Global| Apr 29 2020

Global| Apr 29 2020EU Indexes Fall Hard

Summary

There is no-catching the dropping, tumbling knife There is not much to analyze in the EU indexes this month. The bottom fell out and everything went down with it. One sector, construction, shows some 'resilience' (as it has been doing [...]

There is no-catching the dropping, tumbling knife

There is no-catching the dropping, tumbling knife

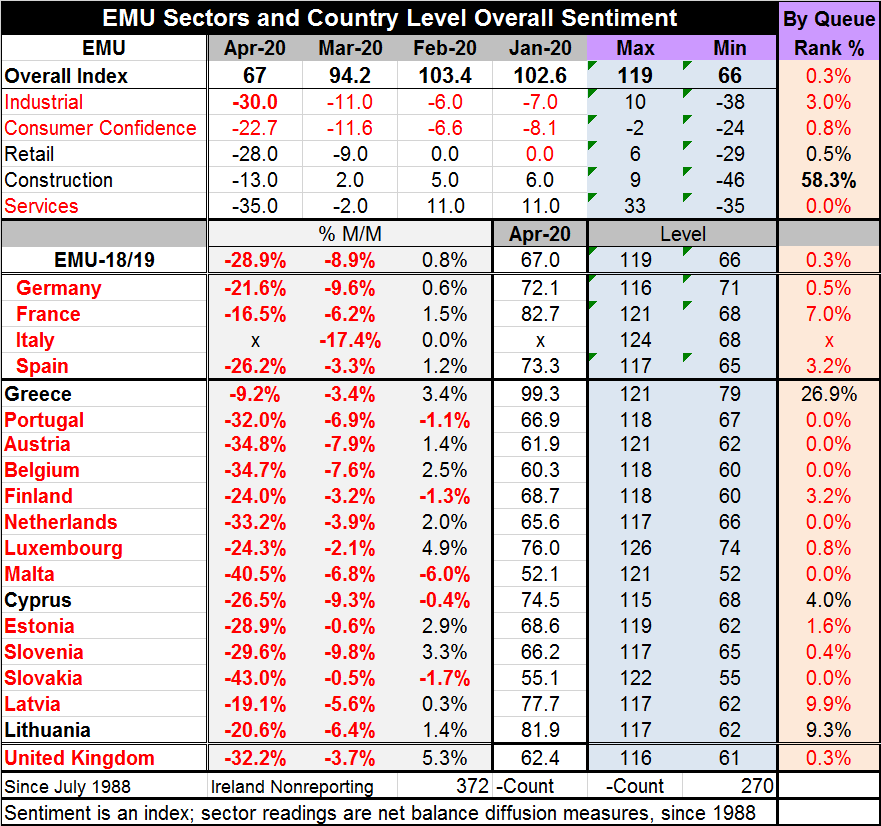

There is not much to analyze in the EU indexes this month. The bottom fell out and everything went down with it. One sector, construction, shows some 'resilience' (as it has been doing in recent months) with a reading of -13. That is at its 58th percentile, still holding above its historic median (the median occurs at a rank of 50%). All other sector gauges as well as the overall index are in the bottom five percentile of their respective historic queues of data. All except construction are abysmally weak and every sector with no exceptions fell hard this month.

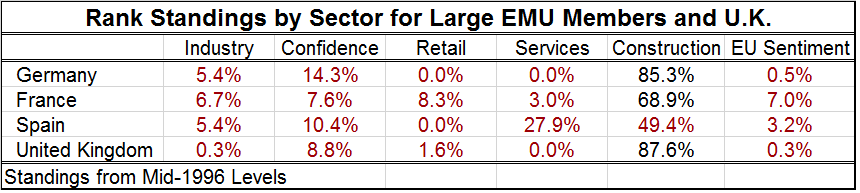

The sectors are weak across all the large economies as well with construction as the sole exception. Spain makes a very weak 27.9 percentile standing for its service sector almost strong-looking given the comparisons.

Sectors by country: sector ranking for large reporting economies EMU plus U.K.

Country readings

I can try to distract you from the sector carnage by looking at country level sentiment gauges, but that won't work either. The best performing individual economy this month is Italy, but only because it didn't report at all! All reporting countries made double-digit percent drops month-to-month except Greece where the index fell by 9.2%, just short of the double-digit cup. The EMU gauge fell by 28.9% month-to-month. Germany fell by 21.6%. Among the three reporting largest economies, France fell the least by drooping 16.5%. April follows a string of weak and falling indexes in March, but April is much worse.

The GDP factor

The hammer fell in April. Today's U.S. GDP for Q1 was reported and March was so weak it carried U.S. GDP into negative territory for Q1. The Q2 expectation for the U.S. is so weak; it is actually hard to put such numbers into spreadsheets and believe the results. But the U.S. and European Q2 GDP numbers are going to be terrible- truly terrible.

Dealing with market optimism

So far, markets are taking all this in stride. The contraction in Q1 GDP today still find stocks rising by 2% or more around mid-day. There is some optimism about the virus and how its situation is evolving.

But I am cautionary about trading virus news as markets are doing. The virus news has been 'looking good' but the shutdown has damaged economies and resulted in deaths. There is little notion of how quickly or fully the economies of the world will recover or to the notion of the best state to which they can return. And how will that state relate to their previous state? By this I mean the previous pace of growth and level of unemployment and so on; what will be the metrics in the new post virus normal...where there will still, be some virus? With markets already showing significant recovery, the most significant thing for valuing equities is not going to be trading off of virus news. The speed of opening remains important. But more crucial is going to be getting a fix on the endpoint - how fully will economies recover. And that is still a very speculative proposition. I think all too many people are assuming that economies are going to pick up where they left off before the virus…and I doubt that will happen. Good luck.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief