Global| Aug 16 2017

Global| Aug 16 2017European GDP...Breaking Good

Summary

GDP growth strengthens in Europe. Not only is GDP growth strengthening for the EMU as a whole, the sense of firming growth is spreading within the community. Better...but is 'better' good enough? EMU growth is up to 2.5% annualized [...]

GDP growth strengthens in Europe. Not only is GDP growth strengthening for the EMU as a whole, the sense of firming growth is spreading within the community.

GDP growth strengthens in Europe. Not only is GDP growth strengthening for the EMU as a whole, the sense of firming growth is spreading within the community.

Better...but is 'better' good enough?

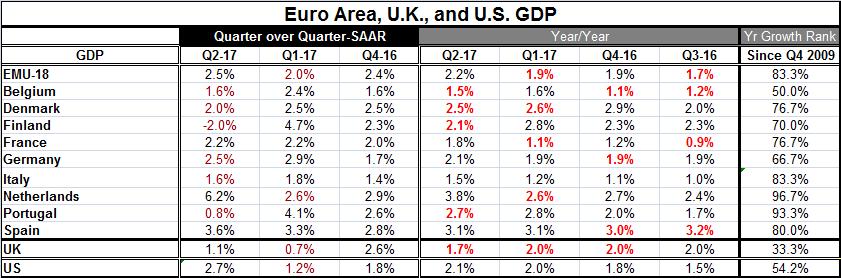

EMU growth is up to 2.5% annualized from 2.0% in Q1. The year-on-year pace in Q2 is up to 2.5%. These are not stellar growth rates by historic experience, but they are solid by the new standards of the new normal in which mediocre gets at least 'B' on an 'A to F' scale of grading.

Not just a bed of roses...thorns too

Still, six of the original ten members reporting GDP in this table demonstrate quarter-to-quarter declines in their respective GDP growth rates. Four of them (plus the U.K.) show declines in their respective year-over-year rates of growth compared to the pace reported last quarter. However, the year-on-year slowdowns are mostly reported in some of the smaller EMU economies: Belgium, Denmark, Finland and Portugal. This quarter (so far) only Finland has reported a drop in GDP for the quarter. And beside that, only Portugal has an annualized gain in Q2 that is less than 1%.

The big news...

The big news, which has been in the making for some time beginning with better PMI data, is France whose GDP quarterly growth rate is up to 2.2% and to 1.8% year-over-year and is no longer looking like the anemic economy among the Big Four. However, Italy, another Big Four economy, saw quarterly growth decelerate in Q2 although its year-on-year growth performance continues to make gains. Those gains, while steady, are also slow and only have the Q2 Italian growth rate up to 1.5% year-on-year.

Mixed performance and choices

In Q2, only Belgium, France and Italy log year-on-year growth rates of less than 2%. That compares to four countries including all of the EMU in Q1 with growth less than 2%. Growth rates evaluated since Q4 2009 find year-on-year growth rates standing at or above the 70th percentiles of their respective historic queues of data in all of these countries except two: Belgium and Germany. The U.K. has slipped to a weak 33rd percentile standing on this same basis. By comparison, the U.S. logs a 54th percentile standing and the Fed has a tightening program that is well under way on year-over-year GDP growth that is now slower than in the EMU. Is the EMU different? Being prudent? Getting behind the curve?

Pressure!

Clearly, with the metrics turning to growth, the ECB is going to feel more pressure to move even though inflation is still below its objective and has been underperforming for a long stretch of time.

Draghi: set to not make news

Today we are getting reports from a source 'close to Mario Draghi' that he will not be tipping off any new policy initiatives at the Fed's upcoming symposium in Jackson Hole, WY. Draghi will attend and participate but will stay 'on topic' and not report any new policy moves.

Central bankers on a hot tin roof

It is an interesting and perhaps touchy time for central banks to make policy. Globally, inflation is undershooting central bank targets. Growth is hanging in there and at a pace that looks more solid since it just keeps on coming but at a pace that is unimpressive and still leaves a lot of people behind. The U.K. has reported today a 42-year low in the unemployment rate. Germany has been reporting the lowest unemployment rates since reunification. The U.S. is worried about its low unemployment rate and yet low unemployment does not raise wages or inflation. For central banks operating with an inflation objective (and like the ECB that has only that objective), it is hard to justify rate hikes in this environment. Yet, the ECB still has some special stimulus programs it could pull back. And central banks can always raise rates on judgement even if the inflation rate is not rising. And this is easier to do when interest rates are well below historic norms as they are now but....

Anyone for tennis?

The 'but' in all of this is that if central banks act on judgement in lieu of facts their judgement had better be right. For example, in the U.S. over 90% of the drop in the unemployment rate can be explained by shifting rates of labor force participation. That means less than 10% is left to be explained by economic performance. If that is a real relationship (not just a spurious statistical correlation), then policy is not on such firm ground in seeking higher interest rates as it may seem. Moreover, it is well realized that we are in an era of a new normal and yet poorly realized as to what the new normal is or what it means. Trying to get interest rates back to old normal in a time of new normal could be a risky and even a dead wrong proposition. But the ball has moved squarely into the court of the central banks and now they have to decide how to play it. Do they want to hit it back and continue the rally or is time to change things up and go for a winner and risk an unforced error?

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief