Global| Aug 21 2009

Global| Aug 21 2009Flash PMI’s Turn in EMU

Summary

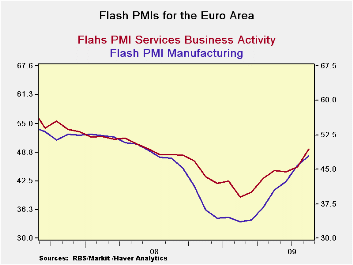

PMI Signals Are Lagging - PMI’s have lagged the pickup but they are near to neutral and the Markit overview index has reached the neutral mark of 50 in August. Markit’s overall PMI reading for the Euro Area rose to this neutral level [...]

PMI Signals Are Lagging - PMI’s have lagged

the pickup but they are near to neutral and the Markit overview index

has reached the neutral mark of 50 in August. Markit’s overall PMI

reading for the Euro Area rose to this neutral level of 50 in August

lagging behind the GDP signals that in Q2 already turned up for two key

E-Zone countries (Germany and France) and with the Zone’s own GDP

barely falling. Purchaser indices that usually are more sensitive than

other macro-data have not been leading in Europe and that is a point to

ponder.

Large jumps in August play catch-up --

The jumps in the respective MFG and Services indices were large. For

Services it is the largest jump in its history that extends back to

mid-1998. For the MFG index it is the eighth strongest jump in a

history that goes back to mid-1997.

Still, the fact that the big signal from the PMIs is lagging

is a curiosity.

Thinking more about PMIs -- PMI indices are

diffusion indices and formally they are indices of the breadth of

change in a certain direction (up or down, greater or less) rather than

of strength. The overall index is a weighted average of components that

look at specific aspects of an industry getting diffusion responses on

each. However, these indices are used as a proxy for strength since the

correlation with ‘strength’ is high for ‘breadth’. Still we should bear

in mind always that ‘strength’ is not in fact ‘breadth’, they are

different things and sometimes the difference matters, even if most of

the time it does not.

Viva la difference?? If you have never

thought of the PMIs this way before, note that this concept has been

long in play in analyzing trends in the stock market. The stock market

index is a weighted average of stocks, an index that goes up and down,

but technicians also look at indicators of ‘breadth’. And when they do,

they DO NOT call them ‘strength’ but when breadth and strength go

together a rally’s strength is said to be more powerful. Sometimes the

market goes ‘up’ but decliners ‘outpace’ advancers. This is exactly the

same thing as looking at output Vs its diffusion. Output and diffusion

do not always go in the same direction. Manufacturing output is like

the stock index and the MFG PMI is its breath measure. Services output

is compared to the breadth of the services PMI. But in the case of our

economic statistics we get the breadth reports much more quickly than

we get the output reports and so the diffusion indices take on a life

of their own and become proxies for ‘output.’

The diffusion difference - What the

diffusion indices usually do, is to pick up small improvements that

might be scattered around the economy and lost. Diffusion indices

create a signal that would otherwise get lost in the aggregation of

data with weighting always going to the largest of reporters. So this

time around it seems that the opposite is happening. A few larger

reporting firms are doing better and driving the macro -data higher

while the smaller firms are not yet on board for the ride. This is not

surprising with all the government intervention (…in Europe, the UK and

the US, in fact) since government tends to work ‘best’ with big

business. If the assistance works properly (or at all) stimulating

output at the larger firms (like auto makers) should create some

knock-on effects that will draw other firms into the upswing. And the

PMI reports may be signaling that, in August, this is finally

happening. But this process is a bit like trying to start a fire with

wet wood on windy day. Just because you have gotten a spark does not

means you will be able to nurse a bone-warming bonfire out of it.

Still, with a spark, you have a chance. And there is some tentative

evidence that growth is spreading- at last. Getting the diffusion

indices on board is crucial – they remain important barometers of the

success in spreading growth.

| FLASH Readings | ||

|---|---|---|

| Markit PMIs for the E-Zone | ||

| MFG | Services | |

| Aug-09 | 47.87 | 49.53 |

| Jul-09 | 46.25 | 45.69 |

| Jun-09 | 42.62 | 44.65 |

| May-09 | 40.68 | 44.82 |

| Averages | ||

| 3-Mo | 43.18 | 46.53 |

| 6-Mo | 38.98 | 44.58 |

| 12-Mo | 39.28 | 44.11 |

| 127-Mo Range | ||

| High | 60.47 | 62.36 |

| Low | 33.55 | 39.24 |

| % Range | 53.2% | 44.5% |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief