Global| Sep 29 2009

Global| Sep 29 2009EU Index Rises For The Sixth Month In A Row, But...

Summary

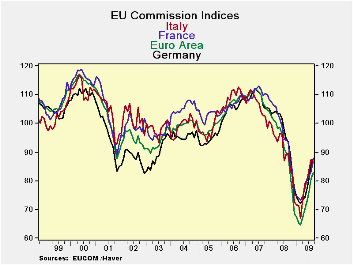

The EU Commission indices for the EU area show that improvement continued in September. Still it was the smallest mo/mo gain since the string of increases began. As a percentage of their range of values the country specific readings [...]

The EU Commission indices for the EU area show that improvement continued in September. Still it was the smallest mo/mo gain since the string of increases began. As a percentage of their range of values the country specific readings are still 15% or more below their respective range midpoints. The UK is the relative strongest and Spain is the relative weakest. In Sept both Italy and Spain backtracked. The UK reading was flat. Those are not good developments.

EU sectors: The EU sector readings show great divergence. Retailing stands in the 45th percentile of its range, the best relative reading over all sectors. Consumer confidence in the 44th percentile and is second best. The industrial and services sectors are behind with relative readings of about the 32nd percentile. Construction is far weaker, standing in its 15th percentile. The raw readings are all negative thus no sector is advancing. That is a key difference between the EU Commission and the NTC-Markit indices where both MFG and Services readings are close to 50 and where the combined reading already shows expansion.

Queue Percentiles - Note that the EU readings are even weaker when ranked by queue than by their percentage of range percentiles. Queuing, positions the various readings in their range of ranked values, setting the actual level of the observations themselves aside. Calculated in this way the current EMU readings are in the bottom 10% to 20% of their respective queue ranges for EU sectors; they are largely in the 10% to 15% range for country specific readings. Theses readings mean that the actual levels of the September reading are in the bottom 10% to 20% of all readings since late 1988. That is still very weak despite the degree of rebound that is apparent. It is much weaker than the picture portrayed by the range rankings

Industrial sector across large EU countries - Looking at the individual sectors across countries we find the weakness is fairly widespread. For the industrial sector the UK ranks highest in its 34th range percentile followed by France in its 33rd percentile. Germany is weakest in its 23rd percentile. For all of EMU orders are only in the 9th percentile of their range, a very weak reading export orders are in the same relative position. However the production is in its 42nd percentile and the production trend is assessed to be in its 46th percentile.

Consumer readings across large countries - Consumer readings are somewhat better across countries standing in their 59th percentile in the UK, above the range midpoint of 50, at 52.5 in Italy. Spain is on the edge at 49.1 and Germany is the weakest relative reading standing in the 32nd percentile of its range. Consumers still fear unemployment as that reading is a still with a top 30% value. Still the economic situation in the next 12-months is assessed to be in its 60th percentile. The time to make a major purchase had been rated in the bottom 15 percentile over the past 12 months but that is now up to a 52 percentile reading in September looking ahead to the next 12 months. That is quite a bit of an improvement.

Retailing across large countries - The EU retail reading for the UK is actually good in the 70th percentile of its range in September. But France in the 47th percentile stands next in its range followed by Germany at the 41st percentile. Italy is weakest in its 15th percentile. All reading for the EMU retailing sector overall are bottom 25th percentile or worse.

Services in large countries - The service sector is weak with most EU nations at or near the bottom third of their respective ranges. The best range ranking is in the UK at the 36th percentile followed by Germany in the 34th percentile and France in the 28th percentile; Spain is the weakest in its 15th percentile. For the EU sector as a whole employment is in the bottom 6 percentile of its range and expected employment is in the bottom 15th percentile of its range Current demand is assessed as in the 26th percentile while expected demand is in the 29th percentile.

Summing up- On balance the EU is showing some improvement but the pace of gain has slowed with the current readings still quite low. For a more robust recovery the monthly improvements must continue. We looked at the EU index, EMU index and at select large countries in the data above and found weakness is still a major hallmark. Spain and Italy took set backs this month among the large countries. In the UK the country index was flat. Germany slowed its pace of improvement. France alone among the larger countries saw acceleration in its improvement. The outlook for continued expansion is still solid but the assessment of the likely pace is still up in the air and several things, unfortunately now point to a reduced pace of increase including the slowdown in the gain for the EU index this month.

| EU | Sep-09 | Aug-09 | Jul-09 | Jun-09 | Percentile | Rank | Max | Min | Range | Mean | By Queue rank% |

| Overall Index | 82.6 | 81 | 75 | 71.1 | 39.9 | 226 | 116 | 60 | 56 | 100 | 10.0% |

| Industrial | -24 | -26 | -30 | -33 | 32.6 | 230 | 7 | -39 | 46 | -7 | 8.4% |

| Consumer Confid | -17 | -20 | -21 | -23 | 44.1 | 208 | 2 | -32 | 34 | -11 | 17.1% |

| Retail | -11 | -12 | -14 | -17 | 45.2 | 202 | 6 | -25 | 31 | -6 | 19.5% |

| Construction | -35 | -36 | -37 | -37 | 15.2 | 221 | 4 | -42 | 46 | -16 | 12.0% |

| Services | -11 | -11 | -19 | -23 | 31.7 | 144 | 32 | -31 | 63 | 13 | 6.5% |

| % m/m | Sep-09 | Based on Level | Level | ||||||||

| EMU | 2.5% | 6.3% | 3.8% | 82.8 | 34.7 | 225 | 117 | 65 | 53 | 100 | 10.4% |

| Germany | 1.7% | 6.3% | 4.1% | 87.4 | 31.1 | 212 | 121 | 72 | 49 | 100 | 15.5% |

| France | 5.6% | 2.3% | 0.5% | 87.9 | 34.0 | 213 | 119 | 72 | 47 | 100 | 15.1% |

| Italy | -1.5% | 4.5% | 4.4% | 86.2 | 34.7 | 224 | 122 | 67 | 55 | 100 | 10.8% |

| Spain | -1.5% | 3.7% | 5.2% | 80.7 | 28.1 | 226 | 117 | 67 | 50 | 99 | 10.0% |

| Memo:UK | 0.0% | 13.1% | 7.3% | 83.5 | 42.1 | 225 | 121 | 56 | 65 | 99 | 10.4% |

| Since Oct 1988 | 251-Count | Services: 154-Count | |||||||||

| Sentiment is an index, sector readings are net balance diffusion measures | |||||||||||

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief