Global| Apr 08 2010

Global| Apr 08 2010Euro-Consumer Remains Sluggish

Summary

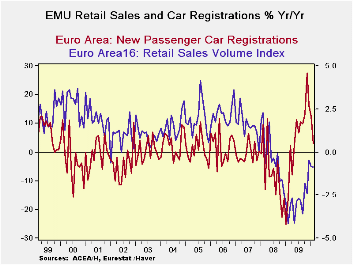

The Euro consumer is not helping to lead growth to the Promised Land. Retail sales came up lame in February after rising by just the thinnest margin of 0.1% in January. The growth rate for retail sales is steady over 3-and 6-months at [...]

The Euro consumer is not helping to lead growth to the Promised Land. Retail sales came up lame in February after rising by just the thinnest margin of 0.1% in January. The growth rate for retail sales is steady over 3-and 6-months at under 1.5% in nominal terms. The lift from auto sales is going, going gone as purchase incentive plans have ended and the bulge in vehicle registrations is unwinding fast. Retail sales in Germany, the big EMU economy, are off for two months in a row. There is no leadership there.

Greece’s problems continue to worsen and to hang over growth prospects for the Zone. No one is sure just what will happen, but speculation is rife and that makes things worse. The German hard line on Greece that delivers election protection to Angelina Merkel can’t make the Zone look like a very attractive place to be. The cry we heard in the past, ’we are all Europeans now,’ rings hollow. They are all Europeans until a crisis hits then they are German, French, Greek and etc. For now Greek bonds are suffering their widest spreads to bunds since EMU was formed; credit default protection is getting to be very expensive for Greek paper. A few market pundits push for Greece to default but for the most part that is a fringe faction. Most realize the potential dangers from such an event and the risk of knock-on effects from having Greece actually default. Just think of the US and what happened when Lehman Brothers failed. It is often hard to predict the fallout from such events; German banks already hold a lot of Greek bonds on their balance sheets.

Meanwhile the Germans are being tough on Greece. One must wonder if Greece at some point does not simply succumb to the pressure and call the German bluff and let the forces of default begin to run their course, forcing Germany to either to deal with the fallout of default or to back Greece more solidly. In the meantime the Greek tragedy plays out as one of Europe’s longest running sold-out performances. Uncertainty about Greece continues to adversely impact growth in the Zone.

The main bright news for Europe has come from the UK where industrial output has risen strongly (compared to flat output in Germany this month) and rising home prices. The Bank of England is continuing to given the markets there assistance with securities purchases. Still growth in the UK is less than stellar, that’s why the BOE is still providing market support after all.

The US recovery is looking better… then bleaker. While the data clearly have improved, the jobless claims report from the current week has shot up to a five-week high making it clear that jobs growth is mounting no head of steam in the wake of the March jobs report. It’s time to go back to playing fantasy baseball, not fantasy recovery. The Fed Chairman is making it clear that job growth is not significantly in gear, dashing the value of any analysis that was arguing that the Fed is on the brink of a rate hike after one lukewarm job report.

Clearly the global economy is still sputtering. While the US expansion seems to be the strongest that is in train; it continues to be unable to get the various jobs metrics on the right path together with any speed. Consumers remain the key to the global recovery since there are many nations with the ability to supply goods. Germany and China and Japan are exporting again. The US is exporting, too. But exports need consumers, and consumers are holding back, especially in Europe. Investment demand is not enough by itself to drive the kind of recovery that the world needs.

| Euro-Area Retail Sales | ||||||

|---|---|---|---|---|---|---|

| M/M | Saar | |||||

| Feb-10 | Jan-10 | Dec-09 | 3-Mo | 6-MO | 12-Mo | |

| Zone Total Value | 0.0% | 0.1% | 0.2% | 1.4% | 1.3% | -0.5% |

| Food,Bev Tobacco | -0.1% | -0.1% | -0.2% | -1.8% | -2.1% | -2.1% |

| Registrations: | ||||||

| Motor Vehicle Reg | 2.6% | -0.8% | -3.0% | -5.0% | -1.0% | 5.6% |

| NonFood Country detail: Volume | ||||||

| Germany Value | -0.4% | -0.5% | 1.0% | 0.4% | 0.8% | -0.9% |

| UK(EU) Volume | 2.1% | -3.0% | -0.2% | -4.5% | -0.7% | 3.4% |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief