Global| Mar 30 2015

Global| Mar 30 2015EU Indices Improve in March

Summary

The EU Commission indices for the EU and EMU showed improvement in both regions in March. For the broader EU regions, the index of sentiment gained 0.9 points mostly on the back of improved retail sentiment and improved consumer [...]

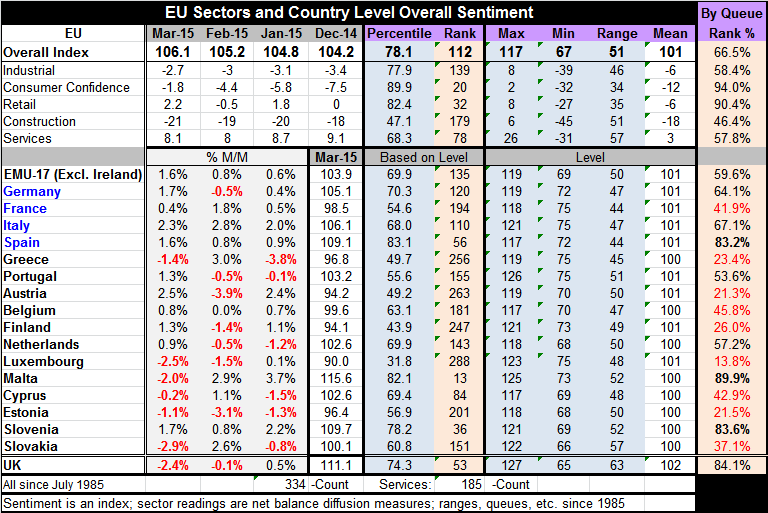

The EU Commission indices for the EU and EMU showed improvement in both regions in March. For the broader EU regions, the index of sentiment gained 0.9 points mostly on the back of improved retail sentiment and improved consumer confidence. There were sector improvements in four of five sectors. The retailing sector index improved by 2.7 points month-to-month, rising to reading of +2.2. Consumer confidence improved by 2.6 points month-to-month but still carries a net negative reading of -1.8 in March. There was a small advance of 0.1 month-to-month for the services sector which posted a reading of 8.1. The industrial sector improved by 0.3 points, also posting a net negative reading of -2.7 in March. Only construction deteriorated between February and March. The overall EU reading was last at 106.1 eight months ago.

The EU Commission indices for the EU and EMU showed improvement in both regions in March. For the broader EU regions, the index of sentiment gained 0.9 points mostly on the back of improved retail sentiment and improved consumer confidence. There were sector improvements in four of five sectors. The retailing sector index improved by 2.7 points month-to-month, rising to reading of +2.2. Consumer confidence improved by 2.6 points month-to-month but still carries a net negative reading of -1.8 in March. There was a small advance of 0.1 month-to-month for the services sector which posted a reading of 8.1. The industrial sector improved by 0.3 points, also posting a net negative reading of -2.7 in March. Only construction deteriorated between February and March. The overall EU reading was last at 106.1 eight months ago.

In the EMU, the index rose to 103.9 in March from 102.3 in February. It was last higher in July 2011. Of the 17 reporting EMU members, 11 saw month-to-month increase in their country level indices; six saw declines month-to-month. The declines were mostly across the smaller EMU members: Luxembourg, Malta, Cyprus, Estonia, Slovakia and Greece.

If we assess the EU and EMU readings to place them in their respective historic perspectives, we find that the EU index stands in the 66.5 percentile of its historic queue - just outside the top one-third of its historic range. The EMU index stands at its 59.6 percentile, a bit lower in its relative standing and just below its 60th percentile (just outside the top 40% of its queue). These are exceedingly moderate readings. The chart above shows that among the big four EMU members only Italy is improving strongly. The rest are static or rising listlessly.

Looking at the various sector standings in the EU, the consumer and retail sectors have the higher relative queue standings. Setting aside the raw diffusion values, the queue values look at each sector and evaluate it as a percentile standing in its historic queue of observations. Consumer confidence, despite is negative reading, has been higher only 6% of the time since 1987. Retailing has been better only 10% of the time. But the services and industrial sectors have been better only about 42% of the time. Construction has been better about 54% of the time.

By sector, the overall reading for the EMU is being carried higher by consumer attitudes and by retailing. By country, the EMU's nearly 60th percentile standing is exceeded by Germany which stands at its 64th percentile, Italy at its 67th percentile, and Spain at its 83rd percentile. But France lags, with its standing in its 41st percentile. These are the four largest EMU economies.

It is somewhat surprising to see that the consumer is pushing the overall EMU index higher and that services and manufacturing are holding things back. While German confidence has been much higher than other EMU members in some of the national indices, in the EU Commission framework confidence in Italy and Spain exceeds consumer confidence in Germany in their relative standings since 1987.

Consumers in Europe are actually in much better spirts. That explains why the retail sales sector is one of the leading sectors. The EMU-wide expectation for unemployment has seen its reading drop from a diffusion level of 24 in December to a reading of 7 in March - a very sharp drop. In fact, the unemployment diffusion raw score fell from 15 in February to 7 in March, a particularly large drop. Since 1987 the fear of unemployment has fallen more rapidly over three-months only three other times- and that was on a string of three consecutive months in 1994. In the EMU, consumers are starting to lose their fear. Watch Europe's consumer and retail sales trends since those sectors are leading Europe ahead, not manufacturing.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief