Global| Jun 02 2010

Global| Jun 02 2010Euro-Area PPI Takes Off Slowly I Turn... Err Scratch That

Summary

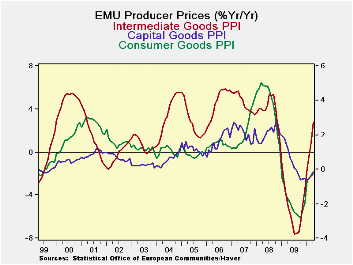

Producer price trends have been rising sharply in EMU over the past few months. The PPI has taken a decided and sharp turn for the worse. Prices are accelerating in two of the three main sectors of the PPI. Only consumer prices fail [...]

Producer price trends have been rising sharply in EMU over the past few months. The PPI has taken a decided and sharp turn for the worse. Prices are accelerating in two of the three main sectors of the PPI. Only consumer prices fail to show acceleration from three-months to six months. Consumer prices and intermediate prices are still lower Yr/Yr but their trends are nonetheless rising sharply. Intermediate goods prices are up very strongly from past weakness.

Germany and France show manufacturing prices ex-energy or ex-energy and ex-food trends (the former for Germany, the latter for France) with accelerations in train. UK manufactures prices are accelerating (the UK is an EU member). Italy’s prices are actually decelerating over three months compared to stronger pressures earlier.

While the PPI is not the price a gauge of choice for the ECB, having such pressures stirred up will not be good news. The dropping euro undoubtedly has something to do with this.

Still Yr/Yr prices are contained for consumer goods and capital goods. Intermediate goods prices are the biggest problem. There the rise in the dollar price of oil and the dropping euro form a double-whammy on prices. If these trends develop in the HICP they will put the ECB on the spot since growth in the Zone is not doing well and the ECB will not want inflation trends like this to take hold in consumer prices.

| Euro-Area and UK PPI Trends | ||||||

|---|---|---|---|---|---|---|

| M/M | Saar | |||||

| Euro-Area | Apr-10 | Mar-10 | 3-Mo | 6-MO | Yr/Yr | Y/Y Yr Ago |

| TotalxConstruct | 0.7% | 0.6% | 5.8% | 6.4% | 2.8% | -4.7% |

| Capital Gds | 0.2% | 0.1% | 1.1% | 0.4% | -0.2% | 1.2% |

| Consurmer Gds | 0.1% | 0.0% | 0.5% | 0.7% | -0.3% | -1.7% |

| Intermediate&Cap Gds | 1.0% | 0.8% | 8.1% | 6.8% | 2.7% | -5.1% |

| MFG | 0.4% | 0.6% | 3.9% | 6.2% | 3.7% | -5.9% |

| Germany | ||||||

| Gy ExEnergy | 0.5% | 0.2% | 4.3% | 3.1% | 1.1% | -1.9% |

| France:Tot | ||||||

| Fr ExF&Energy | 0.6% | 0.3% | 4.2% | 3.3% | 1.0% | -1.6% |

| Italy | 0.5% | 0.5% | 3.7% | 6.7% | 4.1% | -6.2% |

| UK | 0.9% | 0.6% | 8.1% | 7.1% | 5.8% | 1.3% |

| Euro-Area Harmonized PPI ex construction | ||||||

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief