Global| May 09 2008

Global| May 09 2008France: With Consumer and Intermediate Goods Output Weakening… Can Capital Goods Be Far Behind?

Summary

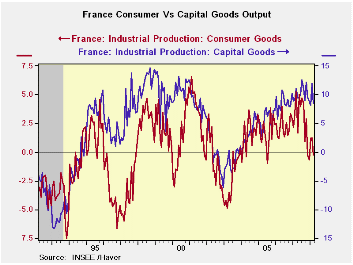

France remains a quintessential e-Zone economy. Its consumer sector has gone slack but capital goods output is still churning up a storm. Still capital goods is lagging sector. Its output can tend to stay strong as its industries turn [...]

France remains a quintessential e-Zone economy. Its consumer

sector has gone slack but capital goods output is still churning up a

storm. Still capital goods is lagging sector. Its output can tend to

stay strong as its industries turn out goods that are legacy of strong

demand earlier in the cycle; it can lag in recovery as well, as demand

for new equipments waits on the moment that new capital constraints are

encountered. Capital goods is lagging sector in the economy. For this

reason I do not take its ‘enduring strength’ as sign that it will

bootstrap the rest of the economy into expansion.

The chart above shows the longer term relationship between

consumer goods and capital goods output trends in France. History also

tells us that the weakness in the consumer sector is something to be

wary of – the sector tends to be a harbinger.

The banking sector problems in Europe and in France, the

strong euro exchange rate, the slippage in various domestic surveys,

give us even more reason to be wary of what has been ongoing strength

in the capital goods sector. It seems to have become a sector with

increasingly poor fundamentals despite its resilience.

| French IP Excluding construction | |||||||

|---|---|---|---|---|---|---|---|

| Saar except m/m | Mar-08 | Feb-08 | Jan-08 | 3-mo | 6-mo | 12-mo | Quarter-to-date |

| IP total | -0.8% | 0.5% | 0.4% | 0.0% | 2.1% | 1.0% | 1.4% |

| Consumer | -0.8% | 0.2% | 1.7% | 4.4% | -2.3% | -1.6% | 2.1% |

| Capital | -1.1% | 2.0% | 0.0% | 3.7% | 5.2% | 4.9% | 4.7% |

| Intermed | -1.7% | 0.4% | 1.2% | -0.4% | 0.4% | -1.1% | 2.0% |

| Memo | |||||||

| Auto | -2.9% | -2.1% | 1.1% | -14.6% | 2.8% | -1.0% | -1.0% |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief