Global| Apr 22 2016

Global| Apr 22 2016Euro Area Still Struggling...with Its Growth and Its Culture

Summary

The EMU flash readings for manufacturing and services tell a pretty clear story of the euro area's ongoing struggle to sustain stronger growth. Both sectors remain above 50, showing expansion. But neither is impressively or even [...]

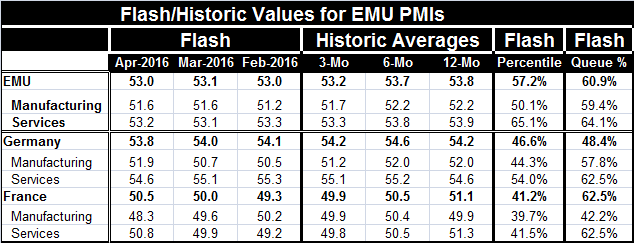

The EMU flash readings for manufacturing and services tell a pretty clear story of the euro area's ongoing struggle to sustain stronger growth. Both sectors remain above 50, showing expansion. But neither is impressively or even comfortably strong. The composite index (not pictured) stands in the 60.9 percentile of its historic queue with manufacturing at its 59.4 percentile and services at their 64.1 percentile.

The EMU flash readings for manufacturing and services tell a pretty clear story of the euro area's ongoing struggle to sustain stronger growth. Both sectors remain above 50, showing expansion. But neither is impressively or even comfortably strong. The composite index (not pictured) stands in the 60.9 percentile of its historic queue with manufacturing at its 59.4 percentile and services at their 64.1 percentile.

Germany has the Iron-man economy of Europe but does its thing by being stuck in second gear and just powering ahead over everything in its path. It grows when other economies won't and is undaunted by low inflation. The German unemployment rate is at a reunification low, but its sector PMI gauges are below their usual standards. At 53.8, the raw German composite PMI gauge stands higher than the EMU gauge, but its relative performance is worse as the German composite stands only in the 48th percentile of its historic queue of data below its historic median. Its manufacturing sector at a diffusion reading of 51.9 exceeds the EMU gauge (at 51.6) but stands only in its 57.8 percentile. German services slipped month-to-month, dropping back to a 54.6 diffusion value, still above the 53.2 reading for the EMU. But German services hold only to a 62.5% percentile standing in their historic queue of data, below the standing for the EMU.

We compare France to nothing else, since nothing is quite like it. France is a picture of lethargy. Its PMI gauges wrap and wind around the neutral compass point of 50. But make no mistake about it: French trends are slipping. This month manufacturing has dipped below 50 and services have risen above it. At 48.3, the French manufacturing PMI is at its weakest since March 2015- one year ago. The French manufacturing sector has a queue standing in only the 42nd percentile of its historic queue of data, well below its median. French services at a diffusion level of 50.8, nonetheless, have a respectable queue standing in their 62.5 percentile. French services have been so weak historically that this is a relatively `firm' queue standing despite its slight increment above neutral that would be positioned perilously in almost any other nation.

These are not impressive stories of growth for the EMU overall or for its two largest economies. But the region is battling and the ECB is fighting to keep its view of stimulus in play even as German policymakers deride its choices. The ongoing policy split within the EMU has gone well beyond the point where it could be called a healthy dialogue of competing views. There is no competition for the German view which knows no compromise and is held as the gospel truth by Germans because it has worked for them, it fits into their culture and they accept its tradeoffs. They want to project it across the euro area. Most of that area wants nothing to do with it.

I continue to view these interior tensions as substantial cultural challenges for the EMU, not just for its success, but for its existence. It is hard to imagine this union enduring with such draconian differences on policy. The Germans are iron-fisted sure of their course and uncompromising. The rest of Europe is less structured to different degrees. It is hard to see how these different values can really coexist in a zone where there will be only one monetary policy and when there is painful punishment for falling out of compliance. There is little sign of either side really compromising, but of course financially struggling nations are forced to adopt at least for a while the uncompromising austerity measures when they fall out of favor with the euro-rules.

Disagreements over migrants are not the only thing tearing Europe apart. The question is whether Europe will ever be able to make peace over its policy choices as long as its members have such divergent views or whether the divergence itself will lessen. Despite the conflict and pain, there is little evidence of anything budging. There is growth; not much, but some. And maybe even less growth than there is hope for change. And despite that, Europeans claim there is solidarity. If so, it is a very strange beast for outsiders to understand.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief