Global| Apr 29 2014

Global| Apr 29 2014EU Sentiment Rises; EMU Sentiment Is Set Back

Summary

The EU sentiment indicator rose in April as the same indicator for EMU fell by 0.5%. All EU-wide sector indicators rose month-to-month except construction. The UK economy is on fire, with its sentiment index in the 94th percentile of [...]

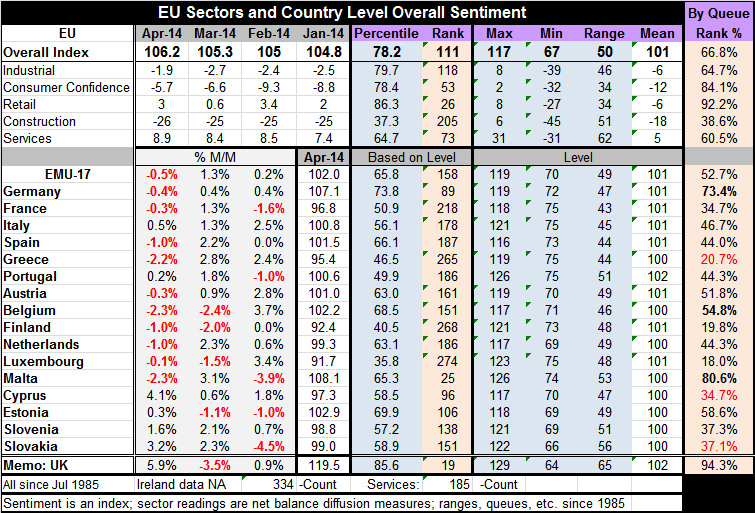

The EU sentiment indicator rose in April as the same indicator for EMU fell by 0.5%. All EU-wide sector indicators rose month-to-month except construction. The UK economy is on fire, with its sentiment index in the 94th percentile of its historic queue, higher only 6% of the time. UK GDP has just posted a 0.8% rise in Q1 2014 over Q4 2013.

The EU sentiment indicator rose in April as the same indicator for EMU fell by 0.5%. All EU-wide sector indicators rose month-to-month except construction. The UK economy is on fire, with its sentiment index in the 94th percentile of its historic queue, higher only 6% of the time. UK GDP has just posted a 0.8% rise in Q1 2014 over Q4 2013.

The indices for the European Monetary Union showed declines in overall sentiment in 11 of the 16 EMU members listed in the table. The one-month declines range from 2.3% in Malta and in Belgium to -0.1% in Luxembourg, -0.3% and -0.4% for France and Germany, respectively. The overall EMU gauge fell by 0.5% on the month after climbing 1.3% the month earlier. The countries showing sentiment gains on the month were the Mediterranean countries of Italy and Portugal as well as Cyprus, Estonia, Slovenia and Slovakia.

The chart shows that while activity and inflation in the EMU historically have moved with a positive correlation over the business cycle, we are now in a very unusual situation: activity continues to move higher while inflation continues to move lower. While the European Central Bank has said that it stands ready to do more and to possibly engage in a program of quantitative easing, in comments today made in by ECB President Mario Draghi to German lawmakers, the message was that quantitative easing would not be enacted any time soon. While the way seems to been cleared for the ECB to engage in such transactions, the desire by the central bank to use asset-backed securities may be hampering its ability to act since there are so few of those in Europe available for monetary operations. At the moment, Europe seems to be caught in this strange dilemma in which its growth is improving but its inflation is falling. Not only is inflation falling, but it's well below its target, much as it is in the US.

Industrial Confidence: Among monetary union members industrial confidence slipped in April falling to a reading of -4 from -3 in March. This is the same level of the reading that persisted in February and January. Germany's industrial sector slipped from 1 to 0; France's sector improved to -7 from -8; Italy's improved to -4 from -5; Spain's also improved to -9 from -10. The UK, not a participant in the single currency arrangement, saw its industrial sector reading jump to 8 from 1, reversing a one-month slowdown.

Consumer Confidence: Consumer confidence in the EMU was flat in April at -9, the same as in March, although those readings represent improvements from the -13 reading in February and the -12 reading in January. Confidence improved in Germany, Italy and Spain, as it fell in France. Consumer confidence readings are widely different across the euro area. Just looking at the four largest economies, France's reading is a -21.7 compared to Germany's reading of 3.1.

Retailing: Retailing in the euro area was flat at a reading of -3 where it has been for all four months of 2014. In Germany the retail sector took a step back, falling from readings of 1 and 2 early in the year to post a reading of zero in April. France continues to post a reading of -10, about what has been showing since earlier in the year. Italy's reading of -5 is an improvement from -8 in March, but its retailing indicator has been fluctuating. Spain's retailing indicator fell back to 7 from a year-high reading of 8 in March. On balance, large EMU member countries continue to show this flatness in retailing. By comparison in the UK the retailing the index jumped to 21 from 8 in March; but the UK indicator is only back to the region that it had occupied in January and February of this year. Still UK retailing performance is a league apart from that sector's performance in EMU nations.

Services: The services sector, the job creating sector for Europe, saw setbacks to a reading of 4 in April from 5 in March; but that reading of 4 is still better than the readings of 3 and 2 in February and January earlier in the year. For the moment, this looks like oscillating progress. Germany's reading for the services sector was flat at 15 in April, but that's lower than it had been in February and January. France's reading showed an improvement to -6 from -7 and those are ongoing improvements from earlier in the year. For Italy there was slippage to -10 from -6 in March, but that only took the services sector reading back to its level of February. Spain also showed month-to-month slippage, but its trends are hard to read. At least the consumer numbers for the euro area as a whole are positive values. On a country-by-country basis, there doesn't seem to be much clear momentum. Moreover, the differences among the various EMU economies seem to be more or less stuck in place.

Construction: The euro area construction sector slipped to -30 from -29; it has been fluctuating between these two values throughout 2014. Germany shows a slip to -10 from -7 for its construction sector in April. France slips to -32 from -29. Italy slips to -37 from -36 and Spain slips to -54 from -53. Each of the largest economies in the monetary union saw some slippage in construction in April.

Employment prospects: Expectations for employment slipped in the monetary union's industrial sector in April to -6 from -5. In retailing employment expectations improved slightly to -1 from -2. Services sector current employment was found to improve to a plus 2 reading compared to -1 in March; expected employment in services remained flat at a plus 2 reading. In construction, employment expectations slipped to -21 from -18 to the lowest value of the year. Expectations for unemployment overall fell to 18 in April from 20 in March, indicating some improvement on the consumer confidence front.

Sum-up: This month's data from the European Commission highlight the ongoing problem of recovery in the euro area. We could not say that this month represented another good report on the recovery trail since the overall EMU sentiment index fell and the indices for most of the EMU members fell. Yet, in the same month, the PMI indicators from Markit have shown improvement. When we find indicators of the same thing producing different results, it's fair to conclude that there's a good deal of turmoil going on in that thing that they are trying to measure. We already know there's a great deal of disparity among EMU countries. Because of that, measures that use different weights are going to produce different results. But even apart from that, survey results derived from a boiling pot of disparate results is likely to produce uneven samples and readings. And the individual countries of EMU also are like a boiling pot with uneven economic readings from month-to-month. All of this is just further evidence of how the EMU countries are still struggling with growth. Undoubtedly, the geopolitical turmoil has now become part of this, as geopolitical and economic uncertainties surely have risen.

The real success story that comes out of these data previous reports and a new sampling of first quarter GDP involves the UK. The United Kingdom shows clear strength anyway you sample it measured or slice it. The growth there is real and solid, making the UK the envy of Europe. Growth in the UK is not yet strong. The UK also has financial sector issues it has to deal with among its domestic problems. However, the UK has put itself on a growth path and has done it by sticking to its budget targets and that's more than you can say for the European Monetary Union.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief