Global| Mar 23 2009

Global| Mar 23 2009February U.S. Existing Home Sales Recover January Decline as Prices Remain Weak

by:Tom Moeller

|in:Economy in Brief

Summary

Sales may indeed respond to prices. That seemed the case according to the National Association of Realtors report on sales of existing homes. They rose 5.1% during February 4.72M and the increase reversed January's decline. Consensus [...]

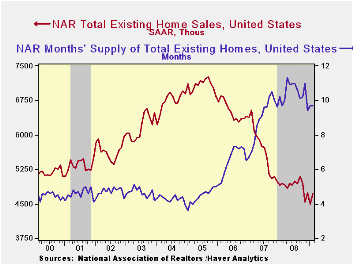

Sales may indeed respond to prices. That seemed the case according to the National Association of Realtors report on sales of existing homes. They rose 5.1% during February 4.72M and the increase reversed January's decline. Consensus expectations had been for February sales of 4.45M homes. Total sales include sales of condos and co-ops. In each of the country's regions sales during February roughly recovered their January declines.

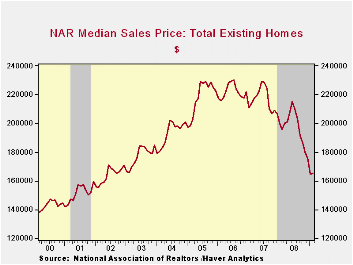

Did continued weakness in pricing power spur the February recovery? Median home prices did rise 0.4% from January. The uptick followed, however, a revised 6.2% (NSA) January decline which was double the initial estimate. The recent weakness in prices left them 15.5% below February of last year and prices have fallen 28.2% since their peak. Declines in home prices and lower interest rates have gone a long way to increase the affordability of an existing home which is up roughly one quarter from one year ago. The measure rose to a record high for the series which dates back to 1971.

For existing single-family homes alone sales recovered most of their January decline with a 4.4% rise to 4.230M units. However, that remained near the lowest level since July 1997. Is the earlier decline in sales forming a bottom? They have been essentially flat for the last four months. (These data have a longer history than the total series).

The number of unsold homes (condos & single-family) on the market increased a slight 5.2% during February but the year-to-year decline of 5.5% may eventually give some lift to home prices. At the current sales rate there was a 9.7 months' supply on the market which was near the lowest since 2007. For single-family homes the inventory also rose a modest 2.6% (-6.7% y/y) after little change during January. At the current sales rate there was a 9.1 month's supply, near the lowest since 2007.

The data on existing home sales, prices and affordability can be found in Haver's USECON database. The regional price, affordability and inventory data is available in the REALTOR database.

The "fact sheet" for the Public-Private Investment Program from the U.S. Treasury Department is available here.

House Prices and Bank Loan Performance from the Federal Reserve Bank of San Francisco can be found here.

| Existing Home Sales (Thous) | February | January | February y/y % | February '08 | 2008 | 2007 | 2006 |

|---|---|---|---|---|---|---|---|

| Total | 4,720 | 4,490 | -4.6 | 4,950 | 4,893 | 5,674 | 6,516 |

| Northeast | 740 | 640 | -14.9 | 870 | 845 | 1,010 | 1,093 |

| Midwest | 1,040 | 1,030 | -14.0 | 1,210 | 1,130 | 1,331 | 1,494 |

| South | 1,740 | 1,640 | -11.2 | 1,960 | 1,860 | 2,243 | 2,577 |

| West | 1,200 | 1,170 | 30.4 | 920 | 1,064 | 1,095 | 1,357 |

| Single-Family | 4,230 | 4,050 | -3.6 | 4,390 | 4,341 | 4,960 | 5,712 |

| Median Price, Total, $ | 165,400 | 164,800 | -15.5 | 195,800 | 197,250 | 216,633 | 222,042++ |

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief