Global| Dec 03 2008

Global| Dec 03 2008Euro Area Retail Sales Crash Hard Consumer Spending Plans Continue To Be Cut...

Summary

After Germany reported out such weak sales this month, the gauntlet was thrown down of all of EMU. EMU sales are slipping and doing so at an accelerating pace. They dropped by 0.8% in October alone. The three-month growth rate is [...]

After Germany reported out such weak sales this month, the

gauntlet was thrown down of all of EMU. EMU sales are slipping and

doing so at an accelerating pace. They dropped by 0.8% in October

alone. The three-month growth rate is -2.6% the 6-month growth rate is

-1.6% but that is a bit better than the 12-month pace at -2.3%. Food

purchases are stabilizing to some extent but nonfood sales are in a

slide that is gathering sharp downward momentum.

The growth rates for the PRODUCT CATEGORIES do not show the

slowing in the headlines because they are only current through Sept. It

seems that much of the weakness in nominal sales is recent and is

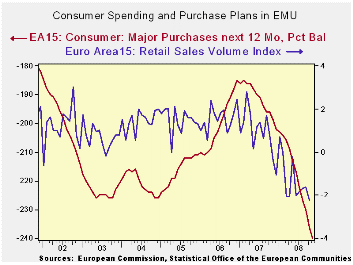

masked by the pick up in inflation. The chart shows the growth of EMU

retail sales volumes. Its trends revels clearly that sales volume

trends have been decelerating sharply and that sales are shrinking.

The EMU PMI indices have been showing deterioration most

sharply in the past few months. Moreover those series are more topical

with observations for November while retail sales headlines are

available for October and component data are fresh only through

September. The more topical data and the inflation adjusted data tell

the most pessimistic story and unfortunately these are the more

reliable reports at the moment.

The European consumer will be contributing to this weakness

more in the coming months. Dropping consumer confidence and a sharp cut

in the German auto industry’s outlook for its sales contribute to such

a view. The spike up in Ireland’s rate of unemployment to its highest

mark since 1998 and Spain’s drop in consumer confidence are further

signs of growing and widespread deterioration. The signs of weakness

are there throughout the Zone and the UK and are they growing in

intensity and spreading across the region. Any European that though

that the slowdown would be confined to the ‘other side of the pond’ is

now thoroughly disabused of that notion.

| Ezone (15) Retail Sales Volume | ||||||

|---|---|---|---|---|---|---|

| Oct-08 | Sep-08 | Aug-08 | 3-Mo | 6-Mo | 12-Mo | |

| Euro Area 15 Total | -0.8% | 0.0% | 0.1% | -2.6% | -1.2% | -2.3% |

| Food | -0.5% | 0.1% | 0.4% | 0.0% | -1.5% | -2.5% |

| Nonfood | -0.9% | 0.0% | -0.1% | -3.8% | -0.6% | -2.0% |

| Textiles | #N/A | 2.6% | -1.7% | 14.0% | 12.5% | -0.9% |

| Books news | #N/A | -0.2% | 0.0% | 3.0% | 1.8% | 0.0% |

| Pharmaceuticals | #N/A | -0.2% | 0.4% | 1.8% | 2.5% | 1.6% |

| Other Nonspecial | #N/A | -0.5% | -0.5% | -0.4% | -1.1% | -3.2% |

| Mail Order | #N/A | 1.0% | -1.9% | 10.7% | 6.2% | 2.3% |

| Country detail: Volume | ||||||

| Germany: Volume excl Auto | -1.6% | -1.0% | 1.6% | -3.9% | -2.2% | -1.4% |

| Italy (Total Value) | #N/A | 0.3% | -0.5% | 1.5% | 0.4% | 0.0% |

| UK (EU): Volume | -0.1% | -0.6% | 1.1% | 1.7% | 1.7% | 2.0% |

| Shaded areas calculated on a one-month lag due to lagging data | ||||||

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.