Global| Dec 05 2016

Global| Dec 05 2016Euro Area Win/Win: PMIs Improve and Retail Sales Improve

Summary

The EMU services gauge finalized shows a lift to 53.8 in November from 52.8 in October. The services, manufacturing and total PMI sector gauges are above their 12-month, six-month and three-month values in November, signaling ongoing [...]

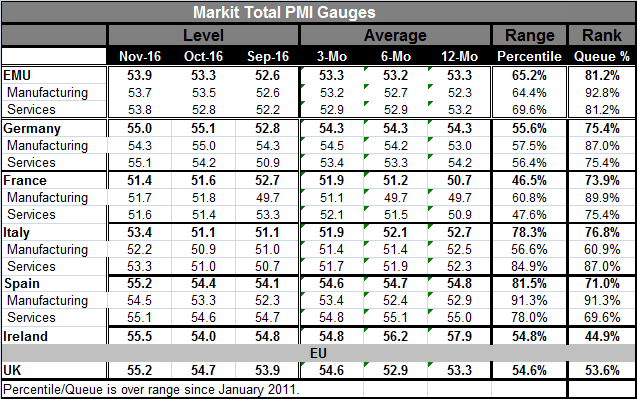

The EMU services gauge finalized shows a lift to 53.8 in November from 52.8 in October. The services, manufacturing and total PMI sector gauges are above their 12-month, six-month and three-month values in November, signaling ongoing upward momentum. Compared to the past six years, the EMU gauge stands in the top 19% of its queue of values. The manufacturing reading is in its top 8th percentile while services stand in their top 19th percentile. From a long-run standpoint, these PMI values are more like normal readings but normal is something that Europe has not been looking at for quite some time.

The EMU services gauge finalized shows a lift to 53.8 in November from 52.8 in October. The services, manufacturing and total PMI sector gauges are above their 12-month, six-month and three-month values in November, signaling ongoing upward momentum. Compared to the past six years, the EMU gauge stands in the top 19% of its queue of values. The manufacturing reading is in its top 8th percentile while services stand in their top 19th percentile. From a long-run standpoint, these PMI values are more like normal readings but normal is something that Europe has not been looking at for quite some time.

PMI performance in EMU

The queue percentile standings of the German and French indices are weaker than for the EMU as a whole, but by relatively small amounts. Italy is an exception as Italy's manufacturing sector is much worse in its queue standing than that for the EMU has a whole, but its services sector is relatively better. Spain shows a similar standing in its manufacturing sector but has a much weaker services sector. But Spain and Italy both show overall current PMI readings higher than their respective ongoing three-month, six-month and 12-month averages. Germany and France show slightly less robust momentum. But EMU-area PMI readings are generally on firm-to-firming trends.

Retail sales in EMU

Another piece of goods news is the rise in EMU retail sales that shook off two months of weakness. Euro area retail sales volumes advanced by 1.1% in October after two months of declines. That gain boosted the three-month growth rate to 2.3% (annualized). While a solid pace, it is slightly lower than its year-on-year pace of 2.5%. And motor vehicle registrations have slowed sharply in the euro area with registrations off by 13.1% in October and declining at a 7.9% annual rate over three months -10.4% over six months and posting a 0.8% drop over 12 months.

Sentix index of sentiment drops

The Sentix index of investor sentiment dropped to 10.0 in December from 13.1 in November. That setback was unexpected. What had been expected was the defeat of the Italian referendum which now has destabilized the view of what is going on in Italy as well as in Europe.

Italian referendum implications

Italy adds its voice to that of the U.K. and as voters reject a plan concocted by its leaders. For Italy, the referendum was a plan to streamline the Italian system and to make change easer to implement. Renzi had planned to push through labor market 'reforms' and these obviously are not wanted by the voters/workers. The U.K. already stuck down its long standing membership in the EU. In the U.S., a mainline political candidate widely believed to be the favorite lost to the upstart non-politician, Donald Trump. And in other European nations, elections are pending for the year ahead. Take the polls as indications of how the voters are leaning at your own risk! The defeat of Renzi in Italy could bring to power groups that favor pulling Italy out of the euro area that want to implement a two-track euro-currency.

La dolce vida?

By and large, Italians- when polled- still favor euro area membership. Still, the rejection of Renzi leaves Italy without a clear direction and we have seen the inability of polls to diagnose what people really think and want. It also is unclear where the rest of Europe will be headed. Markets did not reacted as violently to the Italian results as expected, an indication that most do not see the Italian separatist parties gaining full control. And the 'no' vote on the Italian referendum has been something markets have been preparing for. It was not a surprise. But the rejection of 'reform' and 'modernization' and more 'centralized control' is now official. It does pose new hurdles for Italy and for Italian banks in particular.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief