Global| Oct 16 2020

Global| Oct 16 2020European Car Registrations Rise in September But Do So in Reverse Gear

Summary

September marks the first year-on-year gains in car registrations for 2020. Registrations are now up by 2.9% over September of one-year ago. Sales also show growth surging strongly over six months and over three months, but the pace [...]

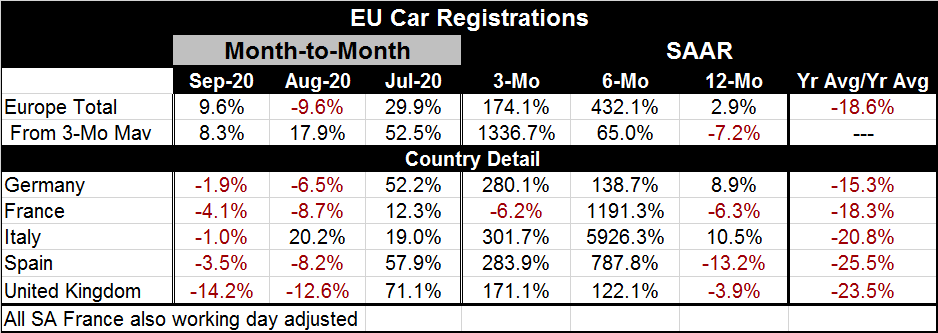

September marks the first year-on-year gains in car registrations for 2020. Registrations are now up by 2.9% over September of one-year ago. Sales also show growth surging strongly over six months and over three months, but the pace is slower over three months compared to six months. So this is no run-a-away rebound. Arguably, strength already has had its day in the sun.

September marks the first year-on-year gains in car registrations for 2020. Registrations are now up by 2.9% over September of one-year ago. Sales also show growth surging strongly over six months and over three months, but the pace is slower over three months compared to six months. So this is no run-a-away rebound. Arguably, strength already has had its day in the sun.

Chart "Motor Vehicle Registrations" shows that the impact of the virus seems to have hit all four countries pictured in the graph about the same with about the same timing. But that conclusion depends on what you consider 'about the same.' While the topography of the various series shows a great deal in common, the year-on-year growth rates still show considerable differences. Germany and Italy are leading Europe to recovery as they are the only two countries in the table with year-on-year increase in registrations. Registrations in Italy are up by 10.5% y/y while those in Germany are up by 8.9% y/y.

France, Spain and the United Kingdom continue to see year-on-year sales contracting. While the data are seasonally adjusted - and auto sales are quite seasonal- there is no getting around the fact that sales in September are backing into their first year-on-year increase of 2020. All five countries in the table show month-to-month declines in sales in September. And four of the five show declines in August as well. Germany and Italy that lead the year-on-year gains do so by logging the smallest month-to-month declines in the group for September.

Maybe this month is a watershed for car registrations and maybe it isn't.

The smoothed year-average over year-average data show a lot more uniformity with Italy, Spain and the U.K. showing registration declines of 20% to 25% while France and Germany notch slightly smaller declines at 18% and 15%, respectively.

This chart shows the forest instead of the trees. European unit vehicle registrations are plotted. In this graphic, it is easier to see that the rise in European sales in September has more to do with a weaker comparison for one year ago than it has to so with any pickup in registrations in September 2020 (since the latter simply did not occur except among a scattering of unnamed, smaller, countries). Comparisons with a year ago will get tougher in October. That will give way to an easier comparison in November then toughen up in December. However, all the comparisons from 2020 (once we get to the year-on-year calculations in 2021) will be easy.

This chart shows the forest instead of the trees. European unit vehicle registrations are plotted. In this graphic, it is easier to see that the rise in European sales in September has more to do with a weaker comparison for one year ago than it has to so with any pickup in registrations in September 2020 (since the latter simply did not occur except among a scattering of unnamed, smaller, countries). Comparisons with a year ago will get tougher in October. That will give way to an easier comparison in November then toughen up in December. However, all the comparisons from 2020 (once we get to the year-on-year calculations in 2021) will be easy.

While retail sales volumes have recovered somewhat better than vehicle registrations, there is still a huge hurdle to sales ahead. It is, by now, a familiar impediment. The virus has once again encroached on reality and Europe is seeing restrictions on economic activity imposed quite broadly across the continent. This will likely adversely impact car sales and registrations.

However, as we ponder the future for vehicle registrations, the future is not grim simply because of the pick-up in the presence of the virus. It is also the weak trends for sales across countries. Demand to purchase vehicles simply has not responded in the recovery. Of course, next year's numbers will be blockbusters on the year-over-year comparisons that will not signify anything of importance. Until we get there, Europe will still have to navigate through the uncertainties of virus control.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief