Global| Apr 14 2016

Global| Apr 14 2016Euro Area Inflation Hovers and Skims Zero

Summary

EMU inflation shows prices hovering around unchanged over the past 12 months. Core inflation is close to 1%. Inflation's progress for the headline over six-month and three-month shows a tendency to faster declines over shorter [...]

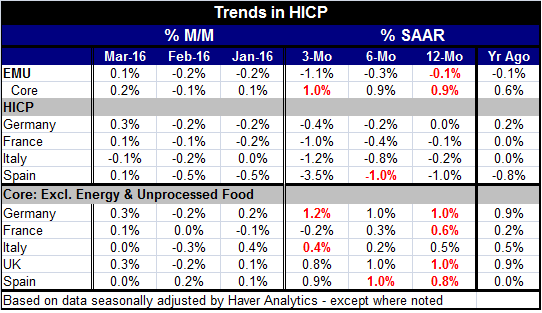

EMU inflation shows prices hovering around unchanged over the past 12 months. Core inflation is close to 1%. Inflation's progress for the headline over six-month and three-month shows a tendency to faster declines over shorter periods. In other words, deflation is still gaining momentum. But set aside food and energy, `core' inflation has been stuck at 1% over this entire span.

EMU inflation shows prices hovering around unchanged over the past 12 months. Core inflation is close to 1%. Inflation's progress for the headline over six-month and three-month shows a tendency to faster declines over shorter periods. In other words, deflation is still gaining momentum. But set aside food and energy, `core' inflation has been stuck at 1% over this entire span.

The four largest EMU economies, Germany, France, Italy and Spain, show inflation flat to lower over 12-month. The progression to shorter time periods shows the deflation trend increasing over short periods for each of these countries. In the largest EMU nations' headline, deflation is gaining.

For core inflation, trends are somewhat mixed but best summarized overall (even including the U.K.) as moving sideways at 1%. The exceptions to some extent are Italy and France where for each inflation is at about 0.5% over 12-month and lower over three-month and six-month. In France, the progression lower is steady; in Italy, it is not. France's core prices are falling over three-month. In Italy, the three-month pace moves back up to 0.4%, just below its year-on-year pace of 0.5%.

For the past year, the headline has been trapped in a range that has a center of gravity just above zero. The trend for the big three EMU economies really has moved in lockstep with the German rate always just a bit higher than inflation in France, Italy and the EMU recently. Relatively higher German inflation has been a characteristic since early 2013.

Over this period, the ECB has taken various steps to try to get inflation higher as it has an inflation target mandated at just below 2%. But as the chart shows (and the tabular data) neither inflation nor the core have been significantly affected or moved to that target. Of course, during this period there has been the significant complication of falling global oil and commodity prices. Weak and falling energy prices have blunted the ability of the ECB to get inflation higher. But recently oil has stabilized as speculation over this weekend's greater-OPEC meeting has run wild. One day markets think there will be an oil deal; the next day a deal seems out of the question. Over the last week several new estimates of oil demand have showed slipping expected volumes, but there is also incoming evidence of oil firms shutting down operations and of U.S. banks being hurt for their lending to the oil sector. This has simply added to the confusion about where the supply-demand balance is headed.

One point to bear in mind that does not seem obvious to many is that the oil technology has progressed very rapidly and it is here to stay. Technology has lowered the breakeven point for various sorts of alternative oil production. Many cite that these new processes can be profitable with oil prices as low as $40/bl. If that information is correct, it would seem to make oil price much higher than $40 quite unlikely in the near term as any move about $40 would cause those new suppliers to come back on stream. Moreover, firms going bankrupt may not even be an issue. When a firm goes bankrupt, others firms come in and scoop up the assets for pennies on the dollar and can be ready to redeploy them with an even lower breakeven production point in the future. Bankruptcy does not seem to be much of a factor in affecting the supply-demand balance.

On balance, I do not think oil has much near term upside at all. The speculation about the greater OPEC meeting continues to ignore the fact that Iran's participation is surely off the table in the wake of it's getting out from under sanctions and trying to ramp its output back up. And several have made Iran's participation in a deal a `must do.' So what happens when must-do meets can't do? We have seen markets willing to seesaw on speculation based on no new facts at all surrounding this trade off. On balance, I do not expect to go into next week with oil prices any higher because of this OPEC meeting.

Inflation trends are going to have to reestablish themselves in an environment where oil prices become stable and possibly bounce a little off their most recent lows. In that environment, we can expect less evidence of deflation. Of course, deflation has also been put in train by the stronger dollar which has spread a smothering impact on global commodity prices. The dollar for now has moved lower, but the Fed is hovering and if it pounces on a new agenda of rate hikes, the dollar could ride that trend to higher values again and set some new deflation forces in train and into the commodity price sector quite separate from oil. And let's remember that Japan has had a long run during which it has continued to fight deflation without oil having played the central role.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief