Global| Nov 29 2016

Global| Nov 29 2016Euro Area and EMU Indices Advance in November But Barely Gain Year-Over-Year

Summary

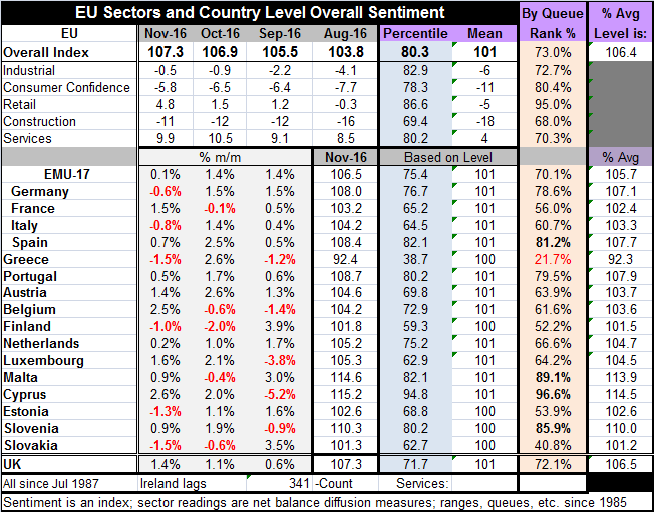

The EU Commission indices for November showed a pick up on the month and the highest EU index in 11 months. The EMU area index ticked higher to 106.5 in November from 106.4 in October; its highest reading in 11 months as well. The EU [...]

The EU Commission indices for November showed a pick up on the month and the highest EU index in 11 months. The EMU area index ticked higher to 106.5 in November from 106.4 in October; its highest reading in 11 months as well. The EU and its sector indices generally show less upward momentum than the Markit two-sector PMI indices.

The EU Commission indices for November showed a pick up on the month and the highest EU index in 11 months. The EMU area index ticked higher to 106.5 in November from 106.4 in October; its highest reading in 11 months as well. The EU and its sector indices generally show less upward momentum than the Markit two-sector PMI indices.

The EU sector indices show month-to-month improvement in four of the five readings. The reading weakening on the month is for services, but it is still above its September level by a good margin, and except for October, the November reading is the strongest in six months. The services sector is hardly showing weakness in November; it just backed off a strong October reading.

The queue standing of the level of the headline and the various sector indices show still firm to strong readings in the EU. The overall EU reading as a 73rd percentile reading while the EMU has a similar 70th percentile reading. The EU sectors show that the relative strength is in retailing with a 95th percentile standing, higher only 5% of the time since 1987. Consumer confidence notches an 80.4 percentile standing. The rest of the sector readings are in the low 70th percentiles or high 60s (68th percentile for construction). These are generally firm but mid-range readings.

Of 16 early reporting members (Ireland does not report early), six showed month-to-month declines in their overall sentiment gauges. Most of the countries are clustered around mid-range values. Greece has the relative lowest sentiment index at its 21st percentile. Cyprus has the relative highest standing at its 96.6 percentile with three other countries having standings in their respective top 20th percentile. The average country reading (unweighted) is at its 65th percentile, a bit below the overall EMU mark; that tells us that the large economies have slightly stronger readings in general.

On balance, the EMU region seems to be even keeling. There is a slight tendency for growth but not strong momentum, and while there is scattered country weakness, there is no evidence of weakness being endemic or cumulating. Only four of 17 early reporting EMU members show two national sentiment declines in the past three months. Four others show a string of three increases in a row with no declines over three months. The monthly results seem to reflect the normal ebb and flow of economic growth. There is not much evidence of a change in speed in any direction. Year-over-year, the levels of the sentiment indices are little changed.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief