Global| Dec 14 2016

Global| Dec 14 2016Euro Area IP Falls

Summary

It's a mixed bad for Euro-Area industrial output as output fell for the second month in a row. The October drop is a decline of only 0.1% and compares to a drop of 0.9% in September. In August IP had spurted by 0.9% and that gain [...]

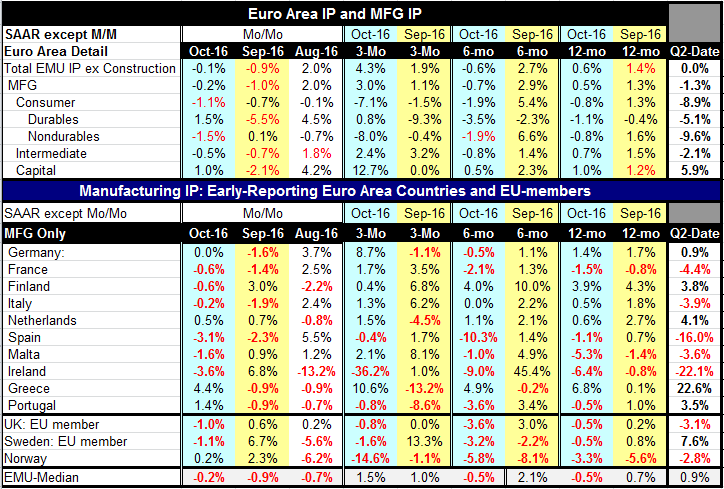

It's a mixed bad for Euro-Area industrial output as output fell for the second month in a row. The October drop is a decline of only 0.1% and compares to a drop of 0.9% in September. In August IP had spurted by 0.9% and that gain still drives the three-month growth rate which stands at a 4.3% annual rate.

It's a mixed bad for Euro-Area industrial output as output fell for the second month in a row. The October drop is a decline of only 0.1% and compares to a drop of 0.9% in September. In August IP had spurted by 0.9% and that gain still drives the three-month growth rate which stands at a 4.3% annual rate.

The pattern of these monthly changes causes the three month growth rate to exaggerate momentum. In the quarter to date IP is actually running at a dead flat zero rate of growth. Despite some life in the more sensitive PMI gauges the actual measures of industrial output in EMU are not performing very well. And three month calculations put an exaggerated glow on recent trends.

By sector IP shows weak to modest rates of growth in all main sectors: consumer goods, intermediate goods and capital goods. These growth rates do perk up over three-months but only on the strength of gains in August as September and October have brought lethargy or weakness to each sector.

Year on year manufacturing is up by 0.6%, consumer output is off by 0.8%, intermediate goods output is up by 0.7% and capital goods output is up by 1.0%. Over six months all of the sectors show declining output except capital goods.

Looking at the Euro-Area by members instead of sectors we find that of the 10 members in the table six show production declines in October and six showed declines in September. Even though August was a much better month for EMU as a whole, production declined in that month in in five countries but it also expanded very strongly (by 2.4% or better) in each of the four largest EMU member economies: Germany, France, Italy and Spain.

In the quarter to date industrial output is falling in five of 10 of the members in the table and in two of the three added European counties at the table bottom.

In short, the IP trends and the pattern monthly observations do not support the view that we get from the improving PMIs for MFG. It may be that the PMIs are ahead of the curve - they are more sensitive as gauges of the economy. It might also be that the PMIs are sensitive and volatile. This is will be something to watch.

Occasionally the PMIs and the data they portray do go their separate ways for a while. And right now that could be risk to policymakers. OPEC is feeling its oats oil prices are rising and for a while we ae going to have the trappings of better growth and rising inflation. It could cause tensions in the Euro-Zone between Germany and other members as well as within the ECB itself. It's a risk that could be deepened if the PMIs disconnect and exaggerate strength.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief