Global| Aug 13 2008

Global| Aug 13 2008Euro Headline Inflation is Unruly; Core Setting Down

Summary

The inflation story in EMU/EU is clear but not uncomplicated. Inflation at 4% Yr/Yr has accelerated in terms of its headline the only measure the ECB claims to have designs on. But oil prices have dropped. That should pave the way for [...]

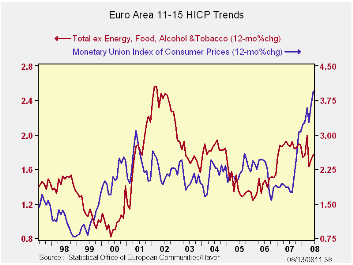

The inflation story in EMU/EU is clear but not uncomplicated.

Inflation at 4% Yr/Yr has accelerated in terms of its headline the only

measure the ECB claims to have designs on. But oil prices have dropped.

That should pave the way for better times ahead. Mover over, the core

rate of inflation is 2.5% Yr/Yr - still ‘too high’ - but its sequential

growth rates show that core inflation has been decelerating over the

recent 6-mos and three months. Moreover, this core deceleration is

observable across some key EMU countries including Italy.

The most troublesome inflation patterns are in the UK. The BOE

has the same 2% inflation ceiling as the ECB. But its headline Yr/Yr

inflation rate is at 7.3% and really accelerating. Core UK inflation

also is blowing up at a 2.2% rate Yr/Yr, 2.9% over six months and 3.9%

over three months.

The breakdown in global oil prices is good news for all

central banks, but the ECB is still in a bit of an inflation fix. The

ECB is getting in a more nettlesome position since its economy is

starting to show more pronounced weakness as core inflation abates. It

challenge – one it has not faced yet -- might be how to deal with

fading but still over-the-top inflation as growth begins to unwind more

sharply.

| Trends in HICP | |||||||

|---|---|---|---|---|---|---|---|

| % mo/mo | % SAAR | ||||||

| Jun-08 | May-08 | Apr-08 | 3-Mo | 6-Mo | 12-Mo | Yr Ago | |

| EMU-13 | 0.5% | 0.6% | 0.0% | 4.1% | 4.1% | 4.0% | 1.9% |

| Core | 0.2% | 0.2% | -0.1% | 1.3% | 2.3% | 2.5% | 1.9% |

| Goods | 0.4% | 0.8% | 0.6% | 7.6% | 6.0% | 4.9% | 1.5% |

| Services | 0.3% | 0.4% | -0.1% | 2.2% | 2.5% | 2.5% | 2.6% |

| HICP | |||||||

| Germany | 0.5% | 0.6% | -0.4% | 2.7% | 3.2% | 3.4% | 2.0% |

| France | 0.5% | 0.5% | 0.1% | 4.5% | 4.0% | 4.0% | 1.3% |

| Italy | 0.6% | 0.4% | 0.0% | 4.2% | 4.6% | 4.0% | 1.9% |

| UK | 0.6% | 0.5% | 0.7% | 7.3% | 5.4% | 3.8% | 2.3% |

| Spain | 0.6% | 0.7% | -0.1% | 4.9% | 4.5% | 5.0% | 2.4% |

| Core excl FE&A | |||||||

| Germany | 0.1% | 0.3% | -0.5% | -0.4% | 0.8% | 1.8% | 2.1% |

| Italy | 0.4% | 0.2% | -0.1% | 1.9% | 3.1% | 3.0% | 1.9% |

| UK | 0.3% | 0.3% | 0.4% | 3.9% | 2.9% | 2.2% | 2.2% |

| Spain | 0.3% | 0.3% | -0.1% | 2.2% | 2.6% | 3.4% | 2.5% |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief