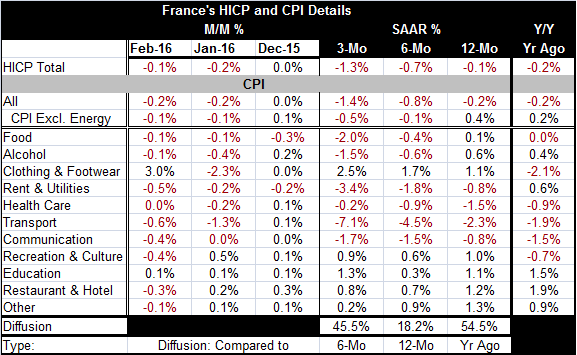

French trends

One year ago France's HICP was negative. Now it is again falling over 12 months, over six months as well as over three months. It is falling progressively faster over shorter horizons. The domestic CPI mimics these movements.

The ABCs of oil-producer Iran's noncooperation

With global oil prices having regained their sanity after trying to buck the trend dictated by the glut in energy, prices are weakening again. Iran is reiterating its long held and very consistent position that it will join no output restriction deal. This is important to understand. Since others have said unless Iran is `in' they are out. Iran is committed to hiking its own production. It has, in fact, been steadily expanding its output. Having been under sanctions, Iran's position is that it has been deprived of sales because of these past sanctions that have just been lifted. It is not about to be trapped into some low-output regime for the sake of firmer oil prices that will benefit others more than it will benefit Iran. Keep in mind that Iran's cooperation in any output-reduction scheme is simply very highly unlikely. And that makes any broad-based output reduction scheme highly unlikely.

No uptrend for oil

The oil price dynamics are still negative. While the impulse to domestic prices no longer is as clear-cut and consistent as it once was, with the recent price up, oil prices are weakening again and there is no upward pressure in train. The glut remains in full force.

Oil is simply one of many negative price impacts

Of course, weak oil prices are behind a lot of the global price weakness, but oil is not the only weak commodity price. Weak demand is adding to downward price pressure apart from those forces transferred through costs up through the supply chain. There are negative effects blowing back from weak aggregate demand as well as those welling up from lower costs through the supply chain. They are squeezing prices lower from both sides.

Deflation is broad based in France

France is showing weak trends with inflation lower over six months than over 12 months. The diffusion metric of only 18.2% on CPI component price changes on that comparison is very low. Only 18% of the sectors have inflation rising on that horizon's comparison. And comparing three-month to six-month trends, diffusion is still under 50% with a reading of 45.5%. Inflation is falling on these horizons in more categories than it is rising. Deflation is broad-based. And the pace of the fall is accelerating.

Price weakness remains widespread as conventional policy limits are reached

So far there is no evidence in France that ECB policies are helping to stabilize prices. Earlier we saw pronounced ongoing price weakness in Germany as well. Italy shows the same weak-price characteristics. The ECB has launched its most aggressive policy on the negative interest rate and QE/loan front. Still, it has limitations on what it can do. As we know from U.S. experience, when monetary accommodation reaches its conventional limits, other efforts may not bear fruit or may bring a stunted harvest.

Poor environment/uncharted policy waters

Europe is still slow-growing. European banks are not as well cared for as banks in the U.S. Those conditions may hamper the effectiveness of the ECB's efforts which themselves are probably less effective because they were implemented so late in the cycle. Europe has a wide array of negative interest rates to deal with. The ECB is making policy in uncharted waters with untested effects and some of the things policy is doing have some clear negative side effects that have not been explored before. It is not even clear that the side effects will not dominate the main intent of policy. Japan is one place where there seems to be serious rethinking of the negative-rate phenomenon as there has been a sharp behavioral shift by Japanese consumers. It is no longer clear how much the BOJ stands behind its own negative rate effort.

Deflation is a growing problem and not just in France

Among 11 of the early reporting EMU members, six show a declining price level year-over-year already. One shows that the year-to-year price level comparison is unchanged. Monthly comparisons amplify this nascent trend. Of these 11 members, 10 show month-to-month level declines in February. Eight of these countries show monthly declines in January as well. By comparison in December price levels were falling in only three countries with flat prices month-to-month in two others.

It's spreading...

Price deflation is spreading. France, Italy and Germany, the three largest EMU members each show the same negative dynamic. With oil prices turning weaker again on global markets, there is NO SIGN of price level stability in the euro area. Of course the new economic policies of the ECB are nascent, and some of the policy changes are on the books and scheduled for implementation, but still not in force. But as of now the battle is being lost. There is still a lot of work to do to put the deflation toothpaste back in the tube.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief