Global| Sep 12 2014

Global| Sep 12 2014European Manufacturing Falls Further Behind the U.S.

Summary

Euro area industrial output showed a strong rebound of 1% in July from its decline of 0.3% in June. However the gain is still not persuasive. In the new quarter, the quarter-to-date calculations show a rise in output at a 2.7% pace [...]

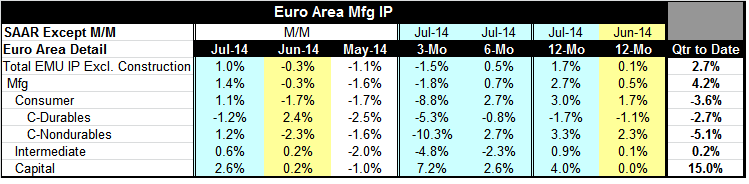

Euro area industrial output showed a strong rebound of 1% in July from its decline of 0.3% in June. However the gain is still not persuasive. In the new quarter, the quarter-to-date calculations show a rise in output at a 2.7% pace that is developing, wholly on the back of this month's rise against a background of chronic weakness. Trends still point lower, just about across the board. Taking this month's gain to heart would seem to be a mistake or an act of hope.

Euro area industrial output showed a strong rebound of 1% in July from its decline of 0.3% in June. However the gain is still not persuasive. In the new quarter, the quarter-to-date calculations show a rise in output at a 2.7% pace that is developing, wholly on the back of this month's rise against a background of chronic weakness. Trends still point lower, just about across the board. Taking this month's gain to heart would seem to be a mistake or an act of hope.

The three-month growth rate for total output is still withering as the 12-month growth rate erodes from 1.7% to 0.5% over six months to -1.5% over three months. This erosion is in play for all the IP components except for capital goods.

Capital goods output alone is on an accelerating path. Output growth is 4% over 12 months. That slips to 2.6% over six months but it rebounds to a 7.2% pace over three months - underpinned by back-to-back monthly gains in June and July.

Two days ago we looked at the composition of IP growth across EMU members. Since then, Italy has also reported. With nine of the first euro area members reporting, four have sales falling and five have sales rising. That is not a strong endorsement of a new trend. Moreover, the German gain of 2.6%, given Germany's weight, is responsible for much of the rebound. There are still eight of nine reporting EMU members with output decelerating over three months; Germany is the sole exception there.

While the July rebound in industrial output surpassed our expectations, we should be careful about extrapolating this good news. The breadth of industries as well as the breadth of EMU members show us that weakness is still the predominate trend in Europe. With new sanctions on Russia and counter measures from Russia still in store, who knows what impediment is next? Poland is already struggling under a cut to its fuel supplies. While there is a pending truce in Ukraine, there is no telling how long it will hold or even if it does hold how events there will shape up. We should not expect the Russians to `play fair.' There is still a good deal of uncertainty in the world, and not all of it is in Ukraine. The Middle East is getting hotter with the U.S. promising action in Syria and the Russians - of all people- arguing that U.S. action there would be against international law. Crimea? Ukraine? Those Russian must have a great sense of humor. Nonetheless, all this conflict raises uncertainty and becomes an impediment to growth.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief