Global| Jul 14 2016

Global| Jul 14 2016Euro Area Progress and Peril

Summary

EMU area and country level inflation continues to coalesce around the zero mark as it has since late 2014. There are hints of inflation divergence cropping us as the chart shows Italian inflation moving even lower while German [...]

EMU area and country level inflation continues to coalesce around the zero mark as it has since late 2014. There are hints of inflation divergence cropping us as the chart shows Italian inflation moving even lower while German inflation is starting to gather upward momentum. It's too soon to tell if there is any veracity to that divergence or if it's just an incipient departure of those two series.

EMU area and country level inflation continues to coalesce around the zero mark as it has since late 2014. There are hints of inflation divergence cropping us as the chart shows Italian inflation moving even lower while German inflation is starting to gather upward momentum. It's too soon to tell if there is any veracity to that divergence or if it's just an incipient departure of those two series.

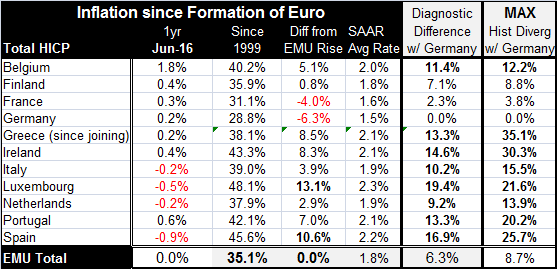

Austria has not yet reported, but of the remaining original EMU members plus Greece, prices are falling year-on-year only for Italy, the Netherlands, Luxembourg, and Spain. Spain's -0.9% is the weakest inflation in the group. Over the past year, Spain has gained 1.1% in competiveness on Germany reducing its price level divergence with Germany since forming the EMU area into a common currency zone to 16.9%. At one time, Spain's price level had risen 25.7% above Germany's compared to its starting ratio of no divergence.

Spain, Portugal, Ireland, and Greece form one bloc that has lost competitiveness in the 13.3% to 16.9% range to Germany since the EMU was formed. Luxembourg has lost the most with a divergence of 19.4%, but that is less of an issue for Luxembourg since it is a financial center. Belgium, Italy, and the Netherlands have lost in the neighborhood of 10% in competiveness to Germany since the EMU was formed. Finland is at a 7% loss and France has kept pace the best losing only 2.3%.

All of the original EMU members have reduced their price level divergences with Germany from their peaks. Greece has come the farthest followed by Ireland and then Spain. Belgium, Finland, and Luxembourg have trimmed their divergences the least. I leave France off this list because France has kept its competitiveness loss to Germany small throughout.

Despite the progress in remolding euro area competiveness along its original lines, divergences persist. Spain and Portugal, despite austerity programs, are in violation of the budget goals they set; while making progress, they have not made enough progress. The EU statement on this was made on July 7 and can be found here. The clock is ticking on what the EU will require of Spain and Portugal next.

Spain still has the highest unemployment rate among the original members at 19.8% with Portugal in second place at 11.6% and Italy at 11.5%. But progress is still being made. Spain's unemployment has fallen by 2.7 percentage points over the last year while inflation has continued to drop. Ireland's unemployment rate has fallen by 1.8 percentage points. Portugal's rate has fallen by 0.8 percentage points, the same as Italy's.

The EMU region is making progress on all fronts as inflation remains low. Inflation divergences are being reduced and unemployment is dropping across nearly all euro area members. Fiscal progress is also in train if not always `on schedule.' But growth remains low and unemployment rates, falling as they are, persist at unnaturally high levels.

The interesting development is this notion of inflation divergence coming back. Just among Germany, Italy, France and EMU year-over-year divergences recently were as great as 1.6 percentage points- that maximum coming between Italy and Germany in 2012. Right now that group is clustered in a one-half of one percentage point range. The current major divergence with the entire group has Belgium at one extreme where its year-on-year rate is 1.8%; it has the greatest divergence with Spain at -0.9% for a 2.7 percentage point gap.

If divergence continues, with German inflation growing faster than in the rest of the euro area, that would be a very unusual development. For most of the EMU's existence, Germany has been the low inflation country. But given the strength, particularly the relative strength, in the German economy it is a possible result. The positive effect will be to reduce further price level differences between Germany and other members compared to the levels that were in place when the EMU was begun. The bad news would be that it would make Germany much less tolerant of easy ECB monetary policy. These trends are worth watching out in the months ahead; these developments will be important to the functioning of the euro area in the months ahead.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.