Global| Apr 15 2016

Global| Apr 15 2016Euro Area Trade Shows a Demand Uptick!

Summary

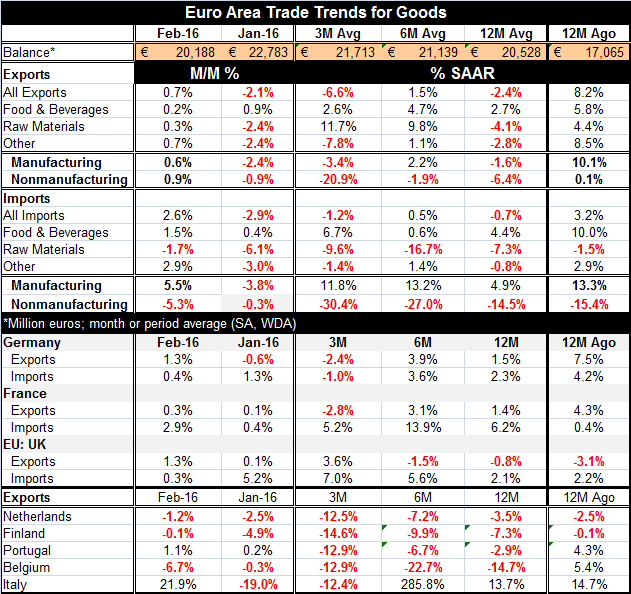

Some distinct divergent trends are starting to emerge and to be reinforced in EMU trade patterns. The first trend is an old one that exports remain weak and may even be weakening further. This is linked, of course, to manufacturing [...]

Some distinct divergent trends are starting to emerge and to be reinforced in EMU trade patterns. The first trend is an old one that exports remain weak and may even be weakening further. This is linked, of course, to manufacturing sector weakness globally and to price weakness that weakens nominal flows in addition to the weakness in real trade flows. Weakness in oil and commodity prices makes nominal growth weaker. That adds up to even weaker nominal flows.

Some distinct divergent trends are starting to emerge and to be reinforced in EMU trade patterns. The first trend is an old one that exports remain weak and may even be weakening further. This is linked, of course, to manufacturing sector weakness globally and to price weakness that weakens nominal flows in addition to the weakness in real trade flows. Weakness in oil and commodity prices makes nominal growth weaker. That adds up to even weaker nominal flows.

Nonmanufacturing trade flows are weak

In the EMU, we see declines in all nonmanufacturing flows for exports and imports from three-month to six-month to 12-month. There is weakness enough that we can be sure it is there for export volumes with declines on both the export and import sides. The plunge is generally worse for import flows than for export flows, but it is considerable on both sides of the trade ledger. Volume and price weakens are reinforcing.

Manufacturing has different export and import trends

In the EMU, manufacturing exports are weak, falling over 12 months and three months despite a slight uptick in February. But manufacturing imports are showing positive and quite firm growth rates over 12 months, six months and three months that stop just short of being an ongoing accelerating trend. Manufacturing imports rose by a sharp 5.5% in February after a down draft of -3.8% in January.

Weak global demand vs. strengthening demand in EMU

These trends speak of ongoing international weakness where falling prices are mixing with the depressing effect of weak commodity prices on developing economies' growth worsening economic results. The global weakness in manufacturing is broad-based also depressing flows generally. But the import data suggest that in the EMU, despite all the same depressing effects, demand has grown firm enough that volume effects are swamping price effects for trade in manufacturing. This suggests that domestic demand in the EMU has been revived (to some extent). While that is not good for the prognosis for the European trade surplus (which fell to a four-month low in February), it is good news for the region generally and good news for the rest of the world to see someplace where domestic demand may be perking up.

Both retail and auto sales are on the rise in EU

Both retail and auto sales are on the rise in EU

The chart of the EU retail sales volume and passenger car registrations makes the point on revived domestic demand. The retail sector has been the best performing sector in terms of the EU Commission sector diffusion indices for some time. Passenger car sales have been solid performers since late 2012, perhaps not as strong as in the U.S. but nonetheless very solid and supportive to growth. We plot this chart in terms of the levels of the two indices to avoid the problem of setting a base from which to calculate growth. In presenting the data in this fashion, we can see that retail sales volumes are only just getting back to prerecession peaks while passenger car registrations are still well below those peaks and seemingly have much more room to run.

Real trends

Of course, over time the population grows, income grows and we expect sales levels to advance (both of these are expressed in real terms; constant dollars for retail sales and at a saar pace for unit sales for passenger car registrations). But Europe's rebound has been more than just perfunctory.

Some mixed trends within Europe

Still, within Europe, we see mixed trends for vehicle registrations. In Spain, sales are slowing rapidly after several years, as incentives have been taken off. There are still, for the most part, incentives in place for electric vehicles which are still being favored in Europe despite the ratchet down in global energy prices. Due to the role of taxes on fuel costs, European fuel costs are still much higher than in America, for example and fuel conservation is still more economic. Europe has other issues as its banks are still struggling and growth and demographic trends have been subdued. There are also challenges stemming for the need to deal with migrants that affect the evolution of growth and consumer spending. Vehicle sales, while expected to slow this year, are expected to continue to advance.

Trade flow and domestic signals agree

We see in trade data and in domestic consumer spending trends some clear reinforcing signs of revival. The ECB may take heart that some of its programs may be working although the impact on actual rates of growth is still quite subdued. But there is much more of a sense of so far so good in this month's trade report than there has been in the recent past. It may be surprising to see such robust imports coupled with weak export performance because of the weakness of the euro on world markets. Of course, early in the year, the euro did demonstrate some strength. But the exchange rate still has European goods as very competitive on global markets and that also makes imports into the EMU relatively expensive and should help to deflect them. The fact that manufacturing imports are being attracted and not deflected is another aspect of the apparent strength being exhibited by domestic demand in Europe...at least for the moment.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief