Global| Aug 03 2007

Global| Aug 03 2007Euro Area Retail Sales Stay in Slowdown Mode

Summary

With Q2 data complete, at least preliminarily, Euro area retail sales are continuing to show lethargy. For the quarter as a whole, retail sales volumes are up by only 0.6% at an annual rate over Q1. This follows a 0.2% result in Q1. [...]

With Q2 data complete, at least preliminarily, Euro area retail sales are continuing to show lethargy. For the quarter as a whole, retail sales volumes are up by only 0.6% at an annual rate over Q1. This follows a 0.2% result in Q1. Food purchases are off by 0.1% at an annual rate in Q2. Nonfood is doing somewhat better with a Q/Q annual rate gain of 1.4%. Still, this is no growth leader.

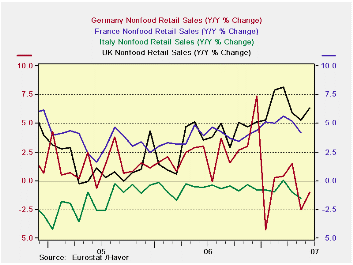

Germany is poised for a normal ‘German recovery’ to take hold – or so officials continue to say. This means that after a trade-led rebound with a strong capital goods sector, the consumer joins the party late. So far there is little evidence that Germany has turned that corner. The VAT hike at year end has surely been a part of the reason. But we are now at mid-year and German sales in Q2 are compared to a VAT distorted and weak Q1. And while Germany’s retail volumes are up at a strong-seeming 6.5% annual rate in Q2/Q1 that compares to a -15.8% drop in Q1, it isn’t really much of a rebound. Year-over-year German sales volumes are off by 0.7%. For all of the Euro area the Y/Y sales gain is 1.0%; nearly twice that for nonfoods at a 1.8% annual rate.

Within Europe the UK (not an EMU member but an EU member and one with a still strong exchange rate) continues to show strong retail sales results. The UK housing market is still strong. The Bank of England, like the ECB, is still warning about inflation pressures and probably is headed for another rate hike. But the UK consumer has been much more active that the typical Euro area consumer. In EMU, unemployment rates are still high, but they have been falling steadily. The proximity to low cost Eastern Europe may be one factor holding back consumer optimism. But one thing is clear, as surely as Europe has had a solid recovery underway, the consumer has been left behind. If Euro area job market improvement continues, this should change, but so far there is little evidence of it and leading economic barometers are showing that a tendency to slow is in the pipeline.

| Jun-07 | May-07 | Apr-07 | 3-Mo | 6-MO | 12-Mo | |

| Euro area 13 Total | 0.4% | -0.7% | -0.1% | -1.3% | -0.6% | 0.9% |

| Food | 0.0% | -0.7% | -0.1% | -3.3% | -0.5% | -0.7% |

| Nonfood | 0.8% | -0.7% | 0.1% | 0.6% | 0.0% | 2.1% |

| Textiles | #N/A | -3.1% | 1.4% | -6.5% | -1.3% | 0.0% |

| HH Goods | #N/A | -0.4% | -1.0% | -1.8% | -2.5% | 1.0% |

| Books news, etc | #N/A | -0.7% | -0.3% | -1.1% | -0.6% | 0.3% |

| Pharma | #N/A | 0.5% | 0.1% | 3.7% | 3.4% | 3.4% |

| Other NonSpec | #N/A | -0.7% | -0.8% | -3.3% | -2.1% | -1.6% |

| Mail Order | #N/A | 1.4% | 0.7% | 1.7% | 3.1% | 0.0% |

| NonFood Country detail;Volume | ||||||

| Germany | 1.6% | -3.4% | 2.2% | 1.2% | -10.0% | -1.0% |

| France | #N/A | 0.0% | 0.1% | 3.6% | 4.3% | 4.2% |

| Italy (Total; Value) | #N/A | -0.2% | -0.5% | -2.1% | -2.2% | -1.6% |

| UK (EU) | 0.9% | 0.3% | -0.1% | 4.7% | 5.2% | 6.4% |

| Shaded areas calculated on a one-month lag due to lagging data. | ||||||

| The EA 13 countries are Austria, Belgium, Finland, France, Germany, Greece, Ireland, Italy, Luxembourg, the Netherlands, Portugal, Slovenia and Spain. | ||||||

| 7COLSPAN | ||||||

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief