Global| Jan 24 2008

Global| Jan 24 2008Existing Home Sales Lowest Since 1998, Prices Off 10% Since Peak

by:Tom Moeller

|in:Economy in Brief

Summary

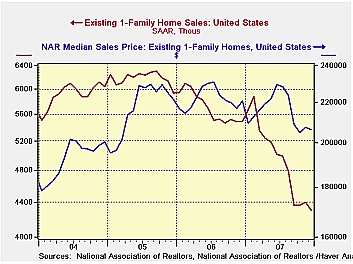

According to the National Association of Realtors, sales of existing single family homes slipped 2.0% during December after a very slight 0.7% uptick in November. The decline was to the lowest level since 1998 and since the sales peak [...]

According to the National Association of Realtors, sales of

existing single family homes slipped 2.0% during December after a very

slight 0.7% uptick in November. The decline was to the lowest level

since 1998 and since the sales peak in late 2005, sales were down by

roughly one third. For the full year sales fell 13.0% on top of a 7.7%

decline in 2005.

Sales including condominiums fell 2.2% last month and ended the year down 22.0% from last December, down 12.8% for the full year.

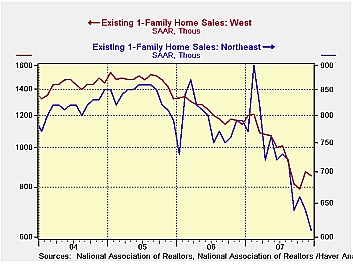

By region, home sales in the Northeast fell 4.6% (-22.4% y/y)

and for the full year were off 7.5% after the 6.9% 2006 drop. In the

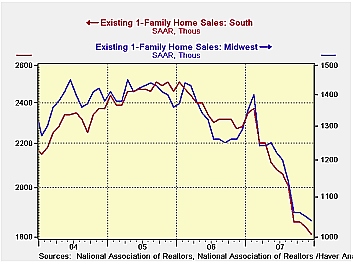

Midwest December sales fell 1.7%, 10.6% for the full year, while sales

in the South ended the year with a 1.0% drop. Combined with a 2.0% fall

in November overall sales in the South last year fell 13.0%. The worst

of it came out West. The 2.1% December decline pulled sales for the

year down 19.2% after a 16.2% drop during 2006. For the full year,

sales of single family homes in the West was the lowest since 1998.

The median price of an existing single family home fell 0.4% (-6.5% y/y) in December. It was the fifth m/m decline in the last six months. It lowered prices for the full year 2.8% below the 2006 level, the first full year decline in the thirty five year history of the series. Since the peak early last year, home prices were off 9.9% in December.

Perspectives on Housing and the Economic Outlook from the Federal Reserve Bank of Kansas City can be found here.

The latest Budget Outlook from the Congressional Budget Office is available here.

| Existing

Single Family Home Sales |

December | y/y % | November | December '06 | 2007 | 2006 | 2005 |

|---|---|---|---|---|---|---|---|

| Total | 4,890 | -22.0 | 5,000 | 6,270 | 5,679 | 6,510 | 7,075 |

| Northeast | 830 | -22.4 | 870 | 1,070 | 1,007 | 1,088 | 1,169 |

| Midwest | 1,160 | -20.5 | 1,180 | 1,160 | 1,334 | 1,492 | 1,588 |

| South | 1,970 | -20.9 | 1,990 | 2,490 | 2,243 | 2,578 | 2,704 |

| West | 940 | -24.8 | 960 | 1,250 | 1,094 | 1,353 | 1,616 |

| Single-Family | 4,310 | -21.6 | 4,400 | 5,500 | 4,966 | 5,708 | 6,182 |

| Median Price, Total, $ | 206,500 | -6.5 | 207,300 | 220,800 | 215,642 | 221,883 | 217,492 |

by Tom Moeller January 24, 2008

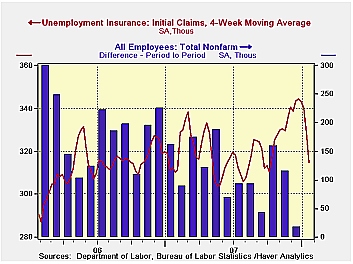

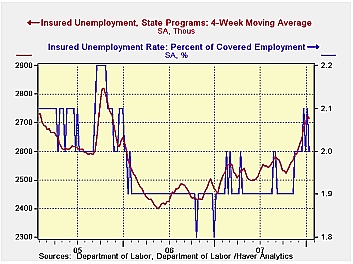

Initial claims for jobless insurance remained unexpectedly low last week. A 1,000 w/w decline followed sharp declines during the prior three weeks which now have totaled 15.7% since the high one month ago. The latest level was the lowest since September.

Initially, this drop in claims was doubted as genuine due to the difficulties of seasonal adjustment during the Holiday season. Those difficulties suggested that claims would bounce up last week. Indeed, a rise to 320,000 had been the Consensus expectation. No special factors were sighted by the Labor Department as having influenced last week's figure.

The four week moving average of initial claims, a measure

which smoothes out most of the series' w/w volatility, fell sharply to

314,750 (+0.7% y/y). It was the lowest level since mid-October and may

suggest that recent labor market weakening was not as great as earlier

perceived. But in a wishy-washy spirit, the perception

should not be wholly dismissed based on the new figures.

A claims level below 400,000 typically has been associated with growth in nonfarm payrolls. During the last six years there has been a (negative) 78% correlation between the level of initial claims and the m/m change in nonfarm payroll employment.

Continuing claims for unemployment insurance dropped 75,000. It reversed a 59,000 increase during the prior week which was revised down slightly. The figure provides some indication of workers' ability to find employment but here again difficulties of seasonal adjustment this time of year are great.

The continuing claims numbers lag the initial claims figures by one week.

The insured rate of unemployment fell back to 2.0% from 2.1% during the prior week.

Monetary Policy Implementation Frameworks: A Comparative Analysis from the Federal Reserve Bank of New York is available here.

| Unemployment Insurance (000s) | 01/19/08 | 01/12/07 | Y/Y | 2006 | 2005 | 2004 |

|---|---|---|---|---|---|---|

| Initial Claims | 301 | 322 | 4.9% | 313 | 331 | 343 |

| Continuing Claims | -- | 2,751 | 11.3% | 2,459 | 2,662 | 2,924 |

by Robert Brusca January 24, 2008

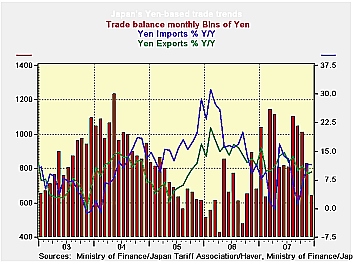

Japan’s exports show a withering trend as Japan’s imports continue to rise at a brisk pace. Export and import price indexes, however, show that export volumes are being maintained better than the nominal figures tell us as export prices are falling and falling faster than nominal exports are shrinking. Imports on the other hand are not as strong as nominal figures show since prices are rising sharply. While imports are up by 37% in the past three months from August to November, import prices rose by less at 35.8% for October through December. As a result Japan’s nominal trade figures give exactly the opposite impression of what is going on.

Nominal imports are rising, while real imports are actually

slowing. On the export side nominal exports are falling, but export

volumes are in fact still expanding. Rising oil prices are creating a

misdirection in terms of import trends. For exports, the rise in the

yen accounts for the drop in export prices. The yen’s rise tends to

result in a reduction of yen export prices, as though exports are

denominated in foreign currency. Volume still seems to be rising, but

if this is a currency effect it could be a warning that profits for

exports are in for a set back.

| Japan Trade Trends | |||||||

|---|---|---|---|---|---|---|---|

| in period level of % chg | Average in period/or % change | ||||||

| All data yen basis | Dec-07 | Nov-07 | Oct-07 | 3Mo Prev | 6Mo Prev | 12Mos Prev | 12 mo Ago |

| Balance on Goods | -- | 11,959 | 13,141 | 11,929 | 11,196 | 10,628 | 7,838 |

| % m/m | % saar | ||||||

| Exports Goods % | 0.9% | 0.6% | 1.9% | 1.5% | 6.9% | 9.6% | 22.1% |

| Motor Vehicles | 2.5% | -3.9% | 17.9% | -6.1% | 11.3% | 16.2% | 40.7% |

| Imports Goods % | 3.9% | 3.6% | 2.9% | 35.8% | 13.7% | 11.4% | 24.1% |

| Motor Vehicles | -25.2% | -7.5% | 9.8% | -84.4% | -53.1% | -27.4% | -23.3% |

| Prices in %, SAAR | 3-Mos | 6-Mos | 12-Mos | 12 mos Ago | |||

| Export Prices | 0.1% | -1.3% | 0.7% | -5.3% | -10.4% | -1.8% | 1.4% |

| Import Prices | 4.9% | 0.7% | 3.8% | 37.2% | 10.0% | 12.6% | 6.6% |

| Memo: Yen/$, AVG, Level | 112.45 | 111.07 | 115.87 | 113.13 | 115.43 | 117.76 | 116.35 |

| Memo Yen Percent ('-' is a fall) | -1.2% | 4.1% | -0.7% | 13.9% | 16.0% | 4.2% | 1.0% |

by Robert Brusca January 24, 2008

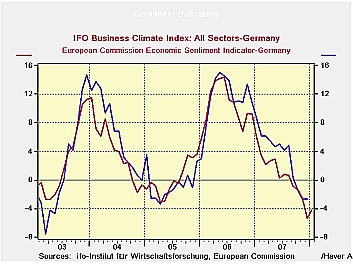

Bounce raises the question of EMU-US de-coupling.

Apparently Germans agree… They agree with the ECB that

weakness does not threaten Germany or Europe and they see better times

ahead as the IFO expectations index that looks six months into the

future rose enough to kick the climate index higher. No wonder Axel

Weber, Bundesbank president, was saying that markets do not understand

the ECB and are too driven by short-term horizons. Weber, in comments

today, hinted that the next ECB move could be to tighten, not to ease

as markets had expected just yesterday.

These events raise the question of whether markets have

de-coupled or whether either Europe’s or the US central bankers are

just plain wrong about the outlook. Can Europe be so strong that it may

need to tighten if the US is as weak as all the fiscal and monetary

stimulus in train seem to expect? Or is Germany and the ECB simply

wrong in their outlook? Or is the Fed and Congress wrong and just too

wrapped up in the needs of US short-term presidential election year

politics?

We can’t tell here and now, but time will tell.

The respondents to the IFO survey did see somewhat weaker

current conditions, but not much weaker. At a value of 107.9 the

current index is still in the top quartile of its range. It slipped by

just 0.2 points in January, less than in December. It is still well

above its average value of 95.0. It is lower year/year by 4.2%, less

than the 6.2% drop registered on that basis in December.

Business expectations improved by 0.8% in Germany. This

propelled the overall climate index up to 103.4 from 103.0 in December.

Expectations are still lower by 4.1% Yr/Yr less than the 4.3% drop

registered in December. But the IFO survey is hardly a report ringing

warning bells in the ears of the ECB.

The overall EU index for Germany had already slowed its rate

of descent in December. Now the IFO actually has improved. We seem to

have a decoupling in progress if the actions of the ECB and the Fed are

each correct. The question is: are they?

| IFO Survey: Germany | ||||||||

|---|---|---|---|---|---|---|---|---|

| Jan-08 | Dec-07 | Nov-07 | Oct-07 | Sep-07 | Aug-07 | Jul-07 | Jun-07 | |

| Biz Climate | -4.2% | -5.3% | -2.5% | -1.4% | -1.0% | 0.7% | 0.8% | 0.3% |

| Current Situation | -4.3% | -6.2% | -3.2% | -2.1% | -1.3% | 2.5% | 2.4% | 1.6% |

| Biz Expectations | -4.1% | -4.3% | -2.0% | -0.8% | -0.4% | -1.1% | -0.9% | -1.3% |

by Robert Brusca January 24, 2008

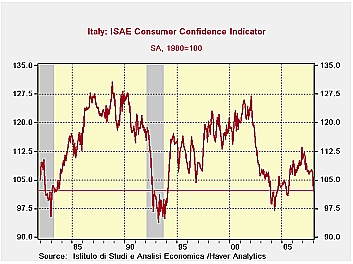

Italy shivers while the Euro Area overheats: What good can

come of this?

Not only is PM Prodi having a difficult time, but so is the

Italian consumer. Whatever fate awaits Prodi, the consumer is already

giving a vote of no-confidence to it. This is despite some resilient

data from elsewhere in the Euro Area. The German IFO index actually

rose in January. The ECB is thinking of hiking rates according to some

of the day’s commentary. If you are an Italian consumer however, you

must wonder if the world has gone mad. The Euro Area may be coming into

one of its really big tests. Inflation has run hotter in some EMU

countries than in others. But because of the single currency there has

been no relief for competitiveness. There is no local currency to

depreciate. Italy is one of those regions.

Since all EMU countries are pent up in the same currency area,

what will affect competitiveness within the Zone, as well as between

the Zone and other areas that is nationally different, is the local

inflation rate, as well as any productivity differences. The small

table below shows that since March of 2000 Finland is the most

competitive EMU nation with a national price index that is some 7.2%

below the EMU average for that period. Germany is next at -4.2%. Italy

ranks as seventh worst among the 12 countries ranked here with a price

level that is 1.2 percentage points ABOVE the EMU average. That would

make Italy some 5.4% less competitive than Germany for the period and

8.4% behind Finland. Ranking below Italy is The Netherlands,

Luxembourg, Portugal, Ireland, Spain and Greece.

| Is the Italian Consumer an Example of…Trouble in the Zone? | |||

|---|---|---|---|

| HICP | March 2000 | High to Low | Gap |

| Sep-07 | Rank | W/EMU | |

| Austria | 16.5% | 10 | -2.6% |

| Belgium | 18.1% | 8 | -1.0% |

| Finland | 11.9% | 12 | -7.2% |

| France | 17.1% | 9 | -2.0% |

| Germany | 14.9% | 11 | -4.2% |

| Greece | 30.2% | 1 | 11.1% |

| Ireland | 28.6% | 3 | 9.5% |

| Italy | 20.3% | 7 | 1.2% |

| Luxembourg | 25.3% | 5 | 6.2% |

| The Netherlands | 21.1% | 6 | 2.0% |

| Portugal | 27.0% | 4 | 8.0% |

| Spain | 29.0% | 2 | 9.9% |

| EMU Total | 19.1% | -- | -- |

If Italy’s problems are due to that sort of competitiveness

loss we should also find encroaching weakness in those lower ranked

countries as well.

For now, whatever the source, Italy’s consumers are feeling

the pinch. Confidence is in the bottom 20% of its range. The current

overall situation is in the bottom six percent of its range. The

expected overall situation in the next 12 months is the worst in this

period. And so on, see the percentile column in the table above. The

Italian household sees things as being bad, and as getting much worse.

It is no wonder Prodi is having trouble, and it will be a real test of

European unity to see what happens in Italy if the ECB goes ahead with

the rate hikes that the Bundesbank’s Weber was warning of today.

| Italy ISAE Consumer Confidence | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| Since January 1999 | ||||||||||

| Dec 07 |

Nov 07 |

Oct 07 |

Sep 07 |

%tile | Rank | Max | Min | Range | Mean | |

| Consumer Confidence | 107 | 107.6 | 107.3 | 107.3 | 33.3 | 63 | 127 | 97 | 30 | 111 |

| Last 12 months | ||||||||||

| OVERALL SITUATION | -69 | -71 | -67 | -63 | 23.0 | 69 | -22 | -83 | 61 | -55 |

| PRICE TRENDS | -21.5 | -24.5 | -23.5 | -26.5 | 29.6 | 61 | 4 | -32 | 36 | -16 |

| Next 12months | ||||||||||

| OVERALL SITUATION | -35 | -35 | -33 | -30 | 0.0 | 99 | 24 | -35 | 59 | -13 |

| PRICE TRENDS | 28 | 25.5 | 26 | 31 | 50.0 | 40 | 49 | 7 | 42 | 23 |

| UNEMPLOYMENT | 4 | 3 | 2 | -2 | 87.2 | 8 | 9 | -30 | 39 | -6 |

| HOUSEHOLD BUDGET | 9 | 6 | 6 | 5 | 29.4 | 60 | 33 | -1 | 34 | 14 |

| HOUSEHOLD FIN SITUATION | ||||||||||

| Last 12 months | -44 | -43 | -44 | -39 | 7.5 | 95 | -7 | -47 | 40 | -29 |

| Next12 months | -14 | -12 | -14 | -13 | 0.0 | 99 | 14 | -14 | 28 | -2 |

| HOUSEHOLD SAVINGS | ||||||||||

| Current | 60 | 63 | 58 | 54 | 93.0 | 2 | 63 | 20 | 43 | 39 |

| Future | -37 | -39 | -42 | -33 | 15.2 | 97 | -9 | -42 | 33 | -24 |

| MAJOR Purchases | ||||||||||

| Current | -47 | -48 | -45 | -42 | 23.8 | 60 | -15 | -57 | 42 | -41 |

| Future | -61 | -63 | -66 | -65 | 38.7 | 41 | -42 | -73 | 31 | -62 |

| Total number of months: | 100 | |||||||||

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief