Global| Oct 27 2016

Global| Oct 27 2016Euro Area Money Supply Crawls Higher

Summary

Money supply (M2) growth in the EMU slowed its year-on-year pace to 5% in September from 5.2% in August. After being boosted to a peak year-on-year pace of 6.8% in July 2015, EMU money supply growth has steady decelerated and has been [...]

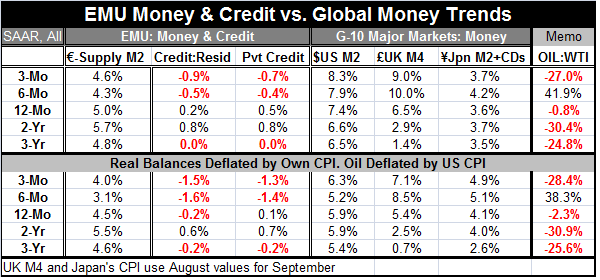

Money supply (M2) growth in the EMU slowed its year-on-year pace to 5% in September from 5.2% in August. After being boosted to a peak year-on-year pace of 6.8% in July 2015, EMU money supply growth has steady decelerated and has been stabilizing at a pace of around 5% since April. Private sector credit peaked at a year-on-year pace of 2% in November 2015 then fell back quickly to post a series of growth rates since then between 0.2% and 0.6%. As of September, private sector credit is up at a 0.5% pace year-on-year.

Money supply (M2) growth in the EMU slowed its year-on-year pace to 5% in September from 5.2% in August. After being boosted to a peak year-on-year pace of 6.8% in July 2015, EMU money supply growth has steady decelerated and has been stabilizing at a pace of around 5% since April. Private sector credit peaked at a year-on-year pace of 2% in November 2015 then fell back quickly to post a series of growth rates since then between 0.2% and 0.6%. As of September, private sector credit is up at a 0.5% pace year-on-year.

The table below presents growth rates on shorter and longer horizons. Shorter term growth calculations for money supply are generally weaker. The same is true of the two credit measures that are each weaker over three months and six months than over 12 months. In fact, both credit measures show declines over three months and six months while they have posted small increases over 12 months.

Expressed in real terms, money growth and credit growth are still weaker over the shorter horizons and a hair's breadth away from decelerating as well.

On balance, EMU monetary trends are not encouraging. Money growth is not responding and neither is credit growth. The ECB has been waiting to announce a step up in its stimulus. That will likely be forthcoming since there is no sign that anything else helpful is in progress.

On a day not saturated with news reports, there is still some other 'good news' to report. The U.K. released a stronger Q2 GDP report than what had been expected. Q3 U.K. GDP gained 0.5% compared to the 0.3% expected. In a separate report, U.K retailers surveyed in October reported to be looking for the strongest gain in sales that they have expected over the past 12 months. Meanwhile, in Italy both business and consumer confidence indicators eroded in September.

Baltic Dry Goods Index Gains

Baltic Dry Goods Index Gains

After cratering early in 2016, the Baltic dry goods index an important gauge of international shipping volume has been on a steady diet of increase. The chart plots the levels of the index since 2011. While the level of the dry goods index is still low, it has been making steady gains with only a recent series of backtracking moves which seem to be 'statistically normal.' If this gauge is pointing to a true pick up in international trade, it could be some of the best news that the ECB could get or the BOE or the Fed or the BOJ or PBOC for that matter. The up-creep in the index is steady and it is strong enough to make a difference. And good news has been hard to come by recently.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief