Global| Aug 22 2007

Global| Aug 22 2007Euro Orders are Quite Firm Within the Zone but Extremely Strong for "Exports"

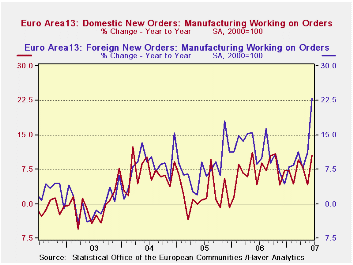

Summary

Euro area domestic orders are fine but are slower than export orders - both are accelerating over 3 months. The UK alone (not a Euro area member) shows orders weakening but the CBI survey shows gains in August. We are left with a bit [...]

Euro area domestic orders are fine but are slower than export orders - both are accelerating over 3 months.

The UK alone (not a Euro area member) shows orders weakening but the CBI survey shows gains in August. We are left with a bit of uncertainty about Europe. But nothing has truly been weak apart from the episodic experience of things like UK orders weakening then rebounding. There are more substantial hints of slowing, but none of weakness. And during the liquidity squeeze the Euro has lost some ground, a factor that is good for Euro area growth prospects.

While there is some irregularity in the Euro area, Italy and France have showed the most consistent signs of weakness among large economies, although French industrial orders have emerged again as strong after some weakness. The ECB is under pressure to not hike rates and today the French finance minister proves there is at least a side and one-half to every argument, by making a case for a rate cut from the ECB. Yes I said (he said) ‘cut’.

Within the Euro area there is this odd result that domestic orders are softer while export orders are strong and accelerating strongly. Exports still undertake a national definition in these data. So export orders from Germany to a French firm would be export orders to France but would still reflect internal EMU orders. This sort of thing makes it a bit hard to sort out what is in train here. For now domestic orders are a bit weaker but are not suspect since they are accelerating, too. Europe’s slowdown may be in progress but it does not seem to be anything more serious than that.

| Saar except m/m | % m/m | Jun-07 | Jun-07 | Jun-07 | Jun-06 | Jun-05 | ||

| Euro area Detail | Jun-07 | May-07 | Apr-07 | 3-Mo | 6-mo | 12-mo | 12-mo | 12-mo |

| MFG Orders | 4.4% | 1.5% | -0.3% | 24.5% | 17.5% | 15.5% | 6.3% | 5.4% |

| MFG Sales | 0.9% | 0.7% | 0.3% | 8.2% | 7.2% | 7.1% | 7.7% | 3.1% |

| Consumer | 0.5% | 0.4% | 0.3% | 4.9% | 4.1% | 4.8% | 7.7% | 3.1% |

| Capital | 0.5% | 0.4% | 0.5% | 5.7% | 7.3% | 8.2% | 4.0% | 1.8% |

| Intermediate | 0.9% | 0.7% | 0.2% | 10.7% | 4.0% | 10.6% | 6.9% | 2.7% |

| MFG Orders | ||||||||

| Total Orders | 4.4% | 1.5% | -0.3% | 24.5% | 17.5% | 15.5% | 6.3% | 5.4% |

| E-13 Domestic MFG orders | 1.8% | 0.5% | 0.2% | 10.7% | 4.0% | 10.6% | 4.2% | 0.9% |

| E-13 Foreign MFG orders | 8.7% | 3.7% | -2.0% | 48.4% | 30.7% | 23.1% | 8.5% | 9.1% |

| Countries: | Jun-07 | May-07 | Apr-07 | 3-Mo | 6-mo | 12-mo | 12-mo | 12-mo |

| Germany: | 4.7% | 3.2% | -1.5% | 28.3% | 27.2% | 17.9% | 9.7% | 7.1% |

| France: | 5.1% | 2.6% | 0.6% | 38.6% | 26.6% | 8.4% | -0.6% | 9.6% |

| Italy: | #N/A | 2.5% | -0.8% | #N/A | #N/A | #N/A | 10.1% | 4.9% |

| UK: | -1.7% | -2.4% | -6.7% | -35.9% | 12.2% | -7.2% | 10.2% | -2.3% |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief